@tetsuotrees @YIMBYLAND fyi port of Houstons the largest US port by tonnage / 5th by teu’s.

English

Jacob ʃei

6.2K posts

@JacobShiach

Light and Sound based programmable Human. Currently tinkering with programmable biology and money. building @unionprotocol @creditclub_eth

Is there any place geographically you could see the United States building a new major city/metro?

i am sad because i don’t see people talking about apps on the timeline as much as they used to where are the apps? i’ll follow each one and do my best to help tell their story to others

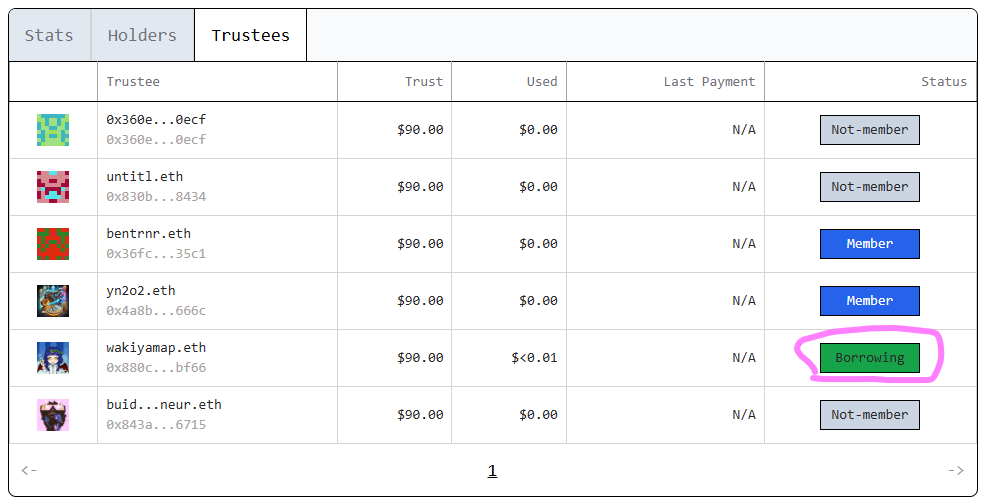

Sometimes you need more than you have in the moment. To realize a dream. To cover an emergency. This is why credit exists. But why let banks and credit agencies have a monopoly on such a vital resource? Enter Union, permissionless credit, now supporting USDC on @base.

USDC loans on @coinbase, powered by @MorphoLabs: May 2 - $120,000,000 Apr 2 - $45,000,000 Mar 2 - $14,000,000 Feb 2 - $2,000,000 Jan 2 - $0 Just $265M BTC being put to work as collateral >100x more BTC sitting idle

@SherryYanJiang tagging you / believing in you! @launchacoin $PEEK +Peek

The concept behind @believeapp is simple: it’s a the Kickstarter for ideas and projects. Here’s how it works: a founder or scout can tag an idea post with @launchacoin, which automatically creates a coin tied to that idea. The market then determines the coin’s fair value based on the size and importance of the problem being solved. For founders, it’s a way to gauge real market demand for their idea or project. If enough fees are generated, the founder can claim the earnings and immediately start building. For scouts, the goal is to discover the best ideas and founders on Twitter, tagging posts on their behalf. If the founder eventually builds the idea, scouts can earn a portion of the fees in perpetuity. We will see thousands of microapps solving niche problems through vibe coding and the opportunities too small for trad investors but perfect for @believeapp and its community to back.

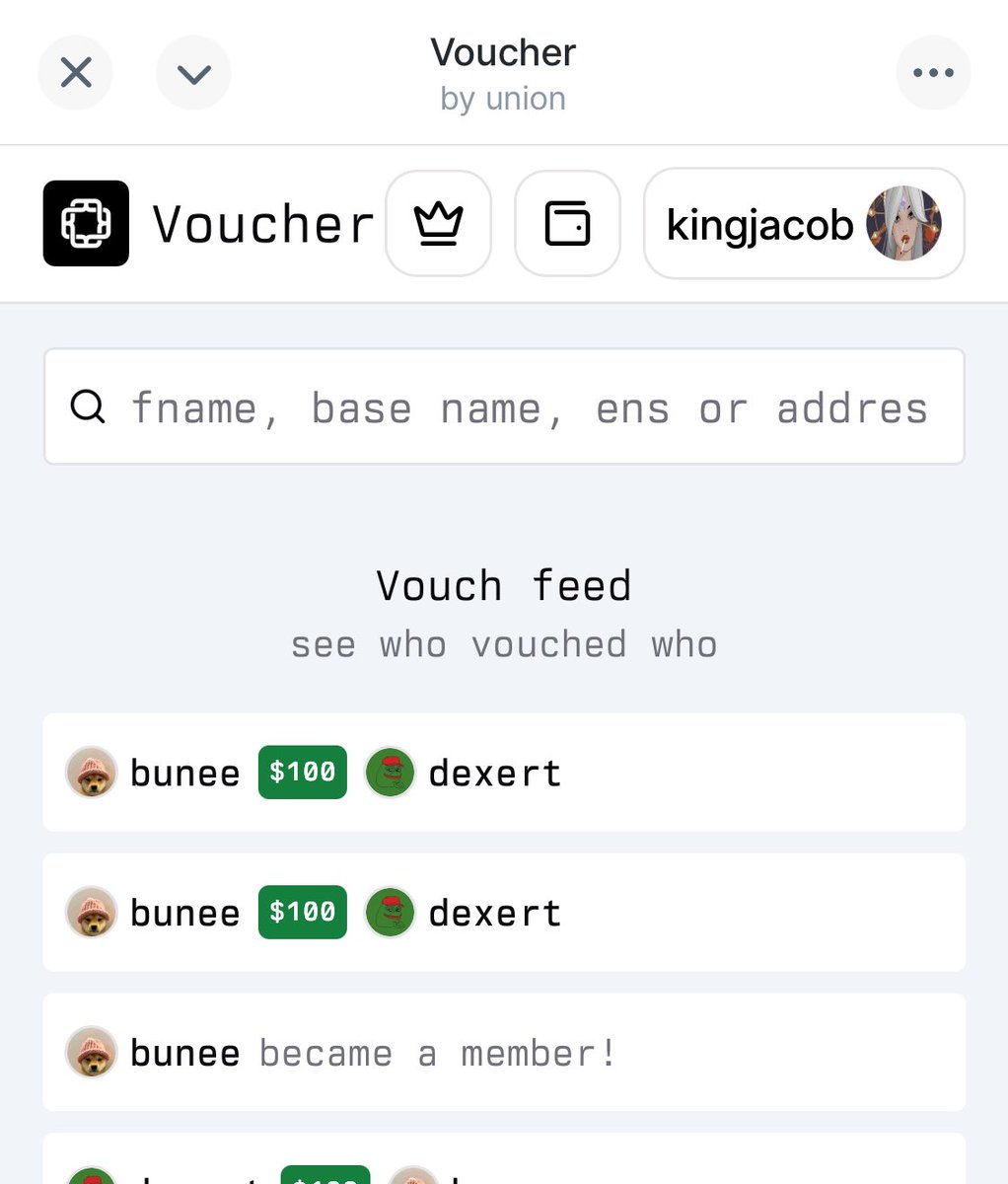

Union x @farcaster_xyz = Decentralized Social Credit If you’re on farcaster, you can now more easily vouch for your social graph using the voucher miniapp.