Sabitlenmiş Tweet

Odin

643 posts

Odin

@JoinOdin

launch and run your vc firm from your phone

anywhere Katılım Temmuz 2020

114 Takip Edilen2.1K Takipçiler

Odin retweetledi

This is true, and the obvious conclusion to anyone working with frontier AI capabilities on a regular basis sees that for many enterprises that would have required large human orgs in the past, the right number of employees beneath the CEO is tending toward 0.

Odin@JoinOdin

English

Odin retweetledi

AI-native startups are 25% smaller, half a seniority level flatter, and more expert-dense than non-AI startups in the same industry and cohort.

These are the findings of a recent paper by @hyunjinvkim and @orgRem, looking at @ycombinator startups versus a matched sample from @PitchBook.

Given the propensity of startups to grow quickly, and the internal frictions created by scale detailed in the article below, AI may already have a meaningful positive impact on startup quality.

Essentially, AI-native startups can run leaner for longer and with greater agility — giving them more room to “make something people want” without scaling prematurely.

Odin@JoinOdin

English

Odin retweetledi

The strangest thing about running Animal Syndication Company solo: AI hasn't just replaced headcount - it's made n=1 a structural advantage.

Managing a network this size, this way, wasn't possible before without dedicated people. Now it runs on something custom I built (graduated from @openclaw — thanks @mattfalconer_ for saving me from many vibecoding mistakes).

I spoke to @AndreRetterath about this recently: doing the same inside an org with n>1 means fighting complexities & red tape I simply don't have. The tooling exists. The org structures don't yet.

Someone will figure it out soon though.

Dan Gray@credistick

Research shows that venture capitalists benefit from broad networks (many connections), rather than deep networks (strong connections). This is probably because close relationships end up warping what should be rational, arms-length decisions. Analysis of VC networks by @murphcapital shows this network profile is a particular strength of solo/duo GPs, who have the most relationships per person. But how can such small teams manage large networks, and use them to create value for founders? Meet Wolfie, @enricomellis' cybernetic teammate (powered by @openclaw), who tracks which LPs might be able to help with particular founder requests.

English

Odin retweetledi

Research shows that venture capitalists benefit from broad networks (many connections), rather than deep networks (strong connections).

This is probably because close relationships end up warping what should be rational, arms-length decisions.

Analysis of VC networks by @murphcapital shows this network profile is a particular strength of solo/duo GPs, who have the most relationships per person.

But how can such small teams manage large networks, and use them to create value for founders?

Meet Wolfie, @enricomellis' cybernetic teammate (powered by @openclaw), who tracks which LPs might be able to help with particular founder requests.

Odin@JoinOdin

Our latest episode of Going Solo is with @enricomellis, founder of Animal Syndication Company, an early-stage investor truly doing things differently. His approach is unique, with no fund, and no fees. Instead, he works with founders to curate a pool of valuable, aligned investors on a deal-by-deal basis. And his investors aren't typical institutional LPs, either. More often, they are individuals investing capital earned from their own entrepreneurial success. In this episode, he spoke with @credistick about... 05:40 - Why he chose deal-by-deal investing 06:52 - Defining who the right LPs are 09:20 - Why angels may provide more support 12:44 - Differentiation in a crowded market 18:05 - Escaping the constraints of VC 23:15 - Why so many VCs suck at marketing 27:28 - Skin in the game with SPVs 33:14 - Hot deals versus good deals 36:36 - Lessons on using SPVs 41:25 - Shout-out to @andreasklinger 41:56 - Angel investing as a form of art collecting 46:40 - The world in ten years

English

Odin retweetledi

One of the silliest mistakes investors make is to confuse scale with success.

This is particularly common in venture capital, where investors have grown used to measuring incremental success as a factor of scale (valuation, revenue, users, etc) rather than progress toward an end state.

The single-minded pursuit of scale is a product of venture capital incentives, pushed by bad investors, and it results in far more failures than successes.

Outlier success stories are usually linked to outlier individual(s), and scale creates organisational entropy which competes with them for control.

This is why the "founder mode" renaissance followed the SaaS-bloat era, why so many rapidly-growing startups end up imploding, and why larger VC firms also see weaker performance.

The counter-intuitive conclusion is that scale should often be restrained to ensure a company makes real progress, rather than optimising for vanity metrics.

English

Odin retweetledi

we expect founders to do whatever it takes to sell…and then we decide we’re above doing it ourselves.

for people investing in a high-risk asset class, VCs take remarkably few risks with their own brand.

Dan Gray@credistick

Why are so many VCs bad at marketing? With some noteable exceptions*, most VC firms see themselves as gatekeepers of capital and therefore underestimate the value of differentiation. @enricomellis has strong views on this problem, and why VCs should risk crossing the chasm of cringe. (*see @imlaurieowen's recent article, linked below.)

English

Odin retweetledi

Why are so many VCs bad at marketing?

With some noteable exceptions*, most VC firms see themselves as gatekeepers of capital and therefore underestimate the value of differentiation.

@enricomellis has strong views on this problem, and why VCs should risk crossing the chasm of cringe.

(*see @imlaurieowen's recent article, linked below.)

Odin@JoinOdin

Our latest episode of Going Solo is with @enricomellis, founder of Animal Syndication Company, an early-stage investor truly doing things differently. His approach is unique, with no fund, and no fees. Instead, he works with founders to curate a pool of valuable, aligned investors on a deal-by-deal basis. And his investors aren't typical institutional LPs, either. More often, they are individuals investing capital earned from their own entrepreneurial success. In this episode, he spoke with @credistick about... 05:40 - Why he chose deal-by-deal investing 06:52 - Defining who the right LPs are 09:20 - Why angels may provide more support 12:44 - Differentiation in a crowded market 18:05 - Escaping the constraints of VC 23:15 - Why so many VCs suck at marketing 27:28 - Skin in the game with SPVs 33:14 - Hot deals versus good deals 36:36 - Lessons on using SPVs 41:25 - Shout-out to @andreasklinger 41:56 - Angel investing as a form of art collecting 46:40 - The world in ten years

English

Our latest episode of Going Solo is with @enricomellis, founder of Animal Syndication Company, an early-stage investor truly doing things differently.

His approach is unique, with no fund, and no fees.

Instead, he works with founders to curate a pool of valuable, aligned investors on a deal-by-deal basis.

And his investors aren't typical institutional LPs, either. More often, they are individuals investing capital earned from their own entrepreneurial success.

In this episode, he spoke with @credistick about...

05:40 - Why he chose deal-by-deal investing

06:52 - Defining who the right LPs are

09:20 - Why angels may provide more support

12:44 - Differentiation in a crowded market

18:05 - Escaping the constraints of VC

23:15 - Why so many VCs suck at marketing

27:28 - Skin in the game with SPVs

33:14 - Hot deals versus good deals

36:36 - Lessons on using SPVs

41:25 - Shout-out to @andreasklinger

41:56 - Angel investing as a form of art collecting

46:40 - The world in ten years

English

Odin retweetledi

5 months of Animal.

9 investments, just under $10M committed. Co-invested with @a16z , Sequoia, @pluralplatform , @singular__ . First follow-on closing now.

to my surprise: 80% of deal flow is inbound. My whole VC career it was outbound grind.

And AI is becoming the heart of the model, compensating for my lack of fees and team. Building the harness is a dark art (took a while to boil away the slop) but Animal is starting to look like what I wanted: a modern, AI-native syndication company.

Talked through all of it with @credistick on his podcast. Best writer on VC from a capital-markets lens imo

Dan Gray@credistick

The latest episode of Going Solo is with one of the rare early-stage investors who has dared to break from industry norms. @enricomellis runs Animal, a syndication company that curates individual LPs around investment opportunities. Enrico does not manage a fund, nor does he want to, and therefore does not charge fees. His success is tied to the founders he backs, and his LPs own returns. A fascinating conversation, and a brilliant investor. And if you've followed my writing on AI for solo GPs, ("The Macx Threshold"), the section on how he is using agents is particularly insightful.

English

Odin retweetledi

The latest episode of Going Solo is with one of the rare early-stage investors who has dared to break from industry norms.

@enricomellis runs Animal, a syndication company that curates individual LPs around investment opportunities.

Enrico does not manage a fund, nor does he want to, and therefore does not charge fees. His success is tied to the founders he backs, and his LPs own returns.

A fascinating conversation, and a brilliant investor.

And if you've followed my writing on AI for solo GPs, ("The Macx Threshold"), the section on how he is using agents is particularly insightful.

Odin@JoinOdin

Our latest episode of Going Solo is with @enricomellis, founder of Animal Syndication Company, an early-stage investor truly doing things differently. His approach is unique, with no fund, and no fees. Instead, he works with founders to curate a pool of valuable, aligned investors on a deal-by-deal basis. And his investors aren't typical institutional LPs, either. More often, they are individuals investing capital earned from their own entrepreneurial success. In this episode, he spoke with @credistick about... 05:40 - Why he chose deal-by-deal investing 06:52 - Defining who the right LPs are 09:20 - Why angels may provide more support 12:44 - Differentiation in a crowded market 18:05 - Escaping the constraints of VC 23:15 - Why so many VCs suck at marketing 27:28 - Skin in the game with SPVs 33:14 - Hot deals versus good deals 36:36 - Lessons on using SPVs 41:25 - Shout-out to @andreasklinger 41:56 - Angel investing as a form of art collecting 46:40 - The world in ten years

English

Odin retweetledi

Today we launch @ukdynamism, a new philanthropic fund to back the believers and builders in UK dynamism

I am delighted to be leading the fund, which is anchor funded by @xtxmarkets and is being incubated by @RenPhilanthropy

ukdynamism.fund

UK Dynamism Fund@ukdynamism

The UK can once again be the most dynamic country in the world. Today we launch the UK Dynamism Fund, a new philanthropic fund to support the believers and the builders of UK dynamism. Apply now: ukdynamism.fund

English

In venture capital, the cost of fees can be significantly reduced if LPs co-invest directly alongside VCs rather than investing solely through the fund.

As a result, LPs that build robust co-investment programs have been shown to significantly outperform those who delegate all investment activity to the GP.

This effect has been amplified considerably as private markets have expanded, with more mature companies raising larger and later funding rounds.

Odin@JoinOdin

English

Odin retweetledi

“Limited partners are more and more convinced that they have mistakenly believed that the boilerplate ‘two and twenty’ rule ensures a proper alignment of interest and incentives.”

Recasting Private Equity Funds after the Financial Crisis: The End of ‘Two and Twenty’ and the Emergence of Co-Investment and Separate Account Arrangements (2013)

Odin@JoinOdin

English

@DStrachman Honestly just big fan of the whole @JoinOdin crew

English

Dan is one of the few people who I think would make for an incredible fund of funds manager. Someone should anchor him and let him rip.

Dan Gray@credistick

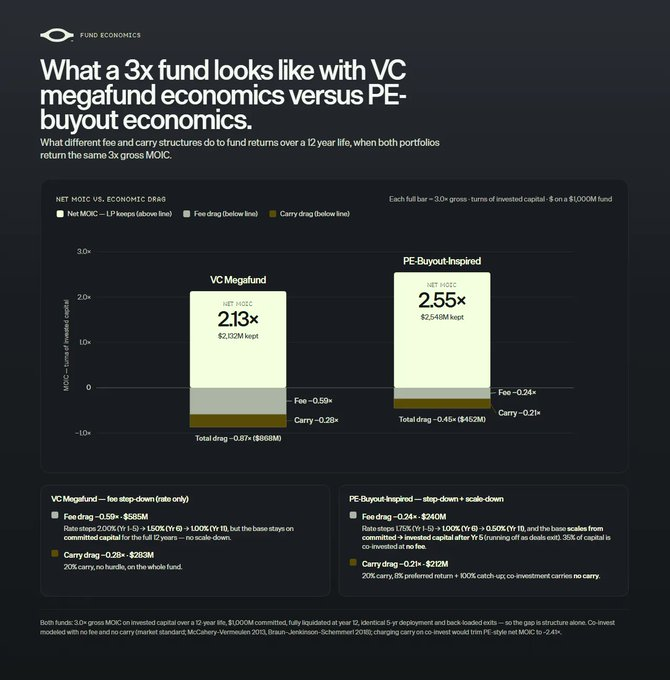

What's the difference between VC megafund economics, and PE buyout economics, on the assumption of $1B invested producing 3x gross MOIC? A loss of $416M, for the VC megafund LPs. In PE buyout, a larger share of capital is invested through low/no fee coinvestments, fees do not scale linearly, and there are more aggressive step-downs and scale-downs. Terms optimised for managing billions. In VC, the industry still largely operates on 2–2.5% on committed capital, with modest step-downs, and 20% carry with no hurdle. Economics intended for boutique firms, usually managing double-digit millions. With megafunds offering a scale and risk profile that is closer to PE buyout than traditional VC, with more capital going into relatively mature companies, there's a clear case to adapt the core terms. Simply by emulating reforms from the PE buyout strategy, megafund LPs would benefit from better alignment and a meaningful lift in performance. More importantly, it would curtail the mindless agglomeration incentivsed by linear fees, which is a structural contributor to poor performance, stagnant innovation and weak exit markets. It’s remarkably low-hanging fruit.

English

Odin retweetledi

What's the difference between VC megafund economics, and PE buyout economics, on the assumption of $1B invested producing 3x gross MOIC?

A loss of $416M, for the VC megafund LPs.

In PE buyout, a larger share of capital is invested through low/no fee coinvestments, fees do not scale linearly, and there are more aggressive step-downs and scale-downs. Terms optimised for managing billions.

In VC, the industry still largely operates on 2–2.5% on committed capital, with modest step-downs, and 20% carry with no hurdle. Economics intended for boutique firms, usually managing double-digit millions.

With megafunds offering a scale and risk profile that is closer to PE buyout than traditional VC, with more capital going into relatively mature companies, there's a clear case to adapt the core terms.

Simply by emulating reforms from the PE buyout strategy, megafund LPs would benefit from better alignment and a meaningful lift in performance.

More importantly, it would curtail the mindless agglomeration incentivsed by linear fees, which is a structural contributor to poor performance, stagnant innovation and weak exit markets.

It’s remarkably low-hanging fruit.

English

Subscribe to listen to future Going Solo episodes:

linktr.ee/goingsolowitho…

English

Electronics (1960s), biotech and personal computing (1980s), internet (1997-2000), clean energy (2004-2006), crypto (2016-2018), artificial intelligence (2022-?), and space (2026-?).

The cyclical boom and bust nature of venture capital is accelerating, as capital concentrates and is shifted more dramatically by market memetics.

Is this a sustainable reality for venture capital's LPs?

In a recent episode of Going Solo, @arian_ghashghai, GP at @EarthlingVC, reflected on LP's long-term appetite for this strategy.

English