kaung wong justin

147 posts

kaung wong justin

@Justin15647

BTC and Mining Stocks $IREN

Katılım Şubat 2022

2.6K Takip Edilen199 Takipçiler

Why digital nomads are rushing to Paraguay (and nobody's talking about it) 🇵🇾

While everyone's fighting for Portugal Golden Visas and Dubai residencies

Smart expats are quietly moving to Paraguay

The reason? Paraguay offers what most countries can't:

Residency in 60-90 days, with ZERO physical presence requirements after approval

But here's the part nobody tells you

You can maintain your Paraguay residency while living literally anywhere in the world

No mandatory stay. No annual visit requirements. Nothing

What you get:

✅ Temporary residency for 2 years + permanent after that

✅ Path to citizenship in 3 years

✅ 0% tax on foreign income (territorial taxation)

✅ Access to Mercosur (live/work in Argentina, Brazil, Uruguay)

✅ One of the cheapest residency processes in the world

No minimum income requirement, no local investment, nothing

Just show up and get your residency

The catch? You need to know the exact process... or you'll waste months dealing with bureaucracy

Want the complete Paraguay residency roadmap? DM me "PARAGUAY" 👇

English

@LEADER_TRADING wen deal, Mike will drink petrus tonight

English

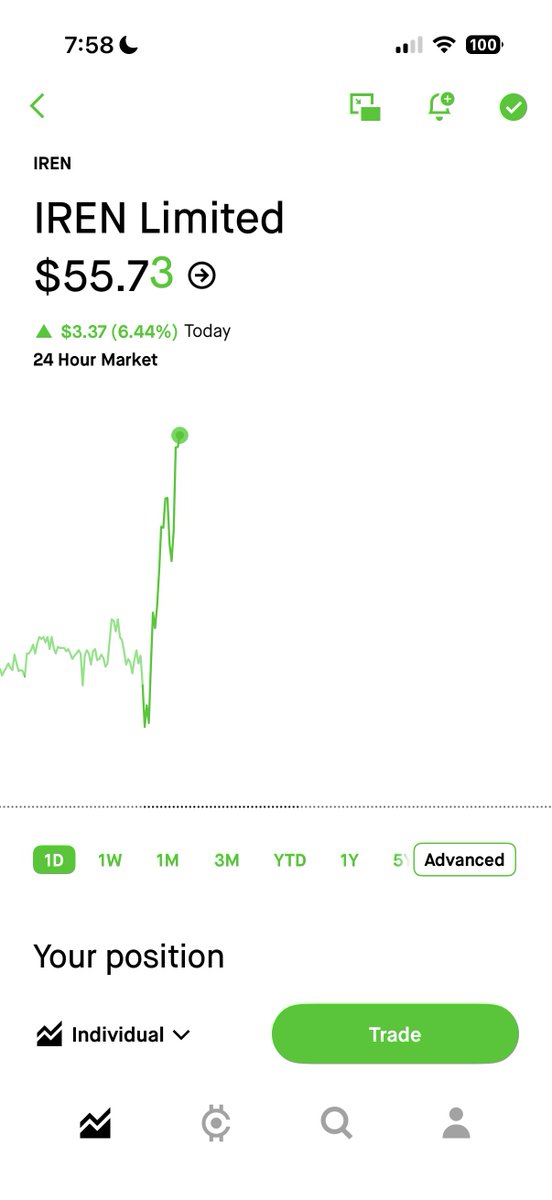

$IREN session so far… bit of an ascending tingle forming throughout the first 2 hours. Needs some stars to align across broader markets, but a $52.20 break when that happens could be really solid.

English

9 days until $IREN earnings on 2/5

sidebet: $10 to anyone in the comments if I'm right

Kevin Xu@kevinxu

This is INSANELY bullish. $IREN moved earnings up: Feb 11 → Feb 5. You don’t pull earnings up unless you’ve got good news. Last time: MSFT deal dropped 3 days before earnings. 14 days until 2/5. Bookmark this. Deal before earnings again?

English

🚨 HEATSEEKER GIVEAWAY 🚨

To celebrate 50K followers, I’m giving away 1 FREE month of Heatseeker to one lucky winner!

How to enter:

1) Follow me and @SkylitAI (the team behind Heatseeker)

2) Comment “HS” under this post

That’s it. In 24 hours, a giveaway bot will randomly pick the winner.

I’ll announce the results in a separate post.

Good luck to you all my friend. 🧡

Thank you all from the bottom of my heart for being here.

English

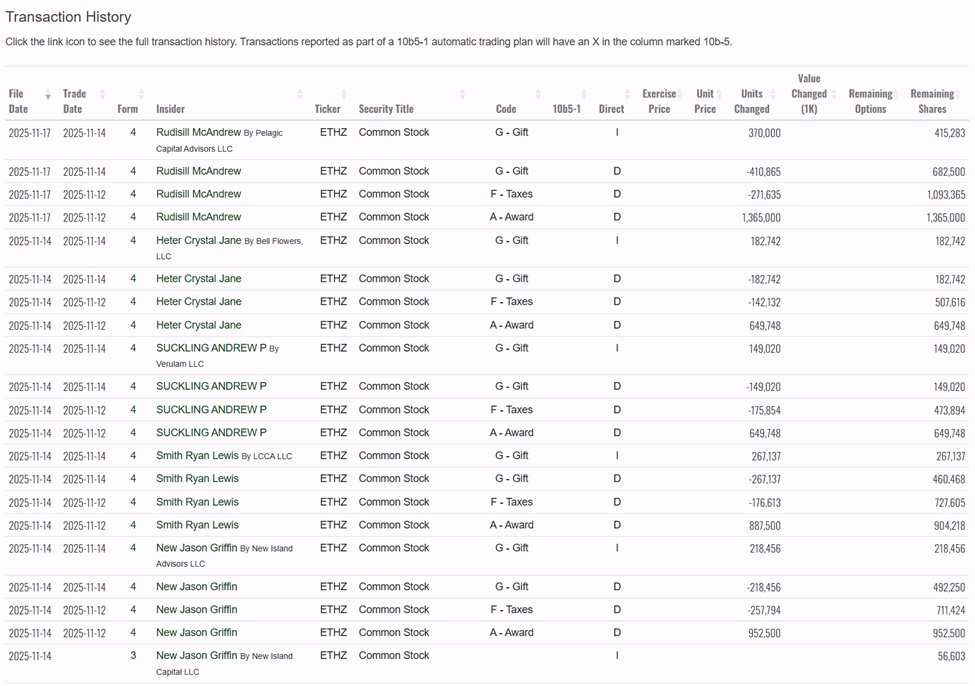

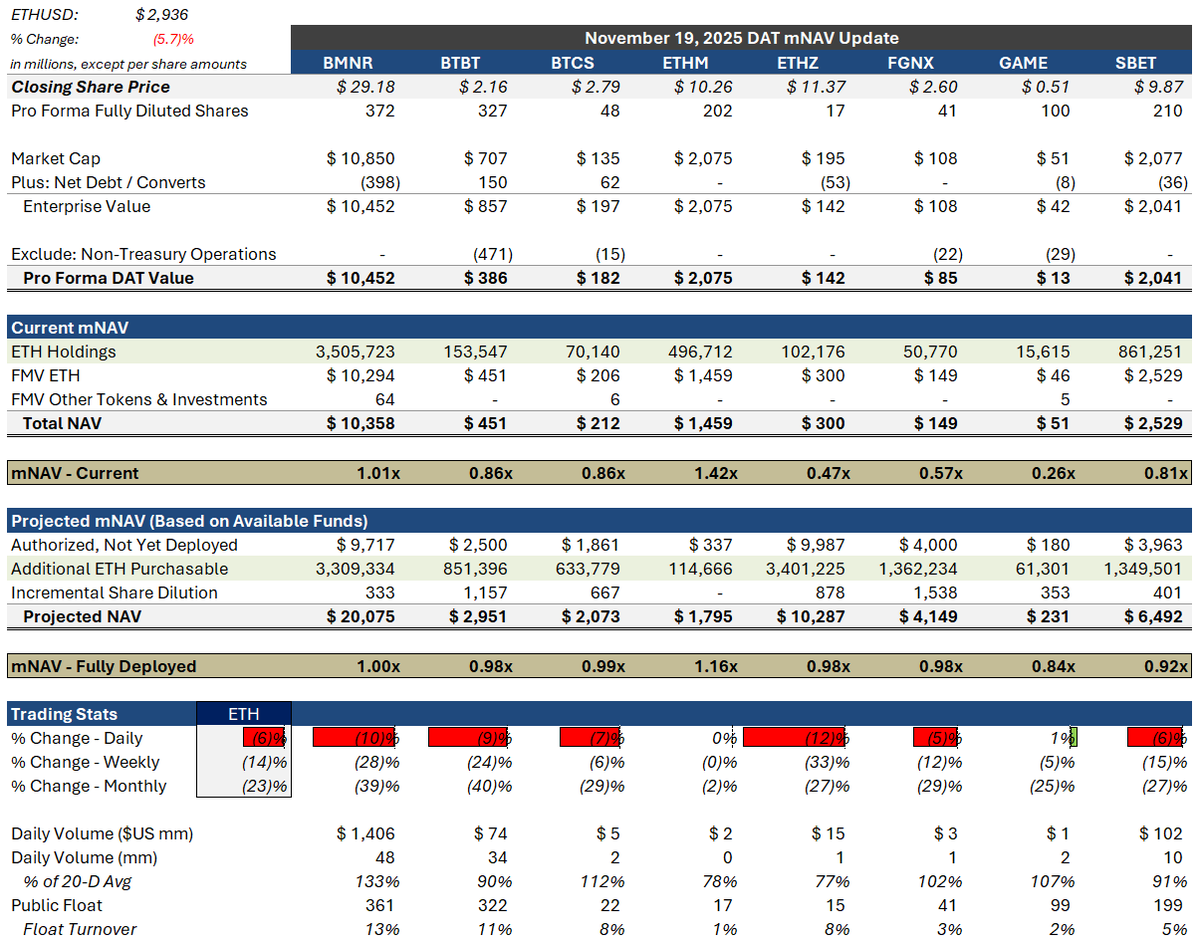

$BMNR $BTBT $BTCS $ETHM $ETHZ $FGNX $GAME $SBET

Daily DAT Update (Wed 11/19/25):

$BTBT reported last Friday. No new purchases since 11/7 but worth noting is that @SamirTabar said on the earnings call that no $WYFI shares will be sold in 2026.

$BMNR with a host of personnel updates since the last update. New CEO, 3 board members and a chartist added to payroll. Last ETH purchase was 11/10.

$ETHZ still getting whacked after a slew of insider transactions hit the tape recently (see attached). mNAV down to 0.5x.

First update in a few weeks. Earnings last week for most DATs a nothingburger. $MSTR now down 60% since July highs and mNAV approaching parity. Sentiment for DATs (and risk/momo assets) has shown no signs of improving. Unfortunately the DAT model simply doesn’t work when mNAV’s are near or below parity, so hands are tied for most. No buying of this dip.

All eyes on $NVDA tonight. In Jensen we trust.

English

Please remember that I could have accumulated closer to 2M shares under $1 if I waited a little longer to disclose my position.

Not everything is about personal profit. I want to see people win.

Mike Alfred@mikealfred

I am bidding for more ASST but I am concerned that unless BTC goes back under $100,000, it may be difficult to buy a large amount of shares under $1.30 going forward.

English

Removing some inactive members soon…

Comment your most bullish stock if you don’t want to be removed ⬇️

English

What you’re seeing with $IREN, in my opinion, has absolutely nothing to do with $BTC or it being a miner.

You’re finally seeing it start - yes, just START - to be found as an AI play. Which, if you’re long, is what YOU should view it as. The $BTC mining was / is an appetizer.

English

坏了,现在实时 ETH 价格已经跌破他的清算价格了😂

他的清算价格是 $1,836,不过预言机价格还在他的清算价格之上。就看 ETH 能不能在接下来快速反弹回来了,不然他的仓位快要开始清算了。

本文由 #Bitget|@Bitget_zh 赞助

余烬@EmberCN

6.5 万枚 ETH 处于清算边缘的巨鲸/机构,在 4 小时前从 Bitfinex 提出 2,000 ETH ($3.75M)、币安提出 154 万 USDT 补充抵押品和还款。将清算价格从 $1,932 下降到 $1,836。 这个价格仍然非常危险,现在 ETH 价格距离他的清算价格,仅有 $50 刀。 噢,对了。这个巨鲸/机构作为抵押品的 ETH 主要都是在 2022 年 5 月以循环贷方式买的,成本均价差不多 $2,088。目前亏损超过 $1400 万。 debank.com/profile/0xab7b… 本文由 #Bitget|@Bitget_zh 赞助

中文

Wait so Trump mentions a crypto reserve with SOL - XRP - and..........ADA, but no ETH?

Oi Vey!

GIF

English

@DNV99999 @danroberts0101 @mikealfred @GlennHarro @kentpdraper @danroberts0101 please make it happen!

English

I urge @danroberts0101 and Team $IREN to Improve IR Communication, and Communicate an AI Deal ASAP, because the market and Investors now Want Evidence that IREN is Capable of Making IMPORTANT AI DEALS with Hyperscalers and Large Corporations @mikealfred @GlennHarro @kentpdraper

𝐀𝐠𝐫𝐢𝐩𝐩𝐚 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭𝐬@Agrippa_Inv

$IREN has a serious problem... In this deep-dive post, I’ll shed light on $IREN's Achilles' heel: its Investor Relations (IR) & Communications Strategy. Although $IREN is one of the best-positioned data center companies in this AI-driven paradigm shift, its stock trades like a memecoin or a micro-cap penny stock. There is a serious disconnect between the company’s fundamentals and its share price. $IREN's executive management & IR team have done an incredibly poor job of controlling the narrative surrounding the company. This has been an ongoing issue for at least a year (since I started covering the stock), but it has become glaringly obvious in recent months. It’s now so out of hand that $IREN has drastically underperformed its $BTC mining peers during the recent $BTC sell-off—even though it has the highest operating margins and is the fastest-growing company in the segment. If anything, $IREN should be the stock least susceptible to these kinds of $BTC-driven pullbacks, given its industry-leading break-even point. I’m fully aware that no company has 100% control over its share price. Capital markets are dynamic and influenced by countless factors. However, having covered this stock extensively over the past year, I can see a massive misalignment between investor perception and reality. This misalignment has left a large gap for content creators like @FransBakker9812, @TheKamaHsutra, and myself to fill. Thanks to IREN’s weak IR strategy, there is huge demand from its retail investor community for explanations about IREN’s business model, its competitive moat, and the trajectory it’s on. But this issue isn’t just limited to retail investors. During the last earnings call, institutional investment analyst @StephenGlagola questioned the viability of IREN’s remote data center sites in West Texas for AI workloads—echoing a common narrative on X: "Remote sites aren’t viable for AI workloads. Only metropolitan sites are." Anyone who has spent a decent amount of time researching this topic knows this is completely false. The question should have been an easy layup for Co-CEO @danroberts0101 to refute and set the record straight. Instead, Dan appeared irritated by the question and didn’t even bother to give a comprehensive answer. He likely assumed everyone should already know better. The problem? They don’t. Yes, $IREN made an investor presentation last July highlighting its sites’ suitability for AI/HPC, but that was 8 months ago. You can’t expect to change a narrative with a single investor deck. IREN’s infrastructure is literally its biggest moat. Every earnings presentation, every investor update should hammer home the fact that its sites are AI/HPC-suitable. Every potential investor should know this. To make matters worse, executives from other aspiring AI/HPC companies like $BTBT, $MARA, $WULF and $CORZ are now actively spreading this false narrative about remote sites being unsuitable for AI. In my opinion, these companies can’t secure thousands or even hundreds of MWs and are instead forced to pick up smaller sites near metro areas. So they spin the narrative in their favor (credit to @TheKamaHsutra for pointing this out to me). The end result: Retail & institutional investors alike are starting to believe $IREN's 2.4-3 GW portfolio is worthless for AI/HPC. As someone who has spent hundreds, if not thousands, of hours studying & covering $IREN, this is beyond frustrating—because it’s entirely avoidable. The $1B ATM: A Self-Inflicted Wound 👇 Another massive overhang on the stock—undoubtedly a key factor in the severity of the recent sell-off—is the poorly communicated $1B ATM announcement. As recently as the prior earnings call, management signaled that dilution was largely over and that future capital needs would be met through debt, even mentioning potential shareholder distributions by late 2025. Then, just ~2 months later, $IREN dropped a $1B ATM, *potentially* diluting shareholders by well over 40% at these levels. The only explanation so far? "IREN needs to fund Horizon 1 (AI/HPC expansion), Sweetwater substation, and 2 additional EH/s (including ASIC upgrades), which together cost ~$500M." Meanwhile, the company is generating $20M-$25M in monthly cash flow even at these suppressed $BTC prices. So why the $1B ATM? Why not $400M or $500M? There’s a huge, unexplained gap. All we get from management is the vague excuse of "financial flexibility." Unsurprisingly, many investors assume the worst—that $IREN is recklessly using ATMs without regard for shareholder equity. Even institutional investors (that I'm in contact with) who reached out to IREN's IR department got the same lazy response: "financial flexibility" and "funding of additional growth initiatives." That’s not a sufficient justification for a potentially excessive capital raise. The Likely Truth about the ATM (That Should Have Been Communicated) 👇 I actually do think there’s a reasonable explanation for the ATM size. Multiple industry sources have pointed out that in today’s environment, proof of funds is a key factor in closing large-scale deals. It’s highly likely that the $1B ATM was structured this way as a show of capital strength to aid in negotiations. But if that’s the case, why wasn’t that clearly communicated? This is yet another case of poor IR strategy hurting shareholder goodwill. ❌ It’s incredibly frustrating because this is entirely avoidable. $IREN's fundamentals—both operational and financial—are exceptionally strong. Yet its IR team fails to capitalize on this. Most investors, especially in such a tech-heavy industry, aren’t well-versed enough to grasp IREN’s moat and growth potential on their own. It took me over 100+ hours of research to fully understand it—and almost none of that knowledge came from direct $IREN related sources. Investors shouldn’t have to do all the heavy lifting. It’s IREN’s job to set the tone and steer the narrative surrounding its company—just like every other public company does. Below, I break down three false narratives that are currently gaining traction and debunk them one by one (something IREN’s IR team should be doing).👇 On paper, $IREN is one of the best risk-adjusted opportunities in the market right now. Its infrastructure portfolio of 2.4 GW (soon likely to be 3 GW) alone is likely almost worth as much as the company's entire market cap of ~$1.75 billion (if it were to be sold). However, in my view, this gap between fair value and actual market cap is largely self-inflicted. $IREN needs to open a new chapter of strategic investor communication. There’s so much the company could do—from educational posts on X to detailed investor decks and presentations that clearly articulate their vision and the rationale behind their decisions. Right now, $IREN is underselling itself, and from the outside, it almost seems like they suffer from imposter syndrome. Having spoken to people inside the company and conducted extensive research, I know $IREN is the real deal. At their core, they are infrastructure developers—they excel at building massive greenfield sites from scratch at record speeds and designing cost-effective, power-dense data centers at scale. What they are not good at—at all—is selling their vision and technical competency to investors. And when a company relies on ATMs to raise capital, this becomes a critical issue. An undervalued company issuing new shares to fund growth faces a real opportunity cost in the form of excessive dilution. ❌ Co-CEO @danroberts0101 recently admitted to having made plenty of mistakes in the past, but he also emphasized that he and his brother are willing to adapt and change course when needed. That level of flexibility is one of the most valuable qualities a management team can have. I’m convinced now is the time to be nimble once again—to course-correct and address $IREN's IR shortcomings. And I’m not alone in this view. Every $IREN investor I’ve spoken to shares this concern. I’ve had discussions with institutional investors like @BCryptM, major shareholders such as @Umbisam and @litigious_dulce, and retail analysts including @FransBakker9812, @TheKamaHsutra, @benemodi, and plenty more—all of whom see the same glaring issue. I would go as far as to offer my help directly. I’m young, ambitious, and passionate about $IREN's future. If needed, I’d even consider relocating to Australia to work under Lincoln Tan, $IREN's Head of Investor Relations, helping to reshape and execute a stronger IR strategy. While I’m serious about this offer, I’d already be satisfied seeing $IREN take this feedback constructively and start moving in the right direction on this matter. Thank you for reading, cheers! 🤝

English

$IREN has a serious problem...

In this deep-dive post, I’ll shed light on $IREN's Achilles' heel: its Investor Relations (IR) & Communications Strategy.

Although $IREN is one of the best-positioned data center companies in this AI-driven paradigm shift, its stock trades like a memecoin or a micro-cap penny stock.

There is a serious disconnect between the company’s fundamentals and its share price.

$IREN's executive management & IR team have done an incredibly poor job of controlling the narrative surrounding the company. This has been an ongoing issue for at least a year (since I started covering the stock), but it has become glaringly obvious in recent months.

It’s now so out of hand that $IREN has drastically underperformed its $BTC mining peers during the recent $BTC sell-off—even though it has the highest operating margins and is the fastest-growing company in the segment. If anything, $IREN should be the stock least susceptible to these kinds of $BTC-driven pullbacks, given its industry-leading break-even point.

I’m fully aware that no company has 100% control over its share price. Capital markets are dynamic and influenced by countless factors. However, having covered this stock extensively over the past year, I can see a massive misalignment between investor perception and reality.

This misalignment has left a large gap for content creators like @FransBakker9812, @TheKamaHsutra, and myself to fill. Thanks to IREN’s weak IR strategy, there is huge demand from its retail investor community for explanations about IREN’s business model, its competitive moat, and the trajectory it’s on.

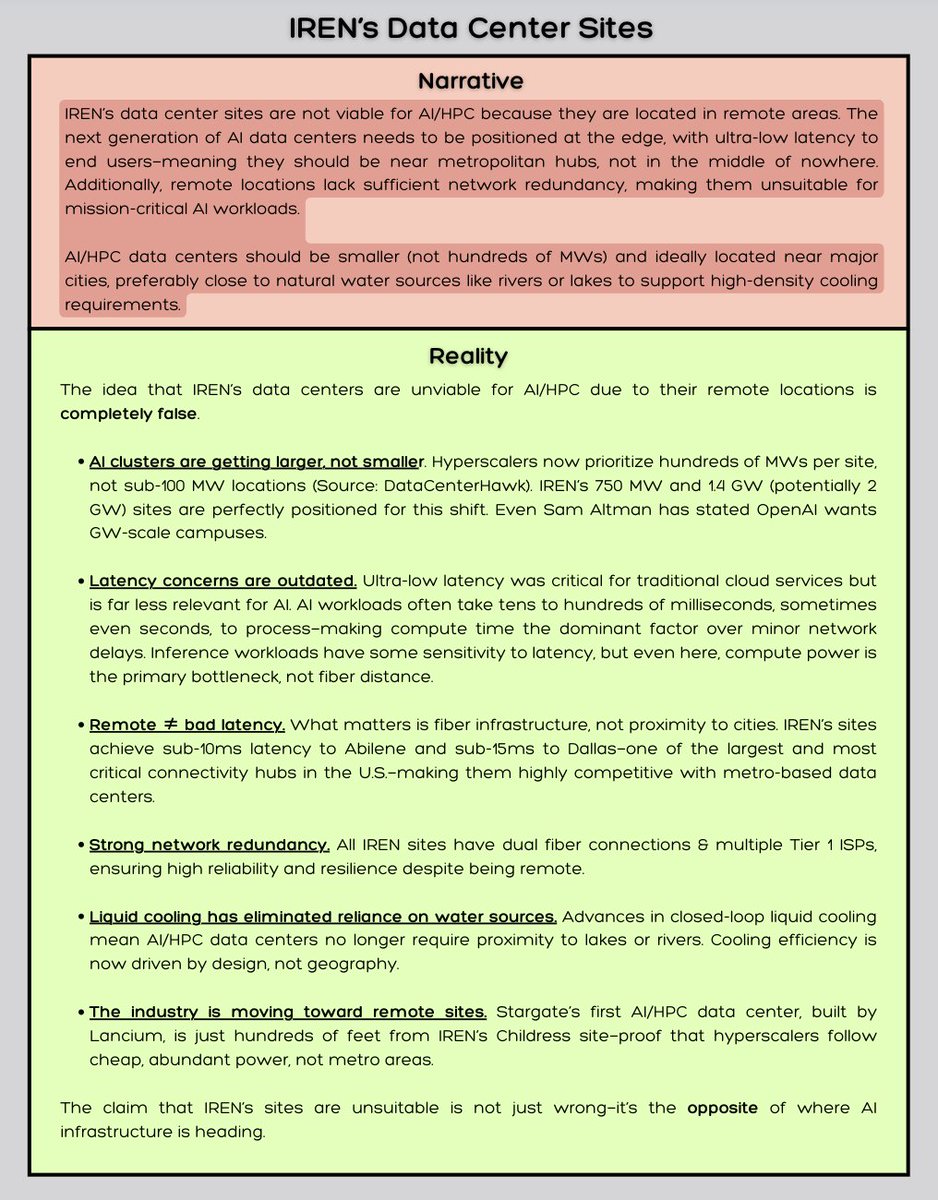

But this issue isn’t just limited to retail investors. During the last earnings call, institutional investment analyst @StephenGlagola questioned the viability of IREN’s remote data center sites in West Texas for AI workloads—echoing a common narrative on X:

"Remote sites aren’t viable for AI workloads. Only metropolitan sites are."

Anyone who has spent a decent amount of time researching this topic knows this is completely false.

The question should have been an easy layup for Co-CEO @danroberts0101 to refute and set the record straight. Instead, Dan appeared irritated by the question and didn’t even bother to give a comprehensive answer. He likely assumed everyone should already know better.

The problem? They don’t.

Yes, $IREN made an investor presentation last July highlighting its sites’ suitability for AI/HPC, but that was 8 months ago.

You can’t expect to change a narrative with a single investor deck. IREN’s infrastructure is literally its biggest moat. Every earnings presentation, every investor update should hammer home the fact that its sites are AI/HPC-suitable. Every potential investor should know this.

To make matters worse, executives from other aspiring AI/HPC companies like $BTBT, $MARA, $WULF and $CORZ are now actively spreading this false narrative about remote sites being unsuitable for AI.

In my opinion, these companies can’t secure thousands or even hundreds of MWs and are instead forced to pick up smaller sites near metro areas. So they spin the narrative in their favor (credit to @TheKamaHsutra for pointing this out to me).

The end result: Retail & institutional investors alike are starting to believe $IREN's 2.4-3 GW portfolio is worthless for AI/HPC.

As someone who has spent hundreds, if not thousands, of hours studying & covering $IREN, this is beyond frustrating—because it’s entirely avoidable.

The $1B ATM: A Self-Inflicted Wound 👇

Another massive overhang on the stock—undoubtedly a key factor in the severity of the recent sell-off—is the poorly communicated $1B ATM announcement.

As recently as the prior earnings call, management signaled that dilution was largely over and that future capital needs would be met through debt, even mentioning potential shareholder distributions by late 2025.

Then, just ~2 months later, $IREN dropped a $1B ATM, *potentially* diluting shareholders by well over 40% at these levels.

The only explanation so far?

"IREN needs to fund Horizon 1 (AI/HPC expansion), Sweetwater substation, and 2 additional EH/s (including ASIC upgrades), which together cost ~$500M."

Meanwhile, the company is generating $20M-$25M in monthly cash flow even at these suppressed $BTC prices.

So why the $1B ATM? Why not $400M or $500M?

There’s a huge, unexplained gap. All we get from management is the vague excuse of "financial flexibility." Unsurprisingly, many investors assume the worst—that $IREN is recklessly using ATMs without regard for shareholder equity.

Even institutional investors (that I'm in contact with) who reached out to IREN's IR department got the same lazy response: "financial flexibility" and "funding of additional growth initiatives."

That’s not a sufficient justification for a potentially excessive capital raise.

The Likely Truth about the ATM (That Should Have Been Communicated) 👇

I actually do think there’s a reasonable explanation for the ATM size. Multiple industry sources have pointed out that in today’s environment, proof of funds is a key factor in closing large-scale deals.

It’s highly likely that the $1B ATM was structured this way as a show of capital strength to aid in negotiations.

But if that’s the case, why wasn’t that clearly communicated? This is yet another case of poor IR strategy hurting shareholder goodwill. ❌

It’s incredibly frustrating because this is entirely avoidable. $IREN's fundamentals—both operational and financial—are exceptionally strong. Yet its IR team fails to capitalize on this.

Most investors, especially in such a tech-heavy industry, aren’t well-versed enough to grasp IREN’s moat and growth potential on their own.

It took me over 100+ hours of research to fully understand it—and almost none of that knowledge came from direct $IREN related sources.

Investors shouldn’t have to do all the heavy lifting. It’s IREN’s job to set the tone and steer the narrative surrounding its company—just like every other public company does.

Below, I break down three false narratives that are currently gaining traction and debunk them one by one (something IREN’s IR team should be doing).👇

On paper, $IREN is one of the best risk-adjusted opportunities in the market right now. Its infrastructure portfolio of 2.4 GW (soon likely to be 3 GW) alone is likely almost worth as much as the company's entire market cap of ~$1.75 billion (if it were to be sold).

However, in my view, this gap between fair value and actual market cap is largely self-inflicted. $IREN needs to open a new chapter of strategic investor communication.

There’s so much the company could do—from educational posts on X to detailed investor decks and presentations that clearly articulate their vision and the rationale behind their decisions. Right now, $IREN is underselling itself, and from the outside, it almost seems like they suffer from imposter syndrome.

Having spoken to people inside the company and conducted extensive research, I know $IREN is the real deal. At their core, they are infrastructure developers—they excel at building massive greenfield sites from scratch at record speeds and designing cost-effective, power-dense data centers at scale.

What they are not good at—at all—is selling their vision and technical competency to investors. And when a company relies on ATMs to raise capital, this becomes a critical issue. An undervalued company issuing new shares to fund growth faces a real opportunity cost in the form of excessive dilution. ❌

Co-CEO @danroberts0101 recently admitted to having made plenty of mistakes in the past, but he also emphasized that he and his brother are willing to adapt and change course when needed. That level of flexibility is one of the most valuable qualities a management team can have.

I’m convinced now is the time to be nimble once again—to course-correct and address $IREN's IR shortcomings.

And I’m not alone in this view. Every $IREN investor I’ve spoken to shares this concern. I’ve had discussions with institutional investors like @BCryptM, major shareholders such as @Umbisam and @litigious_dulce, and retail analysts including @FransBakker9812, @TheKamaHsutra, @benemodi, and plenty more—all of whom see the same glaring issue.

I would go as far as to offer my help directly.

I’m young, ambitious, and passionate about $IREN's future. If needed, I’d even consider relocating to Australia to work under Lincoln Tan, $IREN's Head of Investor Relations, helping to reshape and execute a stronger IR strategy.

While I’m serious about this offer, I’d already be satisfied seeing $IREN take this feedback constructively and start moving in the right direction on this matter.

Thank you for reading, cheers! 🤝

English

@LEADER_TRADING Anyway still holding and can only do so at the moment.

English

and again - this thing has been so random, and more or less, correlates with NOTHING at times. Mind of its own. For all we know $8 bottoms and it is back pushing $12+ by mid march.

That’s the beauty of the market. NO ONE knows 🤷🏽♂️

LEADER TRADING @LEADER_TRADING

my unfortunate OPINION; the past 7 days have essentially destroyed the $IREN bullish case for the short to mid term timeline. Only things to be relatively optimistic about are low RSI and historically random behavior of the stock in general, which is basically “fingers crossed”.

English

@LEADER_TRADING 5 days drop 40% without breathing is so frustrating, just hope it won’t turn into 60% drop like last summer. Luckily there is a daily gap around $10, so at least it will go back in the near future. The main problem of Iren is there is all talk but no real deal.

English

@LEADER_TRADING Totally agree, sad to see so brutal sell off

English

my unfortunate OPINION; the past 7 days have essentially destroyed the $IREN bullish case for the short to mid term timeline.

Only things to be relatively optimistic about are low RSI and historically random behavior of the stock in general, which is basically “fingers crossed”.

English

I write what I feel. And I’d have voted for Trump. He’s the least worse. Certainly not the best American. I personally have tons of US friends who are 100x better - smarter & more moderate - than him.

Only an idiot can think - let alone publicly propose - to move 2mil people away from their land while concurrently claiming day in day out peace in the Middle East.

On the Ukraine crisis - I still don’t understand his plan. One day he says A … the day after Z. We’ll see what happens tomorrow.

English