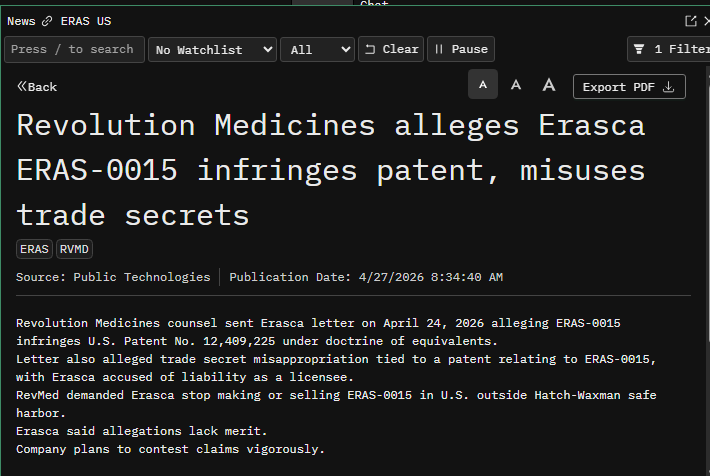

@keisan_15 $rvmd sues $eras arguing they have the same molecule. $eras present safety concerns. $rvmd 😶🌫️

English

personofinterest

229 posts

Putting criticism about timing and data presentation aside, $ERAS' ERAS-0015 seems very similar to $RVMD's daraxonrasib imo. ERAS-0015 is more potent which explains the lower exposure required for efficacy (and associated with on target toxicity of course). It might have a slight advantage on GI side effects (to be seen) but other than that it is likely to have a similar therapeutic index. If we compare just the PDAC data sets, $ERAS reported 4 PRs in 21 patients (~19% ORR) in the US at relevant doses which is lower than dara's 35% ORR but that gap will likely close with more follow up as $ERAS has multiple near PRs at the first scan than can convert in the future (They need 3 such conversions to reach 33% ORR). The limited follow up probably has a confounding effect on safety as well (longer treatment typically leads to more side effects) which should take $ERAS to a similar dose interruption/reduction rate in the future. Gr5 pneumonitis case requires attention but it could be an isolated case. Is $ERAS cheap at $3B? Not sure but for pharmas who cannot afford or simply won't get $RVMD this is the closest fast follower program that could be P3 ready later this year. *no position in stocks mentioned *

Mizuho⬆️the PT on $RVMD to $185 from $!40, reiterated at Outperform, and said that it now models 2035🌐risk-adj'd PDAC revenue of $14B. $IMRX ERAS TGNX ANL VSTM $BBOT Mizuho said in its note: Following last week's unprecedented survival benefit from RASolute 302 of daraxonrasib in 2L pancreatic cancer (PDAC), and now updated data for daraxonrasib (+/- GnP) in 1L PDAC, we raise our PT to $185 from $140 as we take up our PDAC PoS (80% -- >90%) and accelerate the trajectory of adoption in 1L/2L PDAC. While updated 1L PDAC didn't provide PFS/OS curves (immature with medians not reached), 6-month landmark analyses for both regimens compare very favorably to historical GnP (see pages 3 and 4 for data comps). Together with the performance of daraxonrasib in 2L, we see the opportunity in 1L PDAC and the now ongoing RASolute 303 study as extremely well-positioned and supportive of the now $14B we model in risk-adjusted 2035 WW PDAC revenues. Reiterate Outperform.

$RVMD is a buy for long term investors

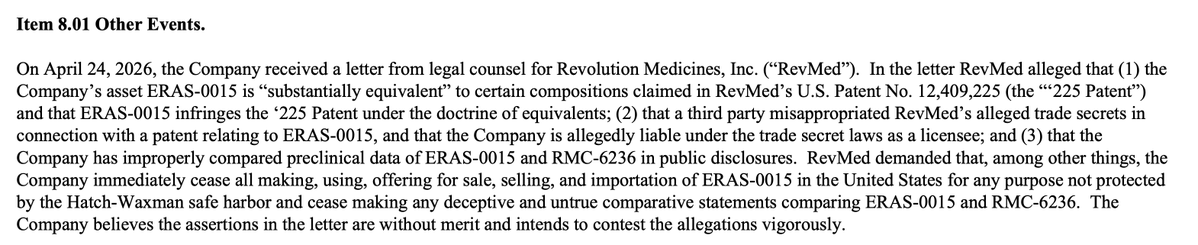

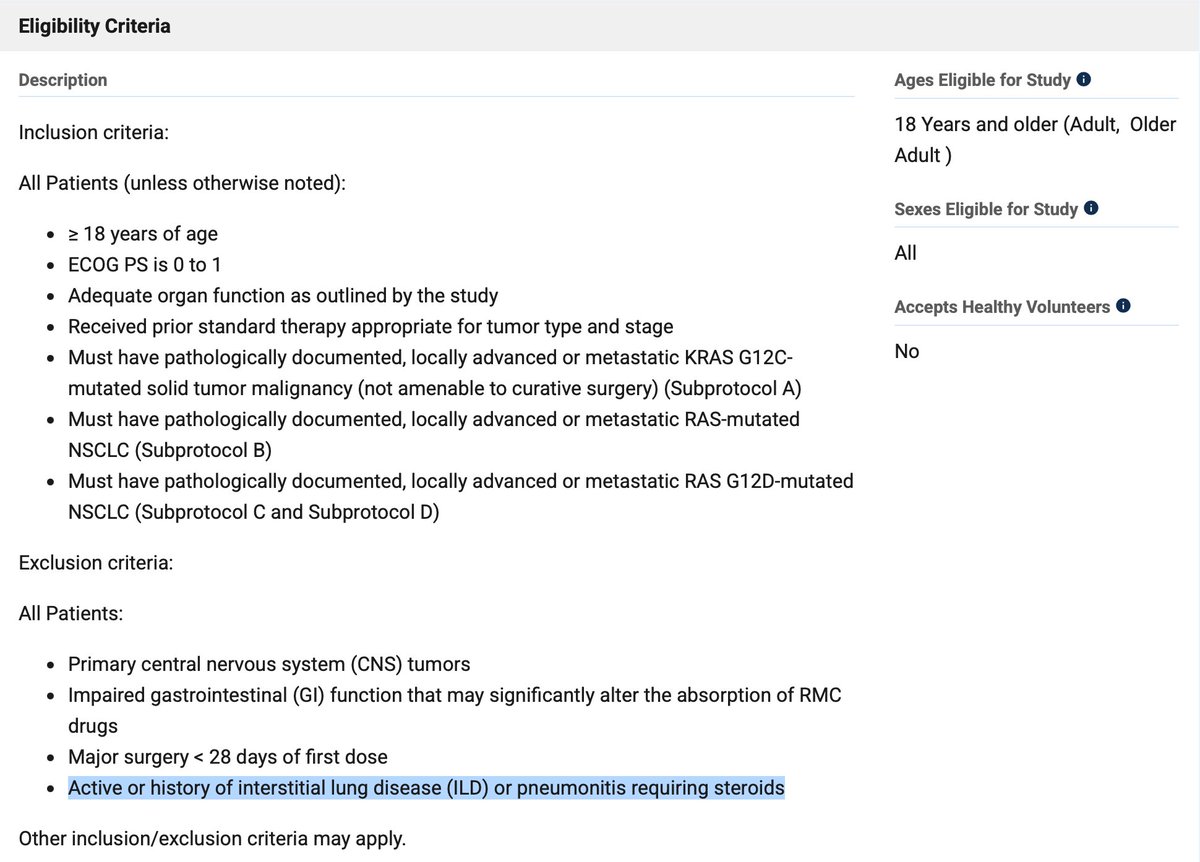

To be fair to $ERAS, $RVMD also reported a grade 4 pneumonitis in the footnote. sec.gov/Archives/edgar…

$ERAS this is why I never trade biotech stocks, no matter how good the chart looks -42% in premarket on a treatment-related death