Les Blake

646 posts

Les Blake

@LesBlake

I help founders and investors build companies. Fractional CFO | Startup Advisor | Founder Tools & frameworks here: https://t.co/3TWnbsvOo2

The Interwebs Katılım Şubat 2009

759 Takip Edilen146 Takipçiler

Just got a job application from someone's dad.

"I would like to submit a job application on behalf of my son"

That is a first.

English

@BskiMike22802 “You do not get to set market conditions and then be surprised by market outcomes.” - Applies to so much more than dating.

English

Kathleen Kennedy is officially leaving Lucasfilm after 14 years.

This will be her last week as head of the studio

English

Oatmeal (and I think that’s rice and sourdough) made the cut! In all seriousness, assuming overall calories are kept in check and people exercise & get sun(day)light, this looks spot on. Maybe up the veggies a bit, add low sugar fermented foods like sauerkraut & this is great.

The White House@WhiteHouse

BREAKING: The Trump Administration announces the 2025-2030 Dietary Guidelines for Americans, putting REAL FOOD back at the center of health. 🇺🇸 REALFOOD.GOV

English

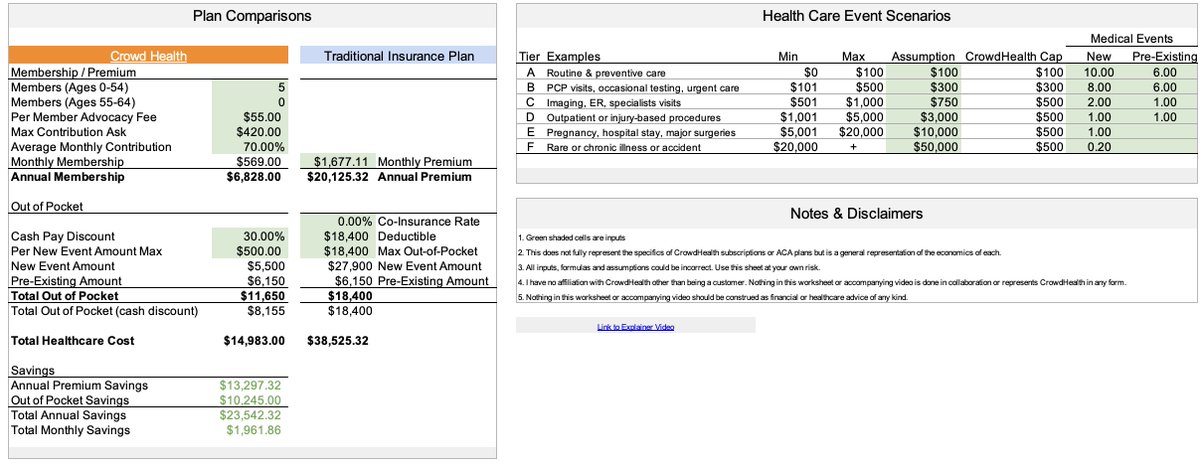

Tomorrow is Halloween but the real nightmare begins November 1st when healthcare open enrollment begins.

My wife and I are business owners who pay for our own healthcare but we will be making a big change this year.

If you’re a freelancer, business owner or someone who pays for their own health insurance read on:

Our premiums, deductibles and maximum out-of-pocket limits have increased +20% per year and will likely be higher in 2026.

For a family of five we pay $20k+ per year in premiums with a deductible and an out-of-pocket max almost as high.

I have been following @JoinCrowdHealth, a crowd sharing plan, for a few years but wasn’t sure if their model would work for us.

Disclaimer: I have no affiliation with nor do I represent CrowdHealth in any capacity.

Healthshare plans like CrowdHealth can be hard to compare apples-to-apples against traditional insurance, so I built a simple spreadsheet tool that helped me analyze the differences between:

• Monthly premiums vs. contributions

• Deductibles vs. shared amounts

• Coverage limits and exclusions

• Annual out-of-pocket costs based on specific scenarios

By my analysis we should be able to cut our healthcare expenses 30% to 50% by joining CrowdHealth.

If you’re not familiar with crowd sharing plans, they’ve been around for a long time.

The basics for CrowdHealth’s model:

• You pay monthly subscription + share amount instead of a premium

• You pay for the first $500 of any procedure

• Pre-existing conditions are excluded for 2 years but capped after

• They help you negotiate potentially significant cash pay discounts

My analysis gave us clarity in analyzing the differences and confidence in deciding to make the switch.

Every situation is unique, but I wanted to create a tool that makes a confusing topic a little clearer.

👉 Comment “Health” and I’ll send you the spreadsheet that includes a short walkthrough video.

English

@Jayyanginspires Exactly right. The scariest part is most don’t realize they’re at a Local Maxima.

making-the-leap.com/p/local-maxima

English

@nateliason @JoinCrowdHealth Same here @nateliason. Interested to hear how you came to the conclusion. Here was mine 👇🏼

x.com/lesblake/statu…

Les Blake@LesBlake

Tomorrow is Halloween but the real nightmare begins November 1st when healthcare open enrollment begins. My wife and I are business owners who pay for our own healthcare but we will be making a big change this year. If you’re a freelancer, business owner or someone who pays for their own health insurance read on: Our premiums, deductibles and maximum out-of-pocket limits have increased +20% per year and will likely be higher in 2026. For a family of five we pay $20k+ per year in premiums with a deductible and an out-of-pocket max almost as high. I have been following @JoinCrowdHealth, a crowd sharing plan, for a few years but wasn’t sure if their model would work for us. Disclaimer: I have no affiliation with nor do I represent CrowdHealth in any capacity. Healthshare plans like CrowdHealth can be hard to compare apples-to-apples against traditional insurance, so I built a simple spreadsheet tool that helped me analyze the differences between: • Monthly premiums vs. contributions • Deductibles vs. shared amounts • Coverage limits and exclusions • Annual out-of-pocket costs based on specific scenarios By my analysis we should be able to cut our healthcare expenses 30% to 50% by joining CrowdHealth. If you’re not familiar with crowd sharing plans, they’ve been around for a long time. The basics for CrowdHealth’s model: • You pay monthly subscription + share amount instead of a premium • You pay for the first $500 of any procedure • Pre-existing conditions are excluded for 2 years but capped after • They help you negotiate potentially significant cash pay discounts My analysis gave us clarity in analyzing the differences and confidence in deciding to make the switch. Every situation is unique, but I wanted to create a tool that makes a confusing topic a little clearer. 👉 Comment “Health” and I’ll send you the spreadsheet that includes a short walkthrough video.

English

Writing a (very) in-depth post on why I canceled my family's health insurance and switched to @JoinCrowdHealth

Anyone have questions? Will be sure to answer them.

English

@tnickgranger Looks like your DMs are off so I can’t send the link. DM me “health” and I’ll send it over.

English

Les Blake@LesBlake

Tomorrow is Halloween but the real nightmare begins November 1st when healthcare open enrollment begins. My wife and I are business owners who pay for our own healthcare but we will be making a big change this year. If you’re a freelancer, business owner or someone who pays for their own health insurance read on: Our premiums, deductibles and maximum out-of-pocket limits have increased +20% per year and will likely be higher in 2026. For a family of five we pay $20k+ per year in premiums with a deductible and an out-of-pocket max almost as high. I have been following @JoinCrowdHealth, a crowd sharing plan, for a few years but wasn’t sure if their model would work for us. Disclaimer: I have no affiliation with nor do I represent CrowdHealth in any capacity. Healthshare plans like CrowdHealth can be hard to compare apples-to-apples against traditional insurance, so I built a simple spreadsheet tool that helped me analyze the differences between: • Monthly premiums vs. contributions • Deductibles vs. shared amounts • Coverage limits and exclusions • Annual out-of-pocket costs based on specific scenarios By my analysis we should be able to cut our healthcare expenses 30% to 50% by joining CrowdHealth. If you’re not familiar with crowd sharing plans, they’ve been around for a long time. The basics for CrowdHealth’s model: • You pay monthly subscription + share amount instead of a premium • You pay for the first $500 of any procedure • Pre-existing conditions are excluded for 2 years but capped after • They help you negotiate potentially significant cash pay discounts My analysis gave us clarity in analyzing the differences and confidence in deciding to make the switch. Every situation is unique, but I wanted to create a tool that makes a confusing topic a little clearer. 👉 Comment “Health” and I’ll send you the spreadsheet that includes a short walkthrough video.

English

I'm thinking about dropping my insurance and doing this.

Paul Millerd@p_millerd

I haven't had insurance in the US for 2.5 years. I joined @JoinCrowdHealth myself for a year and then added my wife and daughter 1.5 years ago. The model is so simple it makes you question the entire existing system I'm very impressed and its actually beautiful seeing people's bills and knowing what youre helping. I've also written extensively how I've hacked the healthcare system in dozens of ways over the past 7+ years all while having ongoing chronic issues that have been confusing. This fits well with that approach although sometimes you definitely waste a lot of money but you do it on providers, not on an insurance membership program Recently they just knocked 10% off my monthly bill for having good blood test results. They also are funding DEXA scans. It's wild being part of a program that wants you to be healthy, not just participating in a insurance program thats bloated, deployed by powerless front people, and has to operate in deeply embedded incentives that are nearly impossible to change I'm pretty sure you get a discount for a few months using this code but even if you dont definitely worth checking out joincrowdhealth.com/?referral_code…

English

@Elenion88 Looks like your DMs are closed. Send me a quick DM that says "health" and I will reply with the link.

English

@captnwaffles17 Looks like your DMs are closed. Send me a quick DM that says "health" and I will reply with the link.

English

@AJA_Cortes It’s ridiculous. My take👇🏼

x.com/lesblake/statu…

Les Blake@LesBlake

Tomorrow is Halloween but the real nightmare begins November 1st when healthcare open enrollment begins. My wife and I are business owners who pay for our own healthcare but we will be making a big change this year. If you’re a freelancer, business owner or someone who pays for their own health insurance read on: Our premiums, deductibles and maximum out-of-pocket limits have increased +20% per year and will likely be higher in 2026. For a family of five we pay $20k+ per year in premiums with a deductible and an out-of-pocket max almost as high. I have been following @JoinCrowdHealth, a crowd sharing plan, for a few years but wasn’t sure if their model would work for us. Disclaimer: I have no affiliation with nor do I represent CrowdHealth in any capacity. Healthshare plans like CrowdHealth can be hard to compare apples-to-apples against traditional insurance, so I built a simple spreadsheet tool that helped me analyze the differences between: • Monthly premiums vs. contributions • Deductibles vs. shared amounts • Coverage limits and exclusions • Annual out-of-pocket costs based on specific scenarios By my analysis we should be able to cut our healthcare expenses 30% to 50% by joining CrowdHealth. If you’re not familiar with crowd sharing plans, they’ve been around for a long time. The basics for CrowdHealth’s model: • You pay monthly subscription + share amount instead of a premium • You pay for the first $500 of any procedure • Pre-existing conditions are excluded for 2 years but capped after • They help you negotiate potentially significant cash pay discounts My analysis gave us clarity in analyzing the differences and confidence in deciding to make the switch. Every situation is unique, but I wanted to create a tool that makes a confusing topic a little clearer. 👉 Comment “Health” and I’ll send you the spreadsheet that includes a short walkthrough video.

English

Cost of health insurance is out of control

$2-4k+ a month

And unless youre visiting the doctor constantly, its money paid out that essentially unused and lost

-Dont care about the "its for an EMERGENCY" lecture

Youd get better ROI on hiring a concierge doctor team and optimizing your familys health

English

I would rather the government print money than tax me. What would you rather - Printing or taxes? Why?

English