@egr_investor @OptimizedPort AVGE would be better. You can just own the profitable ones and remove the unprofitable ones.

English

Masters of Fintwit

8.8K posts

@MFintwit

Trapped on the third rock from the sun with billions of people suffering from Dunning-Kruger effect.

Fed Chair Powell says U.S. private sector job growth is essentially ZERO “Golden age”

BREAKING: Law firm Kirkland is defying the private equity slowdown with a record $11.1 million partner pay for 2025. Kirkland became the first law firm to break $10 billion in annual revenues last year, advising on more than $800 billion of M&A deals in 2025.

The industry buzz is all about the threats of fee-compression (from tech, from AI, from, from, from...), and even more so for advisors who charge standalone planning fees for services (as opposed to AUM fees). Yet in practice, AdvicePay report finds amongst advisors themselves, 54% plan to keep their fees steady, 45% plan to RAISE fees, and only 0.50% of plans to decrease their fees. Median subscription fee is $291/month (which adds up to ~$3,500/year, or very similar to the minimum fee/asset requirements of AUM firms anyway), as demand for advisors who charge planning fees continues to rise... "AdvicePay Report: Fee-For-Service No Longer a Niche Model" kitc.es/3NGWJYl

Here is what a tax like this does: 1) It excites people with zero agency and infinite envy. Beware of these people. 2) It will keep middle class people firmly in the middle class with no real chance of getting wealthy if they stay in Washington State. It should be clear that this IS the strategy. Learned helplessness of the electorate will keep Washington State’s current elected officials in office. 3) It will never allow the upwardly mobile of building any assets or real wealth unless they move. Capping the American Dream is a dystopian and malevolent scheme. It cannot be a valid strategy. But unless droves of middle and upper middle class people leave Washington State, this strategy will win.

Excellent guide for those receiving RSU income. I currently receive over 70% of my labor income via RSUs. As always, my preferred policy is to “sell all” and immediately reallocate to a multi-factor portfolio. #Tech #RSU #Investing #PersonalFinance

Imagine paying taxes on vested RSUs at $120 and it falls by 75% by the time lockup ends.

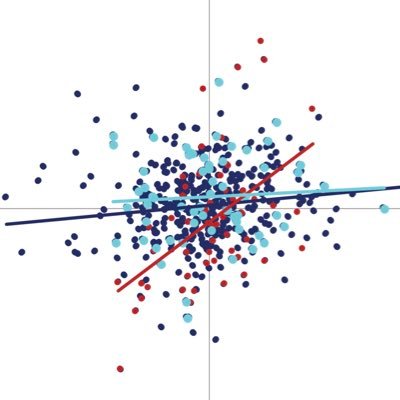

I created a tool to visualize your sequence risk in a portfolio. We talk a lot about the "efficient frontier", but the EF turns investing into a performance chasing and alpha optimization problem. The average investor doesn't care about this (and most active managers can't find it in the first place). The average investor wants to know their TEMPORAL risks across the portfolio. "When can I pay for X?" The Defined Duration Frontier flips the conversation from one about portfolio optimization to sequence risk mitigation thereby helping people understand how their asset allocation actually helps them understand the temporal risks within the portfolio.

I have zero doubt now that the private credit, private equity, and all things private have burst. There cannot be anyone out there who isn't trying to get to the exits. If there is, tee them up for a Darwin Award. cc @spomboy

Private credit executives say don’t worry about private credit, “handful of isolated incidents” “Scott McClurg, head of private credit at HSBC Asset Management, felt the headlines highlighting concerns about private credit were overly focused on a handful of isolated cases. “The catalyst for the media coverage we have seen has been idiosyncratic illegal activities within a very small number companies,” Mr McClurg said, adding that four names had shaped media and public perceptions…” “There isn’t any evidence of a wide or systemic issue.”….” royalgazette.com/reinsurance/bu…

this is a disaster *CLIFFWATER $33 BLN PRIVATE CREDIT FUND Q1 REDEMPTIONS REACH 14% And Cliffwater is interval, meaning it is not permitted to impose gates