Maor Riven

1.5K posts

דיילה על עתידו במכבי ת״א: ״אני פתוח וחיובי להישארות במכבי. נראה אם נמצא פתרון, כי המצב במדינה (האפשרות לסבב נוסף מול איראן) משפיע על המשפחה שלי שחיה במקום אחר, צריך לראות איך אפשר לבצע תיאום ציפיות בנושא. יש לי חוויה חיובית מכולם פה ואני אופטימי אבל אין לי תשובה ודאית לתת לכם״.

עברית

@dvir_luzon אתה מדבר על תקיעת אצבע בעין? מצביעי ביבי יכרתו לעצמם איבר אם ידעו שזה יכאיב למי שהם תופסים כשמאלני

עברית

התוצאות מהונגריה הן גלולה מרה למי שקיווה לשינוי אחר, אבל יש כאן שיעור פוליטי שאסור להתעלם ממנו.

כמה תובנות על הניצחון של פיטר מאדיאר והמשמעות לישראל:

1. הניצחון הוא לא "שמאלה", הוא "נגד". העם ההונגרי לא התעורר פתאום ליברל. הוא נשאר שמרן, הוא עדיין מתנגד להגירה.

מאדיאר ניצח כי הוא היה חכם מספיק לא לגעת בערכים האלו.

הוא לא עשה קמפיין בעד הגירה, אלא קמפיין נגד השחיתות ונגד החיבוק של אורבן לפוטין.

זה מה שבוער להונגרים.

2. להכיר את המערכת מבפנים: מאדיאר הגיע מתוך ה"כוורת" של אורבן. הוא הכיר כל נקודה רגישה, כל קבר פוליטי וכל חולשה.

השמאל ההונגרי עשה בשכל כשזיהה את המומנטום ופינה לו את המגרש. לפעמים בשביל לנצח, צריך לדעת לזוז הצידה.

3. מבחן המנהיגות: השאלה הגדולה עכשיו היא האם הוא יצליח לנווט בין הציפיות של כולם מבלי לשבור את הקווים האידיאולוגיים של העם שלו. המעבר מאופוזיציה לניהול מדינה שמרנית הוא שדה מוקשים.

4. הנקודה הישראלית (והכואבת): עם כל הביקורת על אורבן, ישראל איבדה היום חבר אמת שעמד לצדנו בשעות הכי קשות.

5. מילה לשמאל הישראלי: חגיגות השמפניה כאן בארץ הן לא יותר מ"אמביציה טיפשה". לשמוח רק כי נתניהו איבד בן ברית פוליטי, בזמן שישראל מאבדת תמיכה אסטרטגית באירופה?

זה לא חזון פוליטי, זו פשוט הכנסת אצבע בעין על חשבון האינטרס הלאומי שלנו

עברית

@KampnerSam לא איזה אקדמאי, אני חושב שיש תחומים שבהם מחקר אקדמי יכול להוביל לפריצת דרך בשוק/עולם האמיתי.

מה שאני חושב שיקרה אגב זה כמו שגוגל מציעים שירותים בחינם (משל ייצור הלחם) אבל את הכסף עושים מהפרסומות על גבי הדאטה שאוספים מהמוצרים החינמיים האלה. מניח שיקרה משהו דומה בעולמות הפיזיים

עברית

איך תראה הכלכלה בעידן הבינה המלאכותית?

לאחרונה נייר המחקר הזה מכה גלים בפיד.

הוא סנסציוני, הוא מנבא שחורות, והוא בדיוק מה שקורה כשאקדמאים מנסים לנתח את העתיד דרך המשקפיים הלא נכונות.

העקרון המרכזי במחקר הוא שאנחנו תקועים ב"מלכודת" אוטומציה.

על פי המודל שלהם, כל חברה פועלת בצורה רציונלית כשהיא מחליפה עובדים בבינה מלאכותית כדי לחתוך עלויות (לחובבי תורת המשחקים: אוטומציה היא האסטרטגיה המנצחת בלי קשר לפעולותיהם של שאר השחקנים).

ברמת המיקרו, החברה נהנית מ100% מהחיסכון בעלויות כתוצאה מהאוטומציה, אבל סופגת רק שבריר מהנזק שהפיטורים האלה גורמים לביקוש בשוק.

ברמת המאקרו, אם הכל עובר לאוטומציה, איך אנשים יוכלו להרשות לעצמם לרכוש טובין?

המסקנה שהם הגיעו אליה (נחזור לזה) היא שהחברות עצמן מפסידות כקולקטיב כשהן מפטרות עובדים, כי העובדים הם גם הצרכנים.

למרות שזה (לדעת המחברים) נכון, לא משתלם לאף חברה להאט את קצב האוטומציה כי החברות המתחרות יקחו את כל הרווחים. אז בעצם כל החברות בשוק כלואות במעגל התחרות הזו שבסופו של דבר תקריס בסיס הצרכנים ואת השוק.

הם גם מסבירים למה פתרונות כמו הכנסה כללית בסיסית (UBI) לא יפתרו את הבעיה.

בעיני, המחקר הזה מראה די יפה כמה מחקר אקדמי לא שווה הרבה.

לדעת הנייר הזה שבור מבנית ומטעה מאוד, ומהווה אילוסטרציה טובה לחשיבה מרובעת ושימוש לא נכון במודלים כלכליים.

אתחיל מהסוף. הטעות הקריטית כאן היא ההתעלמות מאיך שאוטומציה מלאה מקצה לקצה תדחוף את עלות ייצור הטובין לאפס. למה זה משנה? כי כשעלות הייצור של כל דבר שואפת לאפס, גם יוקר המחיה הבסיסי שואף לאפס.

אסביר.

תחשבו על מפעל שמייצר לחם בעולם של בינה מלאכותית. הרובוטים ידעו לגדל את התבואה, לעבד אותה, ולאפות את הלחם.

מלבד הייצור היישיר של הלחם, הרובוטים גם יודעים לייצר רובוטים אחרים ולקצור אנרגיה.

יש לכם כאן מעגל סגור שלא תלוי באף אינפוט חיצוני כדי לפעול.

עכשיו, מה יקרה אם המפעל הזה יתחיל לחלק לחם בחינם? בכלכלה נורמלית (כלכלת חסר), אם אתה מחלק טובין בחינם לא תוכל להמשיך להתקיים.

בכלכלת בינה מלאכותית זה לא נכון. מכיוון שהרובוטים עצמם רק צורכים חשמל ותחזוקה (שגם אותה הם מספקים לעצמם), הם יוכלו להמשיך לחלק לחם בחינם לנצח בלי שהעסק יקרוס.

אותו הדבר נכון לגבי ייצור רכיבים אלקטרוניים, הנדסה, חומרי גלם וכו.

במילים אחרות, עולם בינה מלאכותית הוא עולם של שפע חינמי כמעט בלתי מוגבל, לא עולם של קריסה כלכלית.

כלכלנים כל כך רגלים להסתכל על עבודה כאינפוט של תוצר עד כדי כך שכשגם כשהם כותבים עבודת מחקר של שנים על כלכלת בינה הם לא הצליחו להפנים את הרעיון של בינה מלאכותית שיכולה להחזיק את עצמה לחלוטין.

בעבר, הייתם צריכים לספק שירותים או טובים בצורה ישירה או עקיפה (כלומר כסף) תמורת צריכת טובין. אם לא הייתם עושים את זה, לאף אחד לא היה תמריץ ליצור כלום. בעולם של בינה מלאכותית, שורת קוד להגדרת פונקציות הפרס היא כל מה שצריך.

יש סיבה שכל כיתת כלכלה מתחילה עם ההנחות הבסיסיות של הכלכלה. לא שווה לקרוא אותם לפני שכותבים עבודת מחקר? 🤷♂️ קצת מביך…

עברית

@yosefyisrael25 אני חושב שהקבלה טובה לזה, ביביסט זה להיות אחד מלובשי החולצות השחורות בסוף שנות ה2000 עבור טבי נמני במכבי תל אביב.

אנשים שישרפו את הקולקטיב בשביל דמות אחת נערצת מסיבות לא ברורות

עברית

שווה אולי להמשיג את האירוע ״ביביזם״ כי יש פה קצת בלבול. יש לא מעט אנשים שבוחרים ואף מתכוונים לבחור (לצערי) בנתניהו. הם לא בהכרח ביביסטים. הם עושים את מכלול השיקולים (השגוי) וסבורים שבעת הזאת נתניהו הוא האיש שייטיב איתם ויישם את האידיאולוגיה שבה הם מאמינים. ״ביביזם״ זה להיות מושקע רגשית בנתניהו האיש, ולא משנה אם הוא מיטיב או מרע לך. כמו לאהוד קבוצת כדורגל או ללכת עם איזה קמע. זה בהכרח טמטום מוחלט. אף אחד לא מנסה להשפיל אותך - אתה עושה את זה בעצמך.

עברית

@aleabitoreddit You are magic @aleabitoreddit

Question: what are your favorite stocks to swing trade? Whats your best indicator for that?

English

@aleabitoreddit Dude you are the best follow (and subscription) on X!

You got me hooked on your content, keep on goating🐐

English

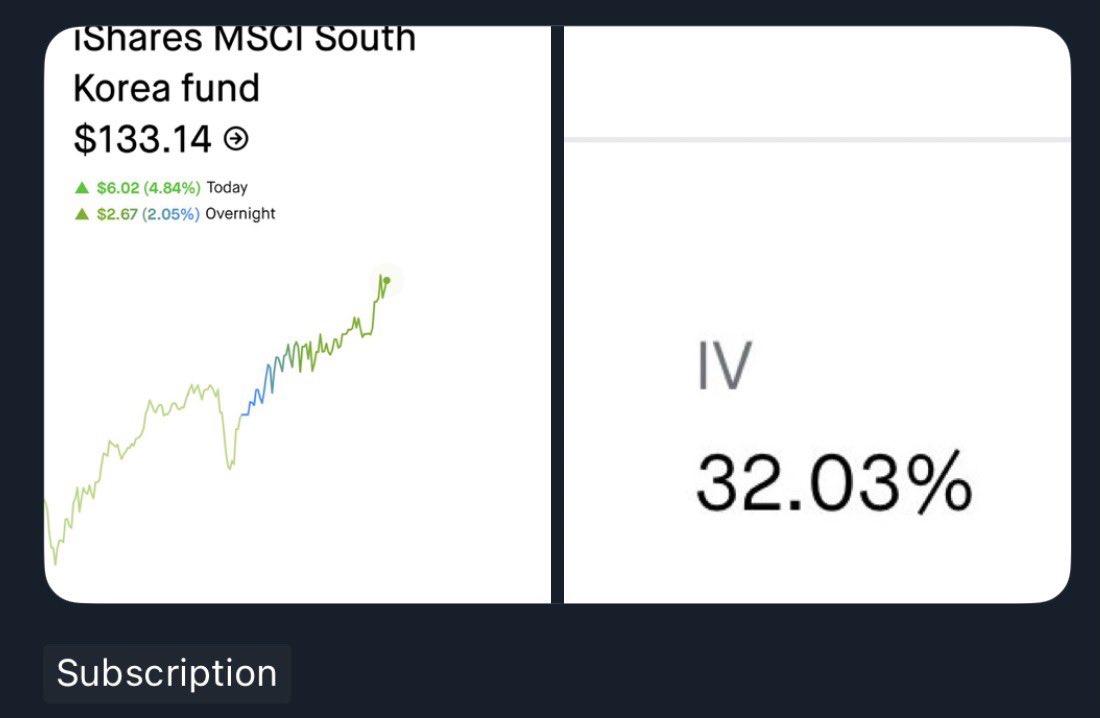

Holy… How goated was this $EWY IV trade?

The South Korean Index volatility went from 32% -> 51% since posting 3 weeks ago.

I’m not as impressed if $AAOI doubles but this call on South Korea’s volatility was legendary.

Serenity@aleabitoreddit

Trade idea that I published to my shower thoughts channel: Korean Index volatility arbitrage and taking advantage of Black-Scholes models. $EWY long options seem mispriced. This is Blackrock's Korea Index, which is majority memory (Samsung Electronics, Sk Hynix). The stock swings 2-5+% a day, and is up 136.25% 1Y, despite priced like a normal index IV. Samsung is volatile. SK Hynix is volatile (eg. 65% - 80% est). But the combination of the two through the index is priced way less than both low beta $GOOGL (37.33%) and $AMZN (39.12%) at ~32% IV. I've been watching $EWY for a bit and it does look volatile. As for pricing my guess is MMs priced in IV based on historical averages (5-10 years), where the Korean index was completely flat. And were expecting calls 2 years out to revert to the mean. But this volatility should be the new norm as markets price in the new memory supercycle (eg. $TSM went from 30% IV to 46.2% IV). Long calls should benefit from both Samsung + Sk Hynix carrying the index. And the main benefit is vega expansion that you won't get from $KORU. You also can't get this option MM pinning like individual US stocks since this is Korea's national index and long term. TLDR: Individual components SK Hynix + Samsung are highly volatile. They're basically half of the index, but options in index are priced with low volatility, perhaps due to historical 5-10 year data. Long calls benefit from vega expansion that weren't priced in correctly as MM forward vol estimates are anchored too heavily on historical realized vol, which was low for $EWY over the past 5-10 years

English

Maor Riven retweetledi

Folks. Can I explain something about world models? Seems like today might be a good day for that.

Advances in large-scale “world models” — whether developed by partners like Google or others — materially expand the frontier of interactive content creation. These models can generate high-quality, interactive, video-like experiences from natural language or minimal input.

Today, they are primarily editable through prompting, which limits the level of determinism and precision required for production-grade game mechanics. As a result, their outputs remain probabilistic and non-deterministic, making them unsuitable on their own for games that require consistent, repeatable player experiences.

Rather than viewing this as a risk, we see it as a powerful accelerator. Video-based generation is exactly the type of input our Agentic AI workflows are designed to leverage—translating rich visual output into initial game scenes that can then be refined with the deterministic systems Unity developers use today. Our agents already generate high-quality scenes from static video. Interactive, camera-controllable video from world models would further enhance this pipeline and materially improve the fidelity and speed of early-stage content creation. We believe this represents a meaningful step forward for AI-driven development across the industry.

Unity’s role is to operationalize these advances. Outputs from world models are ingested into Unity’s real-time engine, where they are converted into structured, deterministic, and fully controllable simulations. Within Unity, creators define physics, gameplay logic, networking, monetization, and live-operations systems to ensure consistent behavior across devices and sessions.

This combination enables developers to move faster from concept to scalable product: AI accelerates environment and asset generation, while Unity provides the execution layer that transforms generated content into reliable, monetizable experiences.

As a result, world models expand content supply and reduce development friction, while Unity remains the system of record for runtime, distribution, and long-term operations. This dynamic broadens Unity’s addressable market and reinforces its central role in the interactive ecosystem.

English

@yossizoo מי שהיה במשחק (וראה את עלי עותמן מקבל טלוויזיה מתנה בסוף) לא ראה מכירה כזו בהיסטורית הכדורגל

עברית

שלח לכל הצהובים שמצייצים על "כולם שונאים אותנו ומחמיא לנו שככה חווגים ניצחון עלינו"

עברית

ישששששששששששששששש

חשבו שהם יבואו לטייל רק בגלל שמאיר מליקה עצר שם פנדל של אבי כנפו בגביע. אחלה גיא מלמד, אחלה קנג׳י, אחלה אגבה, אחלה מגנים ואחלה ירמקוב.

ברק 💚

עברית

@LFC Need to remember that Liverpool played against Villa in the league cup at the same time

Same day 2 games in 2 different continents

English

I can spot Zinedine Zidane, who’s the other player? 🔥

Level: Hard

English

@MeidanK הם מקבלים הרבה כסף כדי לא לשחק בקבוצות אחרות.

זה מודל מכבי תל אביב בכדורסל

עברית

@thewhitepele @NirTsadok מסכים אבל עובדתית קרה משהו שלא קרה כנראה אף פעם (מתי מכבי תל אביב קיבלה 6 שערים בבית?) או לפחות לא קרה 30 שנה

עברית

@MaorRiven @NirTsadok זאת רק תוצאת כדורגל ואנחנו עוד לא יודעים אם תיהיה לזה השפעה בהחלםת מאמן, שחקנים, תוצאות רעות.

Israel 🇮🇱 עברית

למכבי ייקח זמן להבין לעומק מה עבר עליה אתמול במחצית השנייה. אלו מסוג הדברים שפשוט לא קורים לה. היא יכולה להפסיד, היא יכולה להיראות לא רע, אבל בכל שנות מיץ' גולדהאר, המעלה הגדולה ביותר שלה הייתה היכולת לקבוע לעצמה רצפה גבוהה, מין סטנדרט של איכות שדבר מתחתיו אינו אפשרי >>>

עברית

@thewhitepele @NirTsadok העובדה שזה ההפסד הכי גדול של מכבי תל אביב בליגה, מאז ה10-0 למכבי חיפה אומר שזה טרנס גולדהארי כמו שצדוק אומר, זה חצה את המחוזות של שנות הניהול שלו.

עברית

@NirTsadok לא מסכים עם ההגדרה ארוע טרנס גולדהארי. בדיוק כמו שתבוסות מהדהדות ומקריות של ריאל ויונייטד הן לא. ארוע טרנס גולדהארי הוא פרשת מיכה ואצילי פיטורי נמני הבאת זהבי. ההפסד ליוונים לפני שנתיים וחצי היה מעליב יותר ואנחנו לא מתעסקים בו בכלל. זאת תוצאת כדורגל, פריקית, אבל תוצאת כדורגל.

Israel 🇮🇱 עברית

@MeidanK בטח שלא שווים אבא שלו היה על הpayroll של המועדון במשך שנים.

גם הוא בכיס של יענקלה

עברית