Marc Rubinstein

3.4K posts

Marc Rubinstein

@MarcRuby

Former hedge fund manager; writes top 10 finance Substack https://t.co/UiByE4lqSg and contributor to Bloomberg @opinion.

London, England Katılım Eylül 2011

536 Takip Edilen26.3K Takipçiler

I just read a fantastic post by @MarcRuby called, "The Future of IR."

I am not going to spoil it, but I would highly suggest not only reading it and absorbing the information, but commit to going deeper...

I couldn't help but read it through the lens of what I see as the death spiral decline and 'state of affairs of shareholder activism' that has become essentially the following recipe:

Financial engineering + improve your communication/messaging (go dispose of xyz asset, and use proceeds to repurchase shares, and hold an investor sesh...[Do you see it])

vs actually helping corporations/c-suites/boards get better.

Get your mind right

English

I always tell visitors that Hobbs House Sherston is the best white bread they'll ever try. Now I've been vindicated: British Baker picked it as the best white loaf in Britain. It actually is the best!

English

Marc Rubinstein retweetledi

May I gently suggest, @GreenJennyJones, without doubting your good intentions, that this sort of response is part of the problem.

If you meet a specific wrong with a general virtue, you have not answered the wrong; you have stepped around it.

Jenny Jones@GreenJennyJones

@treesey I abhor cruelty and vindictiveness and hatred. Never mind who from, or who directed against.

English

Folks in London. You probably don't have anything to do right now. So get out your Oyster card and buy tickets right now to some see Odd Lots on May 7. Come hang out with me and Tracy and also meet a bunch of fellow listeners.

Joe Weisenthal@TheStalwart

HELLO LONDON FRIENDS: @tracyalloway and I are coming to town for our first live show outside the US. It's on May 7, and we'll be announcing some great guests in the days ahead, but tickets are already selling so you should get yours right this moment. events.bloombergevents.com/event/Odd_Lots…

English

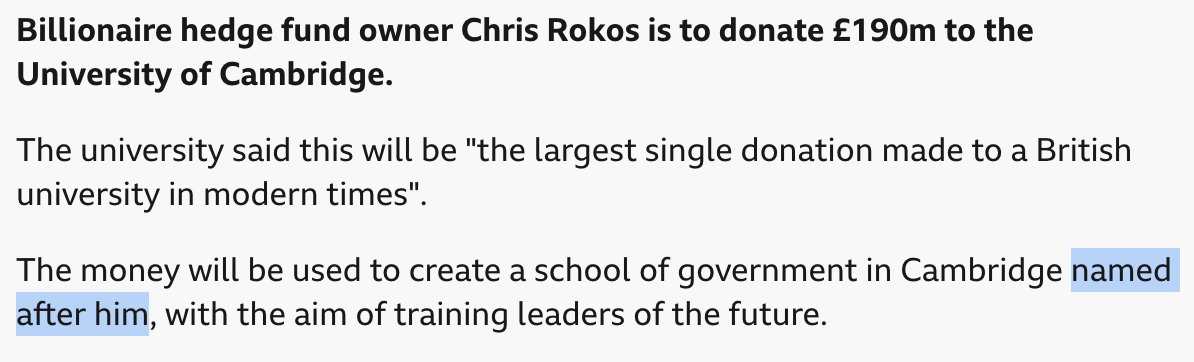

This is a good thing and Rokos sounds like a decent citizen (one of the highest taxpayers in UK) but I'm curious - why name it after yourself? To me that would feel grandiose & I'd want to signal my immense humility precisely by not doing that.

English

Good to see ideological diversity being valued (possibly more at this new school of govt than at Cambridge itself)

English

Marc Rubinstein retweetledi

Revolut’s pivot: Will going full bank kill its tech-level growth and valuation?

I read almost everything I can find about Revolut, but then I saw that Net Interest’s newsletter had dropped a new piece titled Revolut Unbound. I dropped my entire reading queue and started with it.

Net Interest is one of the top finance Substack newsletters, written by @MarcRuby, a former hedge fund manager, seasoned bank analyst, and Bloomberg Opinion contributor.

Marc and I have been following Revolut since almost the beginning, and we both have made small investments in the company. His Revolut Unbound piece is well written; it is best to read the whole thing yourself.

My top takes:

Marc suggests that low per-customer deposit amounts at Revolut could also be due to many customers joining rapidly and initially keeping low balances, which pulls down the overall average.

Another point Marc is making: can Revolut sustain its exceptional growth and high valuation as it fully transitions from a balance-sheet-light fintech company into a real, licensed global bank — or will the constraints of banking limit or alter its upside?

He writes: “One obstacle the group does face as it transitions more fully into a bank is capital. … One big difference though is valuation. … If Revolut can sustain both [rapid growth and 36% ROE], then Storonsky could be very rich.”

That is a great point. Initially, Revolut tried to be balance sheet-light, as I recall, CEO Nik Storonsky said in an interview that this way the company could grow faster and command a higher valuation as a tech company rather than as a bank.

Later, Nik admitted that avoiding heavier regulation was a mistake, and they are now embracing banking licences and biger balance sheets. One day, I will write my opinion piece on why I think it was a mistake.

The core idea of Marc piece: Revolut has come a long way from its early days of wanting to "replace banks" with a light, non-bank model — and securing full banking licences is a unlock that gives it new capabilities (deposits, higher net interest spreads, broader lending), but it also introduces real frictions and trade-offs that didn't exist in its more asset-light fintech phase.

Link to Net Interest newsletter: netinterest.co/?r=26ljc&utm_c…

English

@JaneCazneau If you follow me back I can DM. Thanks (and super work by the way).

English

@MarcRuby Yeah I'm not gonna drop it publicly but DM away if you're curious.

Hint: there are about 3 major (call it $10bn+ in credits back leverage risk on) banks in the world with the solve for it in their docs. Two its clean. One it's messy but I think they get there in the end.

English

Private credit funds will be very reluctant to roll over software loans when they mature. The closed-end funds can't refi any loans right now given redemptions. Since many loans were taken to pay dividends to sponsors, how will they repay maturing loans?

Will sponsors put new $ into the companies? many are past investment period.

Bring in new equity? that will be tough and pricey.

Refi with a mezz lender? will be at much higher rate.

Walk away? Huge loss and hit to reported marks.

In every situation, the equity is worth less even if business performance hasn't changed.

English

@MarcRuby Claude is pretty good at redlining docs from Edgar ;)

DM me if you want a specific link I guess. It's all out there

English

@JaneCazneau Hi Jane -- what's the source for the back leverage filings you posted?

English

@chuck_curious @DruckandTuck @johnarnold Old Jane: my orbital weapons burner

New Jane: my structured private credit burner I guess

AMA new followers. The water is warm

English

@John_Stepek I think 2008 is overused as an analogy, but NDFI loans are the vector to watch. Massive growth over past 10 years, leaving banks with over $1tr loans to non-bank financial institutions.

English

Private credit is clearly under some stress. What I'm thus far struggling to see (only at the early stages of digging in, though) is how this morphs into anything systemic/2008-ish. Theories welcome

Bloomberg@business

JPMorgan told private credit lenders that it marked down the value of some loans, clamping down on its lending as worries mount over credit quality bloomberg.com/news/articles/…

English

That’s four stock prices he’ll be managing. Almost as many as he has in the portfolio.

Bill Ackman@BillAckman

Today, Pershing Square Inc. (PSI), an alternative asset management company, filed to go public along with Pershing Square USA, Ltd. (PSUS) a new closed ended investment company managed by Pershing Square. In the combined offering, investors in the IPO of PSUS will receive shares in PSI for no additional consideration. For example, if an investor buys 100 shares of PSUS in the IPO, they will receive 20 shares of PSI at no additional cost. I explain the transaction in detail in a letter that can be found here: sec.gov/Archives/edgar… [sec.gov] The prospectus for PSI can be found here: sec.gov/Archives/edgar… [sec.gov] And the prospectus for PSUS can be found here: sec.gov/Archives/edgar… [sec.gov] The PSI and PSUS Registration Statements have not yet become effective. The securities described therein may not be sold, nor may offers to buy be accepted, prior to the time the Registration Statements become effective. Before you invest in the combined offering, you should read the Registration Statements for more complete information about the PSI, PSUS, and the combined offering.

English

Marc Rubinstein retweetledi

Here’s @marcruby’s debut Alphaville post, on the obvious arbitrage between disclosure-free “research” on social media and the massive burdens faced by traditional analysts. Hope it’s the first of many Rubyposts! ft.com/content/04b57c…

English

The broker note moved markets. Now the Substack does.

Same impact, fewer regs.

Joe Weisenthal@TheStalwart

The @Citrini7 selloff

English

As traders say: "The market is always right"

Joe Weisenthal@TheStalwart

Kind of incredible. Reading through the Blue Owl earnings call, how different what they're saying is vs. how the market is behaving.

English

@jeuasommenulle after the sale of $400m of loans at 99.8% of par value...

English

Wow- no one saw that one coming

Blue Owl permanently halts redemptions at private credit fund aimed at retail investors

English

Marc Rubinstein retweetledi

TOMORROW AT 11AM ET🚨🎙️

@MarcRuby and @michaelbatnick dig into the rapid rise of secondaries: why private assets are staying private for longer, how liquidity is being engineered rather than waited for, and what this shift means for valuations, incentives, and risk. They explore who wins, who loses, and whether secondaries are making private markets more efficient — or just more complex.👇🔥

Click me🎦youtube.com/live/N6P4tgIJh…

YouTube

English

@The_Analyst_Lab Did a trip out there last year. V interesting what's going on. netinterest.co/p/an-athenian-…

English

Anyone looking at Greek banks? They feel a bit like Spanish/Irish banks five years ago, maybe better?

You’ve got a pretty bank-friendly government and a strong fiscal backdrop (only EU country w/ surplus for next 2-3 years?), very lean cost bases (cost/income at low 30s), and a long runway for lending as EU funds are still barely deployed. Plus, gov is fairly supportive of cross-border m&a. Average deposits are only around €5k, which keeps betas low but also leaves a lot of room for catch-up in asset management and bancassurance. As loan-to-deposit ratios normalize, NII should grow with volumes, while fees can run double-digit for a few years. You’re not getting the easy 0.3–0.4x book rerating anymore, but with c.10% TNAV growth and 6–7% shareholder yield you can still make mid-teens returns without any rerating, main risk is just the macro/unemployment.

@blondesnmoney @dirtcheapbanks @jeuasommenulle

English