Marco Olevano, CFA retweetledi

Marco Olevano, CFA

15.6K posts

@MarcoOlevano

Derivatives Trader - CFA Charterholder - Passionate about financial markets - Views / Opinions expressed are solely my own.

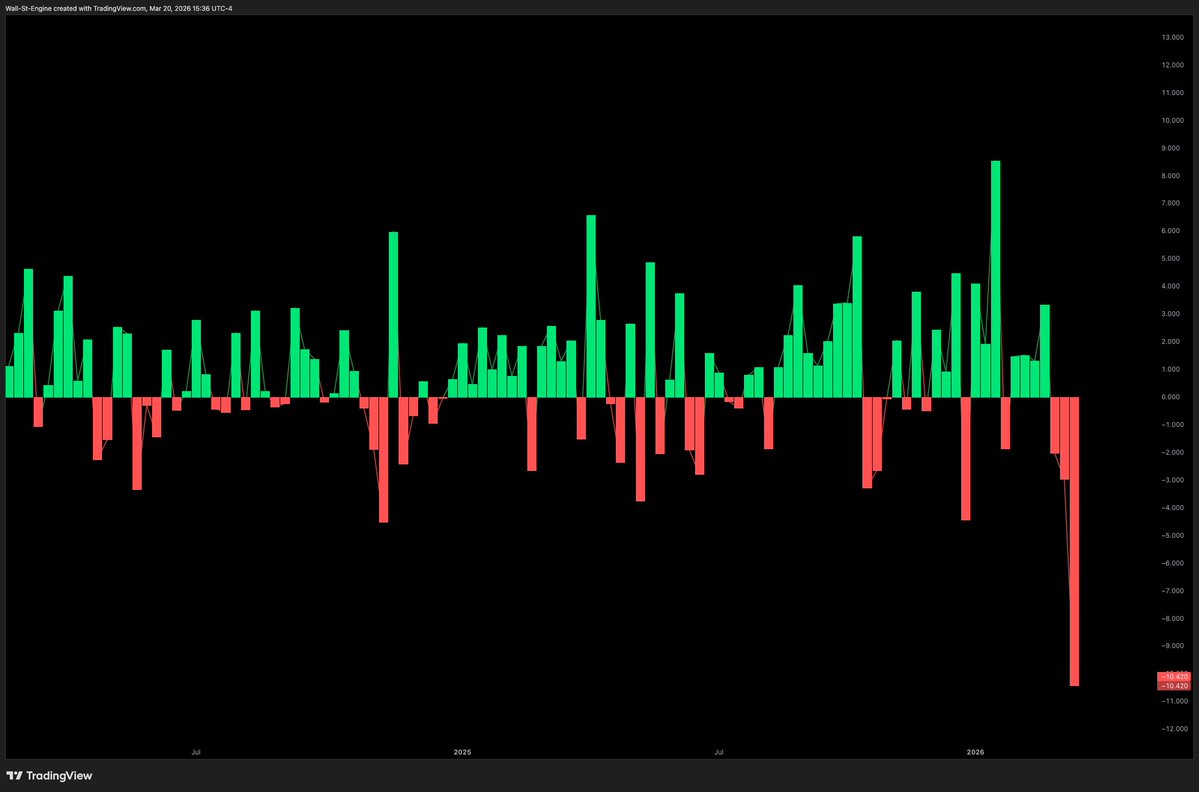

After #GOLD sharp drop, someone commented yeah... in hindsight... I always find skeptics of charts amusing. This is what I shared with our members in last week's update.

FREE Webinar: Defensive Portfolio – Protecting Your Capital Join experts @TraderPetri ,Lucie Moinvaziri & Marco Olevano for real insights into market conditions, volatility, and where to invest to stay ahead. 🗓 23 March 2026 ⏰ 2:00–3:00 PM (SAST) 🔗 us05web.zoom.us/j/86938870421?… 📩 Or RSVP: info@herenya.co.za 📌 Save this — don’t miss it. #Investing #Markets #Webinar