MiamiMarkets

82 posts

MiamiMarkets

@MiamiNYCDC

Takes on equity and credit markets. Not investment advice.

Miami, FL Katılım Kasım 2020

189 Takip Edilen70 Takipçiler

The $GME deck for $EBAY looks like what a college senior trying to pass Finance 301 with a solid C+ would put together

English

BREAKING: Ryan Cohen unfollows Michael Burry on X after he sells his entire GameStop $GME position

Financelot@FinanceLancelot

WATCH: Ryan Cohen attempt to explain how $GME is going to fund an $EBAY purchase. How does the math math? "I don't understand your question."

English

Large alt managers ($APO, $BX, $KKR) aren’t oversold - they’re de-rating to fair value. Asset aggregators post peak, in a crowded field, with fee compression on the come. You’re buying an annuity with deteriorating carry quality. Less juice, lower multiple. What am I missing?

English

$JELD headed for Ch. 11 or out-of-court solution - equity impaired. Sponsor destroyed business pre-IPO. Will have to give Europe away. 4 7/8s of '27 go current in 2 quarters, currently yielding ~30%. Even at a 15% refi coupon that's $40mm of incremental cash interest. Revenue guide up, EBITDA flat - cutting price to move volume. No incrementals. Common unshortable due to lack of cap / borrow / rate (R2K delete), but unsecureds fair value likely 40c ('27s and '32s pari, maturities collapse in BK). NIA

English

They bought the next frontier to ensure relevance and dominance. Really smart M&A / JVs over the years - YouTube, DeepMind, Instagram, WhatsApp, GitHub, LinkedIn, OpenAI, MGM. Most, and potentially all, ended up being bargains. Long all.

English

Monopolistic (excuse me, oligopolistic) MAG 4 ($META, $AMZN, $GOOGL, $MSFT) seem like no-brainers, even at these levels. Some of the best businesses ever created. Deeply moated, exponential growth, high margin, super cash generative - with inelastic pricing power into exploding AI demand.

English

They didn't just adapt to AI, they own it. $AMZN and $GOOGL hold large stakes in Anthropic - and Amazon doesn't just fund it, they power it, running Anthropic on AWS infra and their own Trainium / Inferentia chips. $MSFT is the largest shareholder in OpenAI. $META built their own - Llama is now one of the most widely used AI models on the planet.

English

@patientinvestor See my take, in case of interest - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

$META is looking a lot like $AMZN at sub-$190 2.5m ago. Market didn't like the FCF burn / believe spend would translate into topline fast enough and stock got crushed. It's already recovered. Same movie with $META today - except NTM FCF is still expected to be positive despite equally aggressive capex. Trades at 10.3x NTM EBITDA (per CIQ) vs. 13.4x, 19.3x, and 13.7x for $AMZN, $GOOGL, and $MSFT - despite NTM revenue growth of 22.7% vs. 14.0%, 19.7%, and 15.6%. Fastest grower, steepest discount, better FCF profile than $AMZN. And they don’t need a cloud business to monetize. Vertically integrated across the AI stack with 3B+ daily users as the distribution layer. The avenue is right there. Mag 7 oligopolies don't stay on sale forever. Hard to see a better risk-reward with this margin of safety in public markets today. Not investment advice - long all of these names.

English

$META at 18x earnings makes no sense!

30% revenue growth, reaching half the planet, and still priced like a no growth business.

English

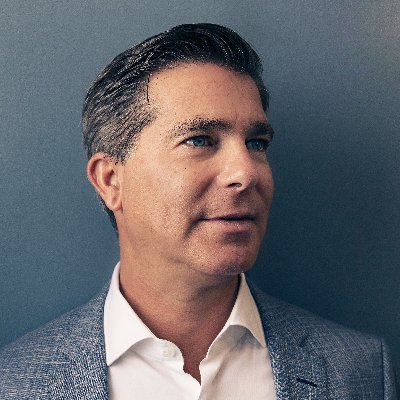

The market reaction of punishing $META because of the increase in CapEx will turn out to be very wrong IMO.

In the $META Q325 earnings call, Zuck already explained well that if $META overbuilds their compute infrastructure for internal needs, they can sell it to external parties.

We are in one of the biggest compute demand/supply imbalances that seems to be getting worse, not better. $GOOGL GCP CEO Kurian expects demand to be bigger than supply for 10 years.

$META's enormous AI compute capabilities will either return ROI in the form of their products (which they are already showing) or/and give great ROI by selling compute to external companies. $META investing in AI data center compute is a big asset, not a cash burn, similar to what metaverse investments were in large.

The market is viewing it as a negative, instead of an enormous strategic advantage in a compute-constrained world.

English

@KobeissiLetter You may find my post of interest - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

Have to respect Cohen's hustle, but $GME will be hard pressed to pull off an $EBAY acquisition. Here's why 🧵:

English

BREAKING: GameStop stock, $GME, erases all gains and falls -4% on the day after offering $56 billion to buy eBay.

English

@GerberKawasaki You may find my post of interest - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

Have to respect Cohen's hustle, but $GME will be hard pressed to pull off an $EBAY acquisition. Here's why 🧵:

English

eBay is actually doing a lot to improve their business. They have no reason to do a deal with a junk company run by this silly guy. $ebay $gme

English

@BoringBiz_ Well, yes, but board is incentivized to dismiss it out of hand and play hard ball. He missed window to nominate in time for June AGM, so time is on side of $EBAY for now and no way they will put company at a 20% premium when turnaround is just starting to work

English

@BoringBiz_ I think it’s more a question of why $EBAY’s board would want to sell. Hard to see this as being consistent with their fiduciary duty to of maximizing shareholder value. Turnaround is bearing fruit - they’d be leaving a bunch of money on the table.

English

Lot of people scratching their head on why a GME would want to purchase eBay, but think transaction makes more sense if you dig into some of the numbers

> Collectibles and trading cards now make up ~30% of GME sales. Ebay is growing their trading cards business at dougle-digits for 9+ consecutive quarters. Both businesses are individually making a big bet on the future of collectibles, which would become a combined effort moving forward

> Gamestop currently sells sealed trading cards across 1600+ stores with PSA grading at 1360+ locations. Most of the PSA products then end up on auctions and for sale on eBay

> Gamestop is currently holding $9 billion of cash and Bitcoin. That cash is currently not earning anything for the business, and needs to be put to work somewhere. The company itself has had poor ROIC on its own operations, so a great way to fix is through M&A

> Gamestop's recent Q revenue was -13.9% y/y. FY25 revenue was -5% y/y. Meanwhile eBay is growing in the mid-teens revenue growth range. Essentially solves your revenue decline problem

> Gamestop has accumulated federal NOLs from a decade of losses, which are currently not providing value to shareholders. Meanwhile, eBay was a net tax payer. The NOLs can ideally be used to offset some of the taxable income

English

@NotA_Bull Numbers seem to support this - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

$META is looking a lot like $AMZN at sub-$190 2.5m ago. Market didn't like the FCF burn / believe spend would translate into topline fast enough and stock got crushed. It's already recovered. Same movie with $META today - except NTM FCF is still expected to be positive despite equally aggressive capex. Trades at 10.3x NTM EBITDA (per CIQ) vs. 13.4x, 19.3x, and 13.7x for $AMZN, $GOOGL, and $MSFT - despite NTM revenue growth of 22.7% vs. 14.0%, 19.7%, and 15.6%. Fastest grower, steepest discount, better FCF profile than $AMZN. And they don’t need a cloud business to monetize. Vertically integrated across the AI stack with 3B+ daily users as the distribution layer. The avenue is right there. Mag 7 oligopolies don't stay on sale forever. Hard to see a better risk-reward with this margin of safety in public markets today. Not investment advice - long all of these names.

English

Absolutely wild that $META lost $160B in market cap after raising CapEx by just $10B even though the business posted some of its strongest growth metrics in years:

• Fastest revenue growth in ~5 years at 33% YoY

• Ad impressions grew 19% & Ad pricing grew 12% (rare combo)

• Reels time spent rose 10% from Instagram ranking improvements

• Q2 guidance came in stronger than expected at up to 28% growth

• Updated ad models drove a 6% boost in landing page view conversions

• Facebook video time rose more than 8% (largest sequential gain in 4 years)

• WhatsApp monetization is scaling with Family of Apps “Other” revenue up 74% YoY

English

@Mr_Derivatives You may find my post of interest - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

$META is looking a lot like $AMZN at sub-$190 2.5m ago. Market didn't like the FCF burn / believe spend would translate into topline fast enough and stock got crushed. It's already recovered. Same movie with $META today - except NTM FCF is still expected to be positive despite equally aggressive capex. Trades at 10.3x NTM EBITDA (per CIQ) vs. 13.4x, 19.3x, and 13.7x for $AMZN, $GOOGL, and $MSFT - despite NTM revenue growth of 22.7% vs. 14.0%, 19.7%, and 15.6%. Fastest grower, steepest discount, better FCF profile than $AMZN. And they don’t need a cloud business to monetize. Vertically integrated across the AI stack with 3B+ daily users as the distribution layer. The avenue is right there. Mag 7 oligopolies don't stay on sale forever. Hard to see a better risk-reward with this margin of safety in public markets today. Not investment advice - long all of these names.

English

Do we buy this $META dip?

Every time it dips it comes back with a tradable rip.

Rinse and repeat right?

English

@FinanceJack44 You may find my post of interest - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

$META is looking a lot like $AMZN at sub-$190 2.5m ago. Market didn't like the FCF burn / believe spend would translate into topline fast enough and stock got crushed. It's already recovered. Same movie with $META today - except NTM FCF is still expected to be positive despite equally aggressive capex. Trades at 10.3x NTM EBITDA (per CIQ) vs. 13.4x, 19.3x, and 13.7x for $AMZN, $GOOGL, and $MSFT - despite NTM revenue growth of 22.7% vs. 14.0%, 19.7%, and 15.6%. Fastest grower, steepest discount, better FCF profile than $AMZN. And they don’t need a cloud business to monetize. Vertically integrated across the AI stack with 3B+ daily users as the distribution layer. The avenue is right there. Mag 7 oligopolies don't stay on sale forever. Hard to see a better risk-reward with this margin of safety in public markets today. Not investment advice - long all of these names.

English

Most $META investors are getting caught up looking at EPS and FCF.

What I'm looking at is OCF, which has been exploding.

When CapEx is high OCF can be a great proxy for what future profitability could look like.

$META just grew OCF 34%…

This business is still an absolute beast even in an investment cycle.

English

@foxenflask Doesn’t solve the funding problem. Those aren’t penny warrants.

English

@tspencer322 That plan may not work - not sure the stock will trade up enough to make that feasible. He’s underwhelmed as head of $GME. ROIC not there. Agree he’s trying to bring his very OTM comp ITM, but don’t see a path via M&A. See my earlier take - x.com/miaminycdc/sta….

MiamiMarkets@MiamiNYCDC

Have to respect Cohen's hustle, but $GME will be hard pressed to pull off an $EBAY acquisition. Here's why 🧵:

English

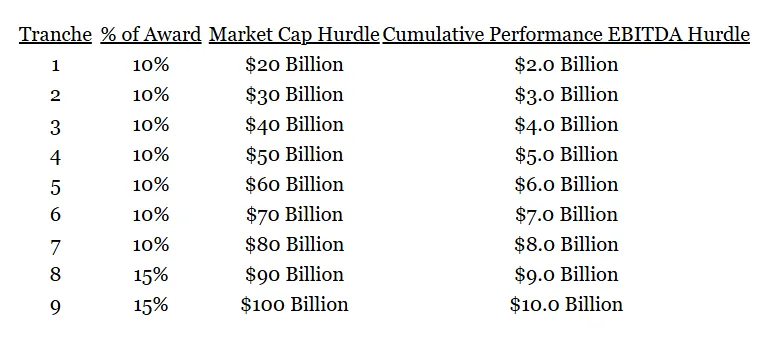

So basically, Cohen could be using the eBay acquisition news potentially to pump the stock price of $GME so he could then have the means to purchase another set of companies and build his own $EBAY.

Makes sense when you see what Dr. Burry posted earlier today showing a list of other potential acquisitions.

This would give Cohen the right to dilute GameStop investors once again putting GameStop over $10 billion in cash overnight.

Once he has an extra three to $5 billion sitting on the sideline to get easily snag up stock in 2 to 3 other companies, take control and merge them into GameStop pushing GameStop market cap close to $50bln.

Within 5 years $GME could see the $100bln needed for his pay package.

Getting eBay is a very ambitious move, but can also be used as a tool to make an absurd amount of money very quickly.

English

$GME isn’t buying eBay.

@ryancohen is doing what he always does.

The media is framing GameStop’s eBay bid as an acquisition.

It’s not.

Ryan Cohen is running a textbook activist investor playbook and the same one he used on GameStop itself.

Let me break it down. 🧵

English

@michaeljburry You may find my earlier take interesting - x.com/miaminycdc/sta…

MiamiMarkets@MiamiNYCDC

Have to respect Cohen's hustle, but $GME will be hard pressed to pull off an $EBAY acquisition. Here's why 🧵:

English

My thoughts on $GME play for $eBay, with an analytic comparison to my February hypothetical.

open.substack.com/pub/michaeljbu…

English