@steve_donze Looks to me like IT index fell off a cliff before forward estimates had revised downwards?

English

Kartikeya Mehta

14 posts

@MumbaiLad

Mumbai boy. Notre Dame, Wharton. I increasingly know nothing.

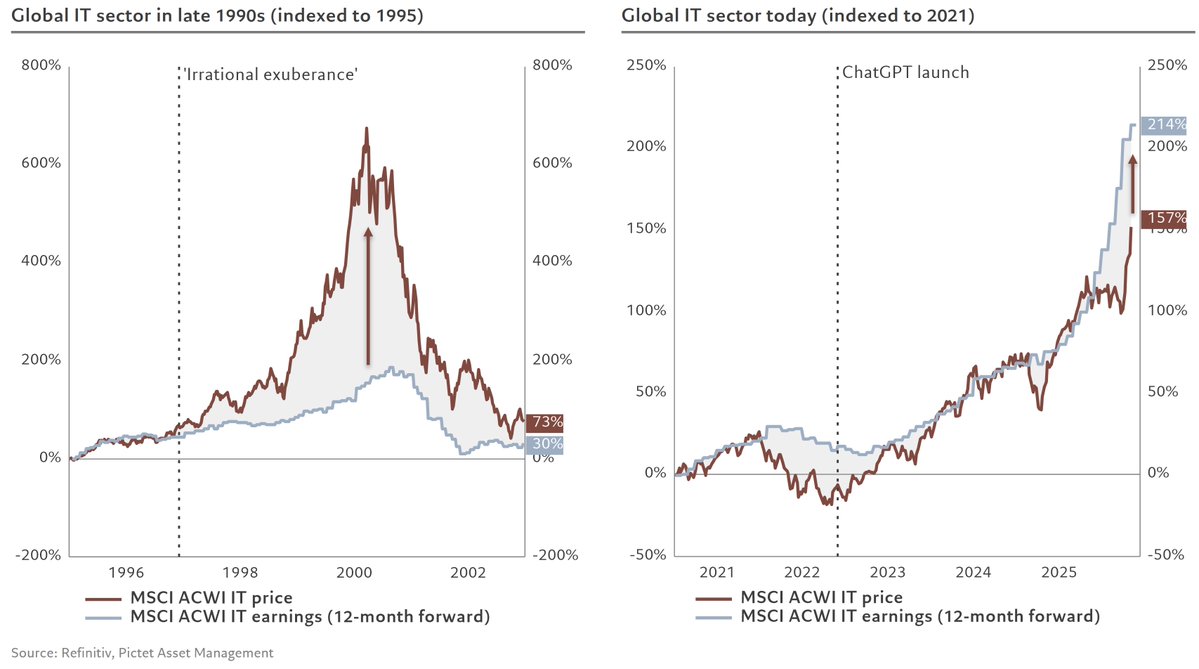

Earnings-led, unlike then.

On food: France has 600+ Michelin Star restaurants. The US has ~200, despite a population 5x larger. A €5 bottle of wine in Spain beats a $25 bottle in California. A €2 espresso in Rome beats a $7 oat milk latte in Brooklyn. This isn't snobbery. It's math per dollar.