Nandus

13 posts

Few things sum up recent events as succinctly as this...

I couldn't believe what I was seeing, so I called my friend Jhonny and said: "What the Fuck?!? La Gente esta muy Loca...."

youtu.be/542urpAYRVA?si…

YouTube

English

1. There are many companies like Nabtesco 6268 in Japan trading at similar multiples, so it doesn't stand out as being special. 2. I appreciate its high market share in industrial robots, with especial credit to its automatic doors and bullet train brakes; but I don't see further upside. 3. Its margins are consistently falling, while cash reserves are rising, potentially indicating some kind of capital mis-management. Ideally, one would want management teams that build operating leverage over time, coupled with buybacks if there aren't any major investments left to be made.

English

[Warning: stream of consciousness shit post] Japan market is gaining steam and unlikely to stop, the main driver being the shift in mindset of Japanese people, from saving to investing, partly aided by the new NISA tax-incentive program. One beneficiary of this trend are securities brokerages, long suffering from falling trading fees, but sitting on decades-long cash reserves. Kyokuto Securities (8706) has been bid up after hiking its DPR to 100% and seeing rapid growth in profits. Similar trends have been seen at 4267, 7343, 2148, and 7226 all announcing 100% DPR. Activism is still alive and kicking, with the likes of 7279 Hi-Lex hoarding cash and securities multiple times its mcap, TBS 9401, a TV broadcaster with shares in Tokyo Electron 8035 twice as much as its own mcap and also sitting on huge unrealized gains on land in Akasaka, and Tokyotokeiba 9672, which has a killer app SPAT4 (horseracing app aggregating all local and urban races), but keeps on losing money on an amusement park and investing in unrelated warehouses. There's also 7803 Bushiroad, which has a killer card game business but is persistently weighed down by a loss-making games business. SIers (short for System Integrators), i.e. the companies to which Japanese firms outsource software development, have been all the rage since last September when the economy felt like it was turning and people turned defensive. These SIers trade at low multiples but are consistently profitable and have very sticky contracts, making them (or cheap trading companies) the most defensive sectors in Japan, imv. However, we're starting to notice that the Japanese economy might be more resilient than once thought, esp. with the huge investments being made in semi plants. In the semi sector, I highlight Okamoto Machie 6125 as a dirt cheap firm with an edge in final polishers, discounted due to China exposure and RS tech 3445 another dirt cheap reclaimed wafer producer discounted by China risk. I also like Shinetsu Polymer 7970 and Mimasu 8155, i.e. the Shinetsu Chemical Group affiliates likely discounted due to parent-child listings. The TSE focused on capital cost disclosures last year, and is expected to ramp up pressure on parent-child listings for disclosure of measures to protect minority shareholders. This new TSE push still has room to be priced in by markets. I envision Japan eventually becoming a 'semi factory of the world' and if this were to play out, even richly valued companies like Fujimi Inc, Lasertec, Advantest should continue to be in favor over decades. Meanwhile, I also envision Japan Inc. to undergo further consolidation. The majority of SMBs are run by founders in their 60s/70s, many of which don't have successors. A lot of these companies are low-margin on their own, but can transform into higher-margin bizes when integrated in larger conglomerates because of economies of scale and pricing power. Waste Management is one sector I'm interested in, as the waste collection sector is extremely fragmented and unprofitable but becomes lucrative once tied to incineration and landfill. The overall increase in AUM in PE (driven by higher GPIF and megabank allocation to alternatives) should benefits the likes of 5842 Integral, 9552 M&A Research, 6196 Strike, and maybe 4310 Dream Incubator. Also, while 99% of market paricipants would probably disagree, I find it intriguing that every station I go to in Tokyo has a prep school nearby like Waseda Academy 4718, Meiko Network 4668, or Ena 9769. These are cash-hoarding businesses that are likely to enjoy survivor benefits in a shrinking market over the LT, and their earnings have proven to be way more resilient than priced in by the market. All of this probably sounds like gibberish to foreign investors, because they're can't invest in small caps anyways because of low liquidity. For such investors, Hikari Tsushin 9435 remains the foremost option as a way to gain exposure to a basket of 300 or more small caps handpicked by value investing experts cultivated within the company. A GARPy name I've tweeted about in the past is Software Service 3733, which continues to be my favorite exposure to Japan's hospital EMR market. It has the second largest share only after Fujitsu. There are only 8000 hospitals in Japan, and 4000 have already been penetrated. New entrants are unlikely to come in at this stage-what remains to be done is use the EMR data as a starting point and cross-sell other software using that data. Arent 5254 though richly valued has an interesting JV with Chiyoda called Plantstream, a SaaS for the construction industry rapidly gaining adoption globally (probably the only Japanese SaaS with rapid global expansion today). Regardless of sector, what I've come to appreciate are recurring business models, where sales increase predictably and margins rise as well because of operating leverage. An under-the-radar sector is warranty/guarantee services, like Japan Warranty Support 7386, Entrust 7191, and eGuarantee 8771. What's important is that this operating leverage can be captured with limited capital, meaning that leverage converts easily to FCF. The only thing I don't like about the semi industry is that R&D costs are likely to spike from here, and what appears as extremely high leverage today will soon be recognized as the 'peak' as many are going to ramp up investments in both increased capacity and R&D. On a separate note, I'm bullish on engineering worker dispatch companies, especially Meitec 9744, as 'reshoring' of factories is likely to be a huge theme in the coming decade. It's much cheaper now to produce in Japan, and there's gonna be a lot of network effects with major players like TSMC being in Japan. Last but not least, consulting is a sector I like because the unit economics are crystal clear (employee x per-employee profit) or (account x per-account profit), and I don't see the need for decision-makers (i.e. consultants) ever being replaced by AI. SHIFT 3697, BayCurrent 6532, Change 3962, and SIGMAXYZ 6088 are the companies I'm watching in this space. Though I doubt anyone has read this far into my post, if you have, and are interested, feel free to DM me to have a convo about any of the sectors or companies I mentioned. You can also email me here for company arrangement or interpretation services: info@jpinv.com

English

@memyselfandi006 What do they mean with "Investor"? $ITM NAV?

English

Nice Chart from the curren Italmobiliare Company presentation. The only way is up !!!

italmobiliare.it/sites/default/…

English

@MichaelR_Quant @memyselfandi006 @Sutjeinvestor @Govro12 Definitely worth to follow, they have an interesting Value Portfolio (good picks such as Kemira).

Another Value Fond owning Lassonde is Palm Valley Capital if im not mistaken, they mostly hold liquidity if they dont find value in markets (about 70-80 percent lately).

English

@memyselfandi006 @Sutjeinvestor @Govro12 Thanks for you insights. Is Tweedy Brown owning this rather a good sign or a red flag? I don't know him, but will Google and research him...

English

Yesterday I bought stocks of the boring Canadian company Lassonde $LAS.A . Margins have come down to 5.3% LTM. They could reach historic margins of 6-7% again. Plus, multiples are low historically.

youtu.be/ADNyHnegqGI?fe…

YouTube

English

Impressive 2024 Guidance release for Paul Hartmann AG. Further growth ahead in 2025, I am still convinced that it shouldn’t trade at the current Forward P/E of 7 and P/B of 0,65 - but I will probably die on that hill 🙂

EQS News | Ad-hoc@eqsnews_adhoc

PAUL HARTMANN AG (ISIN DE0007474041): HARTMANN erhöht seine Ergebnisprognose für 2024 eqs-news.com/news/adhoc/pau…

English

@shocklord @memyselfandi006 @goodinvestingc @vnvglobal @BlaBlaCar They provide the platform and charge a fee for every ride. Even if the Journey ist Like 15 Euros they get about 3 Euros. Its popular as its not just about the ride but sharing it.

English

#vc investing is challenging. Companies fail, rounds are harder, and profitability is critical.

In these challenging times, Per Brilioth of @vnvglobal gave us answers. We, for instance, discuss Voi, @BlaBlaCar, and Alva.

👉🏻👉🏻👉🏻 youtu.be/-bi7dif2Vi8

YouTube

English

@memyselfandi006 @Sutjeinvestor Has any of you ever had a look at Aalberts N.V. from the Netherlands ? Not that they are similar, but they make a big part of their revenue in housing (valves, pipes). Got to know about them because it was a small add recently from Tweedy, Browne.

English

@Sutjeinvestor The sector really looks interestig. No one knows what 2024 will bring, but the sentiment is very bad.

English

@travislundyasia @InvestInJapan @willschoebs @JamieHalse @TeddyOkuyama @Sutjeinvestor @StocksAndMacro @Fritz844 @Jake___Barfield @agoyal00 @JCVpartners @patrick_oshag @evfcfaddict What was your impression on Nabtesco? Tweedy, Browne own it in one of their funds.

English

@InvestInJapan @willschoebs @JamieHalse @TeddyOkuyama @Sutjeinvestor @StocksAndMacro @Fritz844 @Jake___Barfield @agoyal00 @JCVpartners @patrick_oshag @evfcfaddict I have looked at some of these. Nabtesco for years, espec in its conscious uncoupling from HDS (6324), Hakuhodo, Nuflare (now taken private), Lasertec, Tokyo Ohka Kogyo, Yokogawa Elec, Asahi Kasei, Asahi Intecc (always seems pricey to me), Osaka Titanium, Makita, Torishima Pump.

English

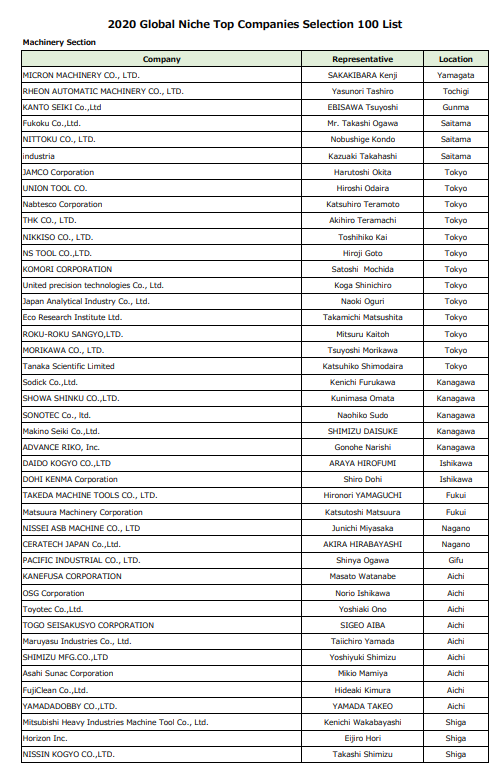

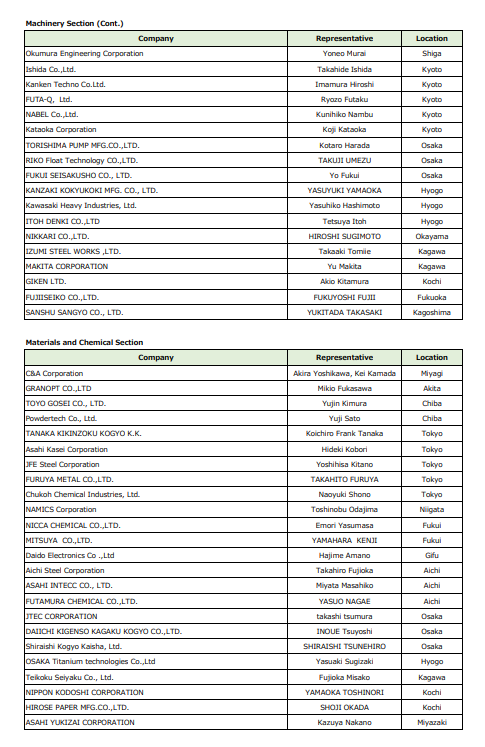

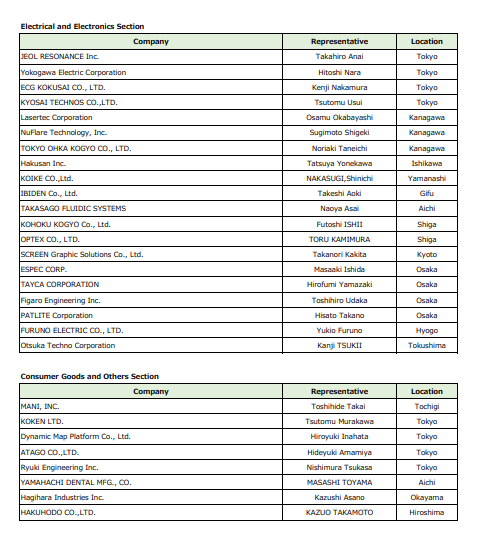

🗾Japan field guide🗾

METI periodically publishes 'Global Niche Top 100' companies from 🇯🇵

Whilst slightly old, the list has a trove of listed companies worth looking at 👇

Which one catches your eye? 👀

#madeinjapan #stocks #investing #multibaggers🇯🇵

English

@poyntout @stromab @Finanztalk0711 @UPMGlobal Danke ! Macht Sinn. Mir gefällt der Waldbesitz, der nach unten zumindest abfedern kann. Vor allem wenn die Unternehmen wie UPM nicht hoch verschuldet sind. Und wenn Lumber ein Vorläufer ist, dann preisen die Kurse vielleicht so langsam eine Rezession ein.

Deutsch

@godwinsoll @TheMarket_CH @gabr_hunter Ich denke, die Rubrik ist zur Vorstellung von Einschätzungen gedacht, und keine Empfehlung der Redaktion. Also müssten Sie sich an Berenberg richten.

Deutsch

@TheMarket_CH @gabr_hunter Sie hatten auch schon BASF als Call der Woche. Ich werde nun also mit Ihrer Vorschläge etwas vorsichtig...

Deutsch

Der Call der Woche, von @gabr_hunter: Interroll

themarket.ch/hinter-der-hea…

Deutsch