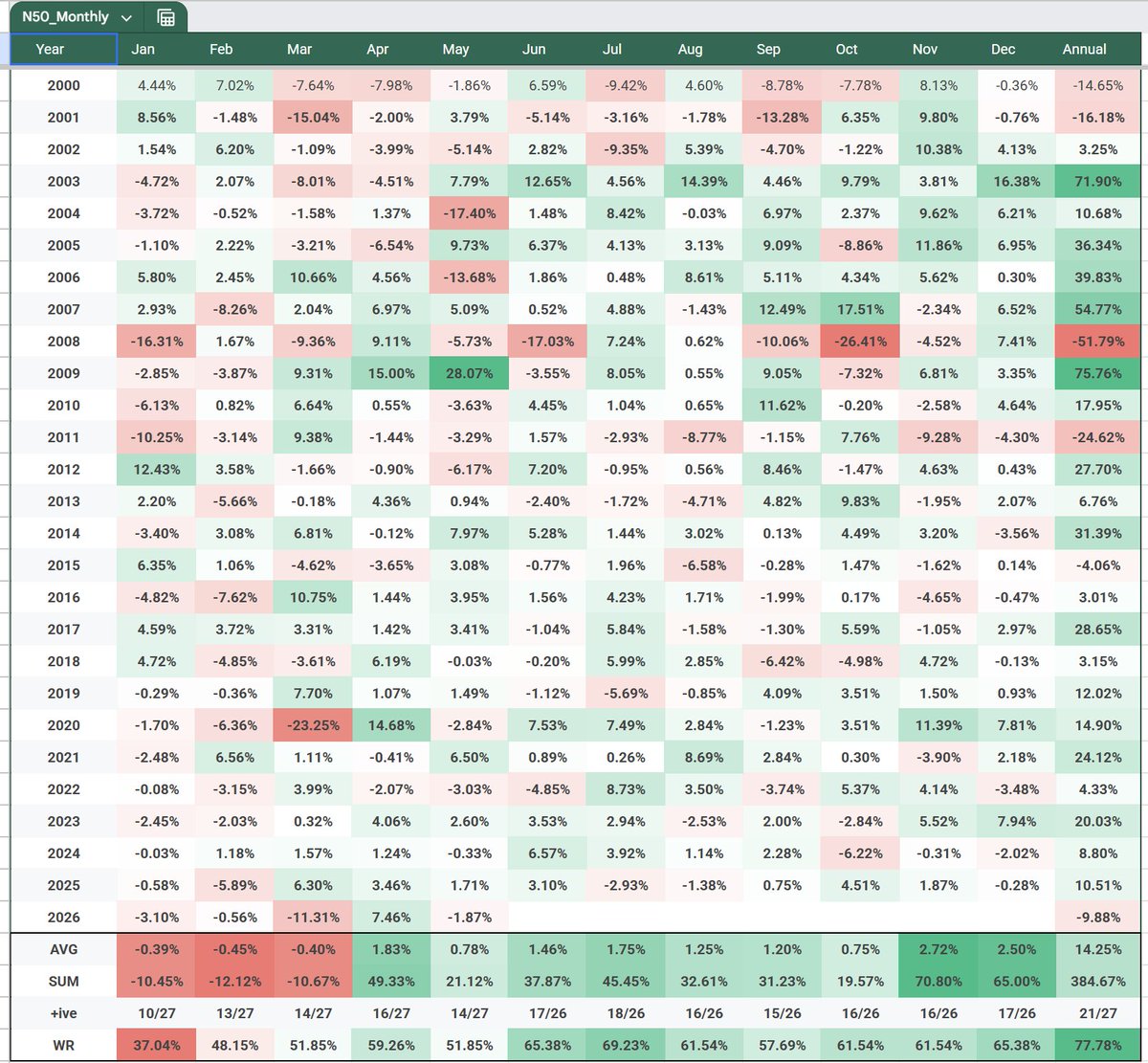

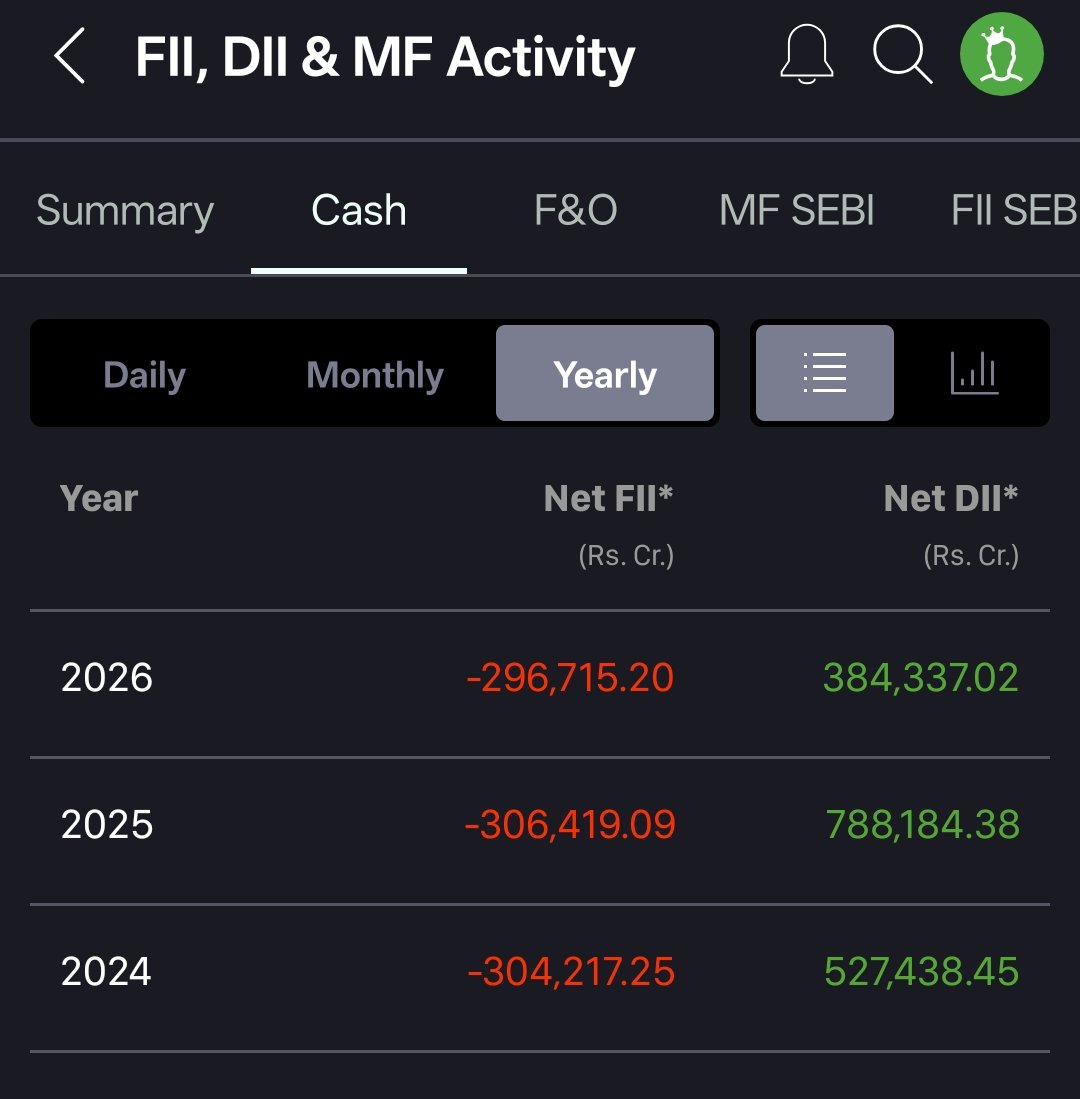

@KalpenParekh @SahilKapoor Yes, the same principle applies to India and other markets. Flat return periods follow major bull runs. That's why booking some profits after abnormal gains is important. And then asset allocation is key to preserving gains and generating alpha.

English