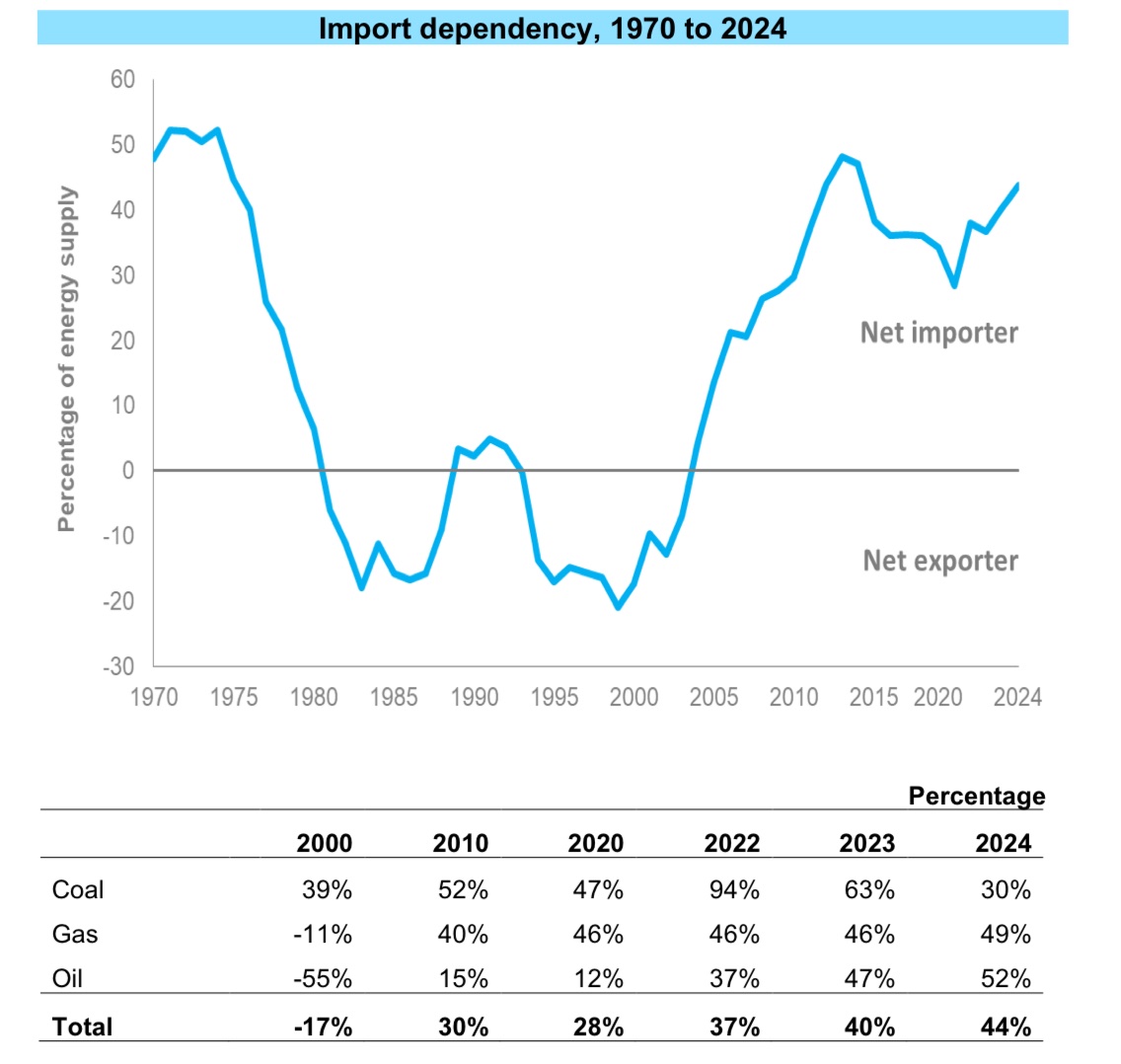

In light of the renewal of the debate around energy extraction, particularly Britain’s oil & gas industry, it seems appropriate to highlight several of the arguments by proponents of the Net Zero agenda against oil & gas, broken down by claim. 1) “Prices are set on international markets, so UK extraction doesn’t help” • While there are international benchmark prices, this is misleading • Commodity trading firms make vast sums of money trading the dislocation between regional prices, seen most clearly in 2022 • UK now imports ~50% of its gas • Domestic production: o reduces reliance on LNG spot markets, the most volatile segment o lowers exposure to geopolitical shocks • Energy imports cost the UK tens of billions per yearduring crises • Domestic supply improves balance of payments and currency stability 2) “Private companies mean profits don’t benefit the public” • North Sea producers face ~75% headline tax rate • Generated ~£9–10bn in tax revenue in 2022–23 (HM Treasury / OBR) • £350bn+ total tax receipts since the 1970s • Supports ~200,000 UK jobs (Offshore Energies UK) • Government retains control via: o licensing o taxation o regulatory approval 3) “We shouldn’t expand fossil fuels during a climate transition” • UK still relies heavily on gas: o ~80% of homes heated by gas • Cutting domestic supply does not get rid of the demand • Imports replace production: o LNG often has higher lifecycle emissions than domestic gas • Gas remains essential for: o power system backup o heating o fertiliser and industrial processes 4) “New extraction won’t lower consumer bills” • It’s true that it does not directly set prices, but: o reduces price spikes and volatility o lowers reliance on high-cost LNG spot purchases o reduces system risk premiums • 2022 crisis driven by regional supply constraints, not absence of global supply 5) “Renewables and nuclear will replace gas by the time new fields come online” • Most projections show gas still in the mix into the 2030s+ (CCC / IEA) • Nuclear build timelines: 10–15+ years (we want these shortened, but we work with what we have) • Renewables require: o backup generation (currently gas) o major grid/storage expansion • Gas still needed for non-power uses (e.g. fertiliser) • Other countries will likely still need to buy oil & gas. We should be able to supply it to them. 6) “We’re running out of reserves anyway” This is entirely false. • UK Continental Shelf estimated to hold ~5–15 billion barrels of oil equivalent remaining(NSTA) , with 2.9 billion barrels of oil equivalent proven & probable reserves. • Falling production reflects: o policy o investment o licensing constraints Rather than any lack of resources 7) “Why more gas storage?” • UK storage capacity: o ~2% of annual demand o vs 15–25% in many European countries • Low storage → higher exposure to: o price spikes o supply shocks • Reduced flexibility since closure of Rough storage facility Gas storage serves to smooth out price volatility and contributes to security of supply. Ultimately, it comes down to this: the Norwegians, Saudis, and Russians do not mind so much when oil & gas prices go up. They are selling the oil and gas. We could be too – and the profits would flow to British companies, British shareholders, British workers, and the British state. Why not have that instead of paying to import it our energy? We cannot let the myths overtake the narrative: let’s get rich.