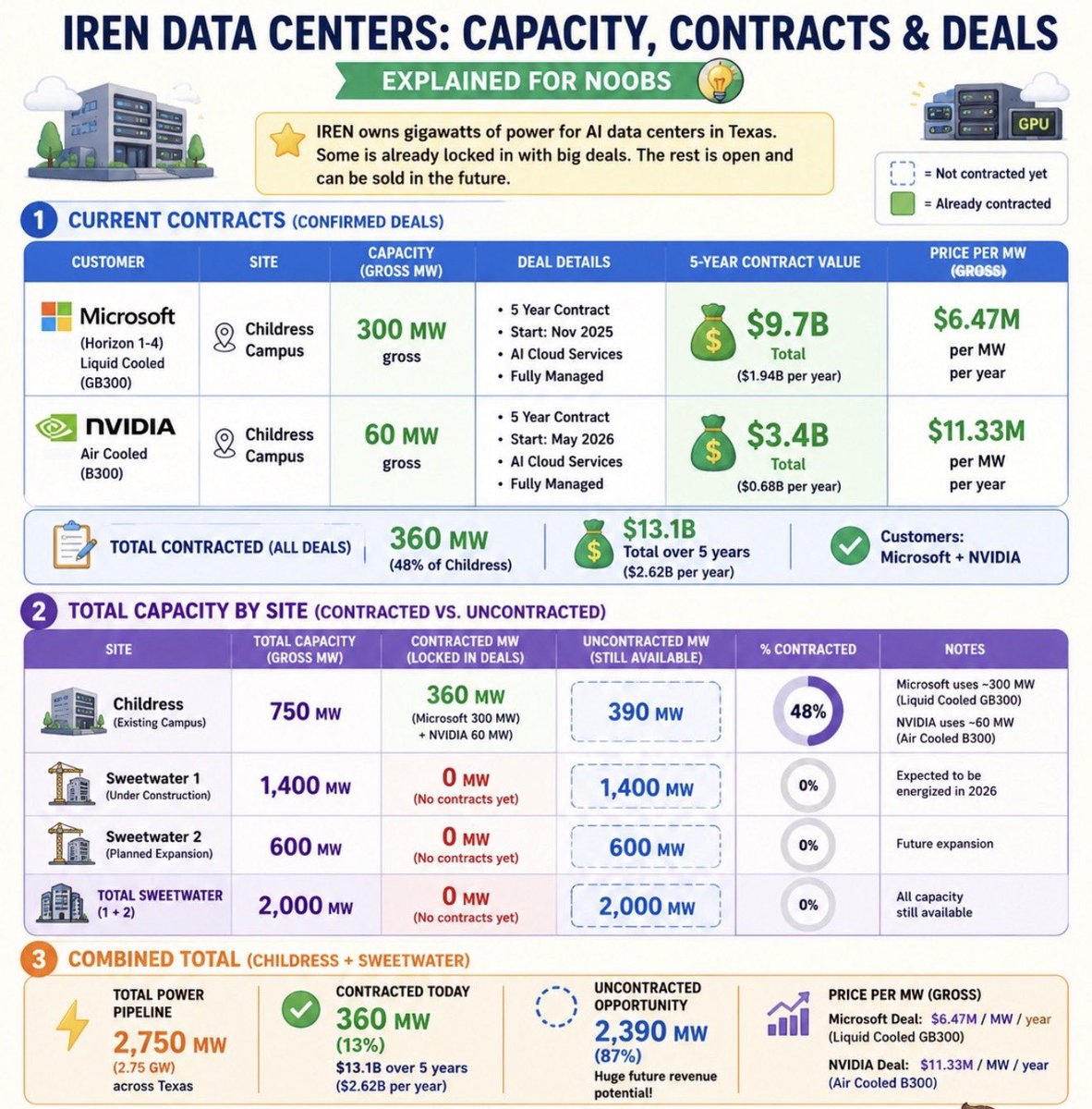

@mikealfred Why won't (can't?) IREN presell any power? Is there an issue here?

English

BankSpecialist

832 posts

@OneLuckyLobster

Stop following me, I am a bot

New account, so here’s the short version. I started at JPM. Built a company. Sold it for $100M+. Served in places where risk was not theoretical. Now I spend my time looking for public companies sitting at the intersection of capital, technology, and strategic necessity. Defense tech. AI infrastructure. Space. Bitcoin. Critical infrastructure. I am not here to post 50 tickers and celebrate the ones that work. I am here to find the few names where the market is using the wrong frame. Old category. New asset. Messy transition. Right team. Massive demand pull. That is where the asymmetry usually lives.

Back-of-envelope numbers for 1 gigawatt data center: All-in Capex: ~$50 bn Enterprise revenue generated: ~$25-30 bn/year Electricity cost: $1-2 bn/year ~2 year payback. The boom is real.

Feels like we’re still early in the compute cycle. Supply isn’t easy, real-world constraints are everywhere. And every step forward in AI just seems to create more demand for compute.

A 5-year backlog on grid transformers just killed half of America's 2026 AI data centers. Sightline Climate tracked 12 GW of 2026 US data center capacity announced across 140 projects. Only 5 GW is actually under construction. 11 GW sits in the "announced" stage with no physical progress despite typical build times of 12-18 months. 25% of those projects haven't disclosed a power strategy at all. That last number is the tell. A quarter of "planned 2026 AI capacity" has no sourced answer to where the electrons come from. Call those projects what they are: vapor capex with a press release attached. Nvidia is shipping. The gating constraint is high-voltage transformers, switchgear, and grid-tie batteries. Pre-2020 lead time on a high-power transformer was 24-30 months. Today it stretches to 5 years. Electrical equipment is under 10% of total data center cost and 100% of the bottleneck. This breaks the standard analyst model. When a hyperscaler announces $50B of capex, the Street treats it as compute coming online in 18 months. If the transformer order wasn't placed in 2022, that money sits as commitment without capacity. You cannot pay for a transformer that doesn't exist yet. The winners under this regime are whoever locked in power purchase agreements and electrical equipment orders 3-4 years ago, before anyone was modeling hundreds of megawatts of inference load. Everyone else is waiting in line behind them. Second order is uglier. Hyperscalers buying $50B of GPUs that sit unpowered depreciate against Nvidia's annual cadence while paying carrying costs on empty data center shells. Every quarter dark is a quarter of compounding waste. The "we're 6 months from running out of compute" panic just became "we're 5 years from running out of transformers." Capital fixes one. Capital cannot manufacture a transformer.

$IREN Just added 7 new positions for Prince George in the past 24 hours. Interesting 🧐

These names are setting up for major upside moves: $IREN Iris Energy $CRWV CoreWeave $CIFR Cipher Mining $HOOD Robinhood $SOFI SoFi Technologies $ONDS Ondas Holdings $UUUU Energy Fuels $ASTS AST SpaceMobile $SNOW Snowflake $SE Sea Limited $CELH Celsius Holdings $LAC Lithium Americas $CIFR chart shared below. The rest are already mapped out inside the community.