Sabitlenmiş Tweet

𝗟𝗲𝘁 𝗺𝗲 𝗿𝗲𝗽𝗲𝗮𝘁 𝘁𝗵𝗶𝘀 𝗽𝗼𝗶𝗻𝘁: 𝗧𝗵𝗲 𝗯𝗲𝘀𝘁 𝗯𝘂𝘆 𝘀𝗶𝗴𝗻𝗮𝗹 𝗶𝗻 𝗺𝗮𝗿𝗸𝗲𝘁𝘀 𝗶𝘀𝗻'𝘁 𝗼𝗻 𝘁𝗵𝗲 𝗽𝗿𝗶𝗰𝗲 𝗰𝗵𝗮𝗿𝘁.

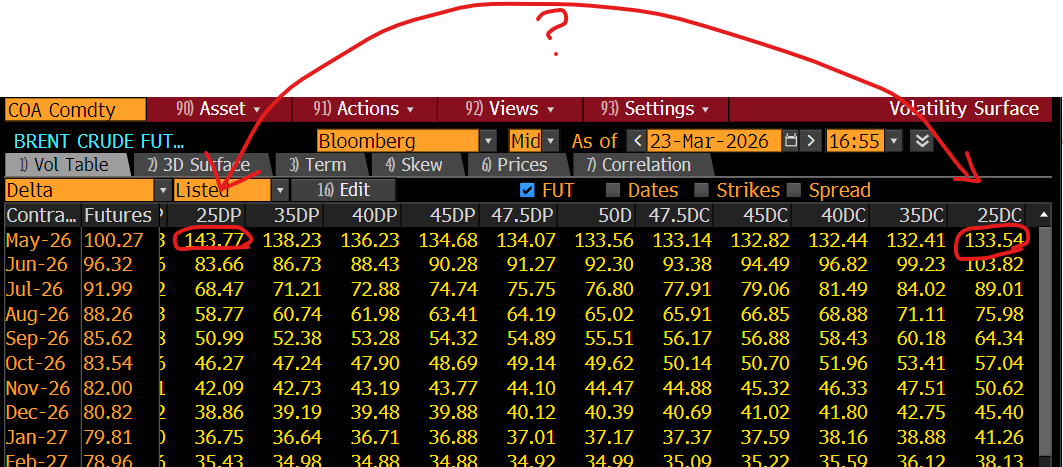

When spot makes a new low and VIX refuses to make a new high, pay attention. That's a vol divergence. The options market is quietly telling you it doesn't believe the selloff has legs.

But most traders miss it because they're staring at candlesticks.

Here's how to read it properly. Pull up fixed strike vol on the front of the curve. If the market is selling off hard and fixed strike vol is flat or drifting lower, that's your tell. The people who price risk for a living are saying "we're not buying fresh protection here."

Think about what that means. If vol can't rally when the market is getting destroyed, what happens when spot bounces even 1%?

Vol gets annihilated.

So the real trade here is selling the vol that can't go up. Different expression, completely different risk profile, and way better risk-reward than just buying the dip. When you learn to trade in more than just the spot dimension, you find edge in other areas like VEGA.

English