Sabitlenmiş Tweet

SkiedOut

435 posts

SkiedOut

@OutSkied

Toronto based buy-sider who loves a pow day.

Katılım Mart 2021

660 Takip Edilen94 Takipçiler

SkiedOut retweetledi

Great engagement farming but except for the facts getting in the way...

Requiring board or company approval for stock transfers, along with mechanisms like Rights of First Refusal (ROFR), is extremely common in private startups and closely held companies. This helps them control their cap table, prevent unwanted shareholders (e.g., competitors, activists, or speculators), manage valuations, and align ownership with long-term goals.

English

If it turns out Russini’s husband really did hire a PI and they’ve had all this info for years and just been sitting, waiting, crafting the perfect moment to go completely nuclear and ruin everyone’s lives and careers involved…

Dude needs to be hired by an NFL organization. I mean the patience and planning alone

English

@dylan522p @AnthropicAI Looks like yellow, green and aqua blue just went on vacation....

English

Claude Code spend had gotten to $10.95M runrate peak at SemiAnalysis

But then Opus 4.7 saved me.

More token effecient for tasks, smarter, and no fast mode.

Thank you @AnthropicAI

You saved me from bankruptcy

English

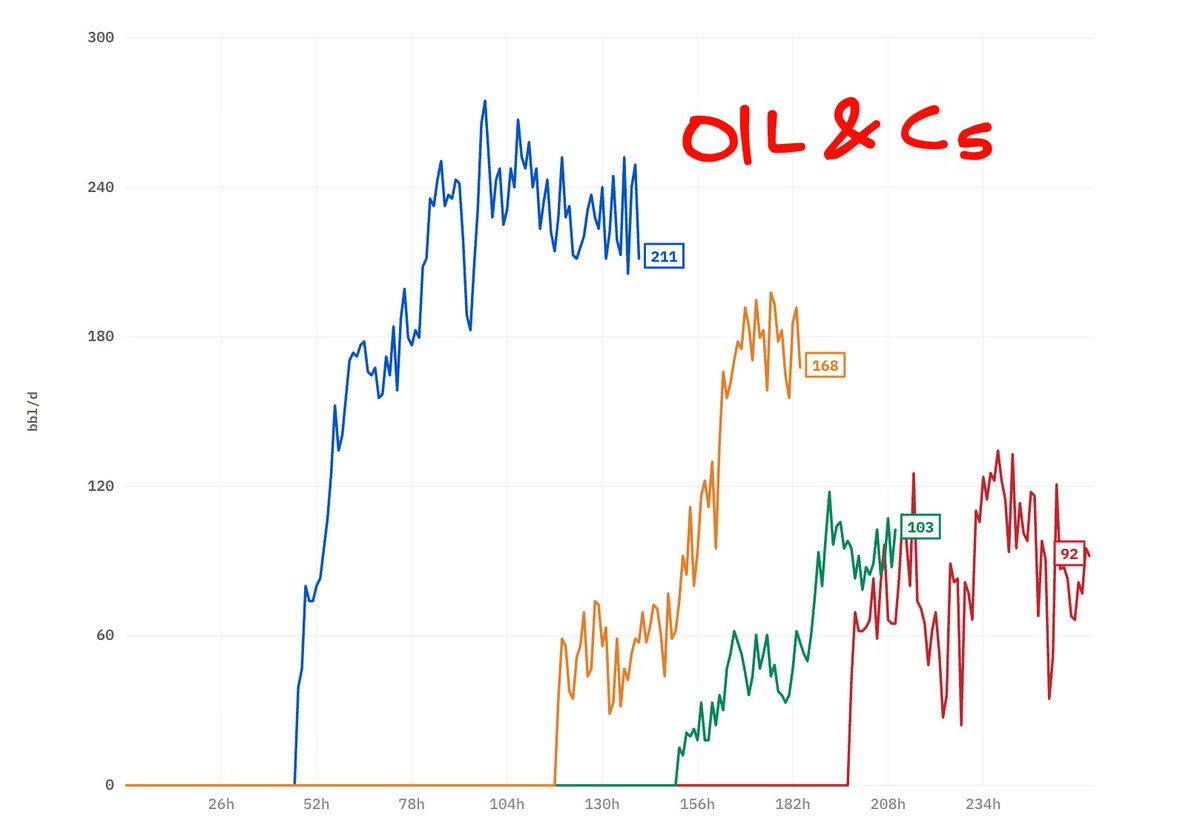

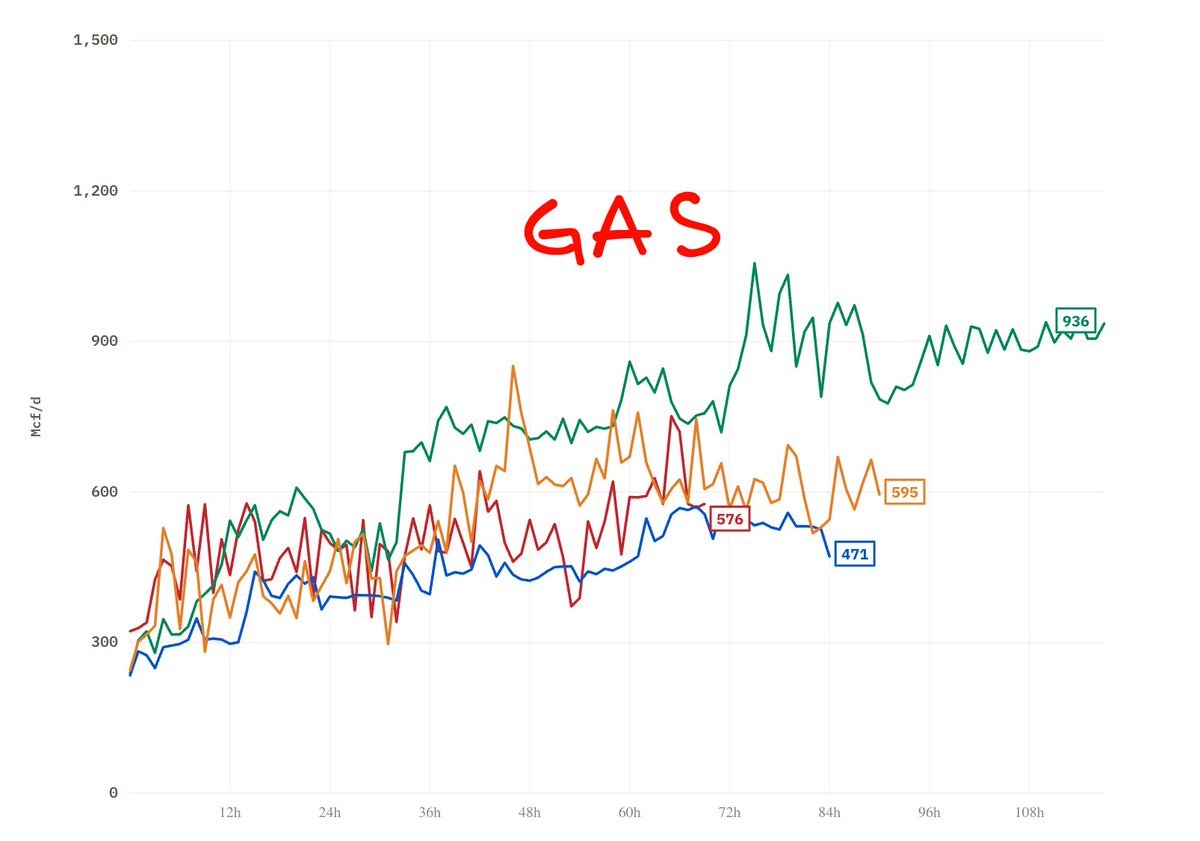

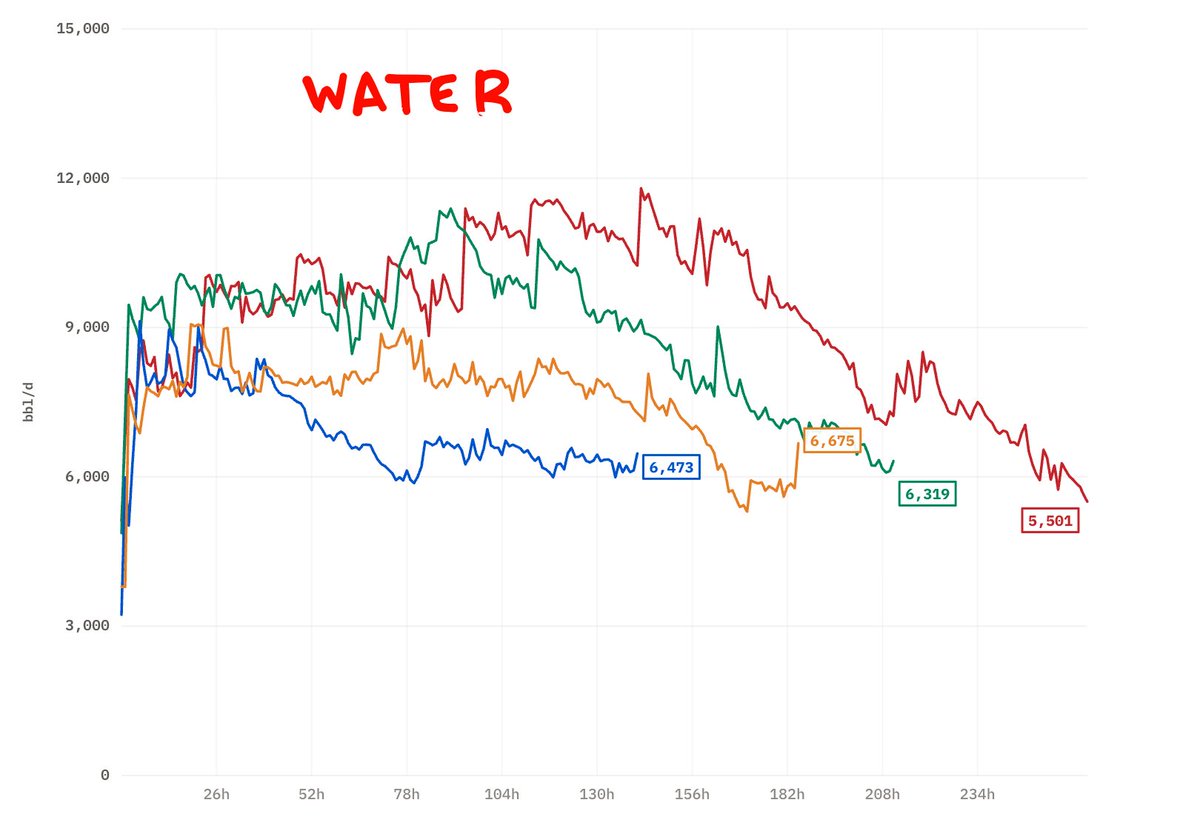

ARC has filed the well tests for their 4 Lower Montney wells. These four charts show the test rates throughout the final in-line flowback period. In the next tweet is an offsetting Upper Montney well for comparison.

Michael Spyker@ShaleTier7

Again, no opinion just the facts -- ARC Attachie production data through February 2026. Overall production is still ~14,000BOE/d less than the original nameplate, but capital has been limited materially, so that's to be expected. The 03-12 pad they brought online last December is cleaning up, with water rates now at ~1,000-1,500Bbls/d and raw gas rates now stabilizing at ~2.0-2.5MMcf/d, this would imply condensate peak IP30 rates of ~400-525Bbls/d. They brought a Lower Montney pad online which I've highlighted with the map attached. These wells were spaced wider than the Upper wells, but don't have any material production data to judge them with yet. March we'll watch for production from the Lower Montney wells, along with how the 03-12 pad continues to perform in what was the 'core' of the Phase 1 start-up area.

English

@secretlyaninja This is an interesting idea. How do you think about the fee drag on the BDCs and that impact on the longrun value vs. NAV?

English

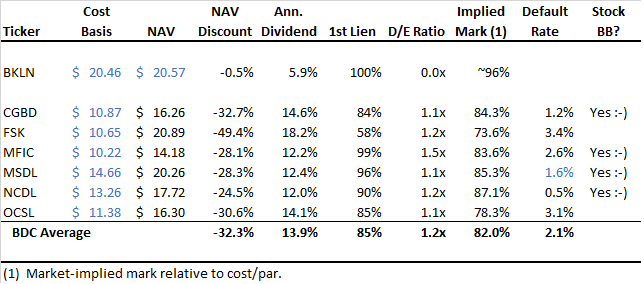

Even if short fee rate doesn't normalize, my cost of carry is only -1% per yr. If it normalizes, I should be getting paid 7.5% per yr. Getting paid that amount to hold a position with good r/r sounds good to me. $CGBD $FSK $MFIC $MSDL $NCDL $OCSL $BKLN

English

I went long a basket of BDCs ( $CGBD, $FSK, $MFIC, $MSDL, $NCDL, $OCSL) & shorted $BKLN against it. Negative vibes against private credit has reached a fevered pitch & BDCs are now mispriced vs leveraged loan comps. Thread on my thesis. 🧵 (1/n)

English

@MaldenDriveCap @DonutShorts I think there is a real chance of lawsuits which further erode enterprise value.

Lending is a business built upon trust, I think they will have real problems rolling their debt which could trigger a death spiral. I would find it interesting at equity like returns >15% yields

English

The #GetMeOut bond of the day

$GSYCN 9 1/4% of 28

Who knew subprime auto could be a problem?????

English

@BrownMarubozu Perfect, I am aware of this and agree with (old) buffet.

No where does he say this is a metric he looks at for valuation purposes. It’s the same way a bank with low cost sticky deposits has an asset, but you don’t see me adding them to its BV.

English

@OutSkied He doesn’t state it directly but I inferred it from his writings and comments on insurance float. The link below is particularly good at encapsulating the concept.

Maybe you are more a young Warren Buffett!

youtu.be/qDuWOkD0d5E?si…

YouTube

English

Greg Abel making it clear that $BRK does not trade below intrinsic value which is true if measured by the Buffet method (float + BV). $FFH.TO on the other hand trades at a giant discount to that measure and has retired a third of the shares in the last 8 years net of TRS.

Brown@BrownMarubozu

One way to measure intrinsic value that I call the Buffett method is to add BVPS + FPS (float per share). $FFH.TO trades at a giant discount using this methodology while $BRK trades at a premium. Another way to gauge a fair P/B multiple is to compare to ROE.

English

@kieranwgoodwin Totally agree. I am now long a small position as the valuation is egregious, I pray kkr is embarrassed by the product and either takes us out of our misery or takes steps to clean it up. This is a classic case of Wall Street greed and bad incentives.

English

If a Retail Investment Product Hall of Shame existed,

$FSK would be a first ballot member.

Babe Ruth credentials:

* started as non-traded BDC in '09 scalping investors for 7-10% intial sale charge

* compounding at whopping 1.50% since coming public in '14

* GP "earning" $2.5bn of fees since '14

* trading 52% of NAV and GP will not commit to using realization to buying back stock since it would reduce their fees

PLEASE REMEMBER PERMANENT CAPITAL DOES NOT EXIST!!

THE MANAGER IS HIRED BY THE BOARD EACH YEAR

English

@yummyCenturyEgg How much pricing power has $csu pushed through historically? I generally agree with your macro view here, I just dont know if this is actually the case with CSU

English

For whom the Bell Curves - $CSU

"Any man's death diminishes me... never send to know for whom the bell tolls [curves]; it tolls [curves] for thee." - John Donne.

$CSU is a real "compounder". But once you start on the bell curve formation, you don't stop until you complete the "constellation". Don't ask me why, that's the law. I have a special aversion to companies that disrespect their customers by raising prices dramatically. Compounder bros who are retarded view that as pricing power. I view that as the bell tolling. This is true especially for canadian compounders. Again, don't ask me why, that's just is.

English

Agree, would add some of the AI fear names to the list as well, eg. $spgi

Arrakis Global@ArrakisGlobal

First time in years, I think going large cap quality, you actually have great r/r across sectors. $MSFT $BX $LVMH type of names in 25-40% drawdowns Probably go 50% long here. Wait for a potential flush and then the other 50% 2022 I got way too cute when Big Tech was a buy

English

@BrownMarubozu @MrDavidThomas I'm seeing a BVPS of $53 in 1995 vs $1250 today. Looks like a CAGR of ~10%, I'll even give credit for a dividend of ~1% and call it 11%. My capiq doesnt good back further but it seems like we are putting a lot of weight on the period from 1985 - 1995?

English

@OutSkied @MrDavidThomas How do you suppose they compounded BVPS 18%+ since inception while averaging 10% ROE? Why doesn’t every company do it?

English

Cue the 'annoying fanboys' and girls at #COBF. Go! 😉 Actually, this is fintwit at its best. Valid points. FFH made mistakes. The real surprise is after a 4 yr rebound, it's still cheap by PE and BV.

Investors just need to guess: Will it fizzle, maintain or accelerate? 🤷♂️

SkiedOut@OutSkied

$ffh.to hate incoming. No group has more annoying fanboys on twitter My beef’s with ffh include the following 1) questionable investment performance for over a decade (drawdowns like this would get you fired anywhere else) 2) the swaps on your own stock 3) the deals with OMERS

English

@OutSkied @Triviumpartnrs The crap ROEs and bad investments allowed us to buy in at 0.7x BV. What's not to like?

English

$ffh.to hate incoming.

No group has more annoying fanboys on twitter

My beef’s with ffh include the following

1) questionable investment performance for over a decade (drawdowns like this would get you fired anywhere else)

2) the swaps on your own stock

3) the deals with OMERS

English

@Triviumpartnrs I would rather companies just buy back shares with real liquidity vs. Using a cashless swap which has liquidity needs that are highly correlated with my business performance. But what do I know

English

@OutSkied Company insiders can see how their business drivers are evolving - unlike some shit co ticker you own.

About your liquidity comment - FFH owned $30bn+ of UST at the time & had an incredibly liquid balance sheet. I suggest model it out

English