Paulo 🇩🇪🇺🇸

34 posts

Paulo 🇩🇪🇺🇸

@PauloGoeb

@CashApp, @AfterpayUSA, @Ripple, @ProsperLoans, @UCLA math

San Francisco, CA Katılım Aralık 2015

7 Takip Edilen18 Takipçiler

@UrataSyndicate @Simonkhalaf @davidmarcus out of the three things I list, the challenge for robinhood imo is narrative cohesiveness. their "robinhood social" play is an interesting attempt to connect the dots but we'll see if that lands

English

@Simonkhalaf @PauloGoeb @davidmarcus Robinhood is still where it's at. They've got speed and focus and relentless execution

English

A few thoughts about PayPal, nearly 12 years after I left.

I woke up this morning to dozens of messages from former PayPal colleagues. It pushed me to finally speak up.

I never spoke publicly about the company after I left. Part of that was loyalty to John Donahoe, who gave me an unlikely opportunity, handing the reins of PayPal to a startup guy who, on paper, had no business running a then 15,000-person organization. But part of it was something else: I had left. I chose not to stay and fight for the changes I believed in. Speaking from the sidelines felt like armchair commentary. Easy opinions without the burden of execution. So I stayed quiet.

But twelve years of silence is long enough. And today's news makes it clear the pattern I've watched unfold isn't self-correcting.

I left PayPal in 2014 because I was deeply frustrated. We had executed a silent turnaround of a company that had lost its soul. We brought back engineering talent, shipped good products quickly, and acquired Braintree and Venmo. The company was on a tear. So much so that Carl Icahn felt compelled to accumulate a position in eBay and push for a PayPal spinoff. At the time, eBay decided to fight Icahn.

It was a difficult period for me, caught between what I felt was right for PayPal and my loyalty to the eBay team.

This is when Mark Zuckerberg approached me to join Facebook. The combination of his conviction that messaging would become foundational, the appeal of going back to building products at scale, and my growing exhaustion with the internal politics at PayPal and eBay eventually convinced me to leave and join one of the best teams in the world, one I had admired for a long time.

In the summer of 2014, I met John in a café in Portola Valley and told him I had decided to leave. During that conversation, he told me that Icahn had effectively won the fight, that PayPal was going to become an independent company, and he tried to convince me to stay on as CEO, but I had already said yes to Mark, and my word is my bond. There was no turning back.

After my departure, the board scrambled to find a replacement, and it took a few months for them to land on Dan Schulman. The leadership style shifted from product-led to financially-led. Over time, product conviction gave way to financial optimization.

Much of the momentum we had created still persisted and carried the company forward, mainly driven by Bill Ready, who came over in the Braintree acquisition and rose to COO. Under his leadership, Venmo grew exponentially, and total payment volume (TPV) accelerated quickly. But the shift under Schulman became more pronounced after Bill's departure at the end of 2019. With him went the product conviction that had defined the post-spinoff momentum. Then, for a period, COVID-fueled online shopping hid a lot of the company's new weaknesses.

During that period, the company made a fundamental miscalculation: it optimized for payment volume instead of margin and differentiation. It leaned into unbranded checkout, where PayPal had the least leverage, instead of branded checkout, where the margin, data, and customer relationship actually lived.

Visa masterfully structured a deal that effectively ended PayPal's ability to steer customers toward bank-funded transactions, which had been a core driver of PayPal's economics. Not long after, PayPal lost a significant portion of eBay's volume. Over time, it saw its share of checkout among its most profitable customers steadily erode as Apple Pay and others continued to execute well.

The same pattern repeated itself across lending, buy-now-pay-later (BNPL), and new rails.

On lending, PayPal missed the opportunity to turn it into a platform weapon. Products like Working Capital were conservative, short-duration, and optimized for loss minimization. Lending never became programmable, never became identity-driven, and never became a reason for merchants or consumers to choose PayPal over something else.

The missed opportunity in BNPL was even more striking. Klarna, Affirm, and Afterpay didn't just offer installment payments, they built consumer finance brands, persistent credit identities, and new shopping behaviors. PayPal saw the BNPL turn, entered the market, and had every advantage: distribution, trust, and merchant relationships. But BNPL was treated as a defensive checkout feature rather than an offensive category. There was no attempt to turn it into a core consumer relationship, no super-app behavior, and no meaningful differentiation for merchants. Others built platforms, PayPal added a feature.

The failure to lean into building and owning new rails followed the same logic. After the spinoff, PayPal had a once-in-a-generation opportunity to build a global, at scale payment network. Instead, the company focused on building on top of existing networks and third-party rails.

More recently, that mindset carried over to PYUSD. Technically, the product was sound. Strategically, it launched without a compelling transactional reason to exist. PYUSD had distribution, but no organic demand. It was not embedded deeply enough into flows to become a true settlement layer, a cross-border merchant rail, or a programmable money primitive. It sat adjacent to the product instead of inside the core of it.

Acquisitions during this period followed a similar pattern. Honey was not a strategic acquisition for PayPal. It added activity, but not leverage. It lived outside the transaction, monetized affiliate economics rather than payment economics, and never meaningfully strengthened PayPal's control of the customer or the checkout moment. Xoom solved a real problem in remittances, but it never compounded PayPal's advantage. It scaled volume without changing the underlying rails, identity graph, or settlement model, and as importantly, it didn’t cater to a high-value, high-margin customer archetype.

None of these were bad companies. They were just a wrong fit for PayPal and became unnecessary distractions.

The board eventually recognized the problem. In 2023, they brought in Alex Chriss, an Intuit veteran with a strong product background, explicitly to restore product conviction. It was the right instinct.

But Alex came from software, not payments. He understood SMB product development. He didn't have the muscle memory for transaction economics, network effects, or settlement infrastructure.

In hindsight, he also made an error: clearing out much of the leadership team that understood payments deeply. Executives with years of institutional knowledge departed within his first year.

This morning, Alex was removed as CEO. Branded checkout grew 1% last quarter. The board tapped another operator, Enrique Lores, the former HP CEO who's been on the PayPal board for five years.

I don’t know Enrique. And he might be a great leader, but on paper at least, he’s a hardware executive. For a payments company.

The common thread through all of this is incentive design. Once PayPal became independent, short/medium-term predictability beat long-term vision and ambition. Stock performance mattered more than platform risk and network opportunity. Financial optimization replaced product conviction.

I'm not claiming I would have made every call differently. Running a public company at scale involves tradeoffs I didn't have to make after I left. But the pattern, choosing predictability over platform risk, again and again, was a choice, not an inevitability.

Over time, the company that had every advantage and could’ve become the most consequential and relevant payments company of our time, lost its mojo, its product edge, and its ability to compete in a market that’s being rewired and reinvented in front of our eyes.

That's the part that's hardest to watch for a company I care so deeply about.

English

@Simonkhalaf @davidmarcus alas, @davidmarcus's old post on the demise of Libra/Diem (x.com/davidmarcus/st…) shows how gov't ambiguity and perniciousness around crypto makes that path a difficult one

David Marcus@davidmarcus

How Libra Was Killed. I never shared this publicly before, but since @pmarca opened the floodgates on @joerogan’s pod, it feels appropriate to shed more light on this. As a reminder, Libra (then Diem) was an advanced, high-performance, payments-centric blockchain paired with a stablecoin that we built with my team at @Meta. It would’ve solved global payments at scale. Prior to announcing the project, we spent months briefing key regulators in DC and abroad. We then announced the project in June 2019 alongside 28 companies. Two weeks later, I was called to testify in front of both the Senate Banking Committee and the House Financial Services Committee, which was the starting point of two years of nonstop work and changes to appease lawmakers and regulators. By spring of 2021 (yes they slow played us at every step), we had addressed every last possible regulatory concern across financial crime, money laundering, consumer protection, reserve management, buffers, and so much more, and we were ready to launch. We had worked on a slow rollout of a limited pilot that some members of the Fed’s Board of Governors were supportive of. At last, Chair Jay Powell was ready to let us move forward in a limited way. The story, as I heard it, is that Jay Powell was told by Treasury Secretary Janet Yellen at one of their biweekly meetings that allowing this project to move forward was “political suicide,” and she would not have his back if he let it happen. I wasn’t in the room when this conversation happened, so take these words with a grain of salt, but effectively this was the moment Libra was killed. Shortly thereafter, the Fed organized calls with all the participating banks, and the Fed’s general counsel read a prepared statement to each of them, saying: “We can’t stop you from moving forward and launching, but we are not comfortable with you doing so.” And just like that, it was over. One essential point is worth making here. There was no legal or regulatory angle left for the government or regulators to kill the project. It was 100% a political kill—one that was executed through intimidation of captive banking institutions. That was the hardest part of this story for me personally. Not that we had failed, but that America, this country I immigrated to and became a proud citizen of because of its rule of law and value system, behaved in such a way for political reasons. It was a very tough pill to swallow. The bright side of the story, though, was the many learnings from this wild ride. By the end of the project, we had made so many concessions to get a thumbs-up that the whole design of the network became a Frankenstein of our initial ambitions. We also learned the biggest lesson of all, which is that if you’re trying to build an open money grid for the world—eventually moving trillions of dollars a day, designed to be here 100 years from now—you have to build it on the most neutral, decentralized, unassailable network and asset, which, hands down, is Bitcoin. And now this is what many of us who went through this scarring journey are building together at @Lightspark. And this time, we won’t stop until we get it done!

English

@PauloGoeb @davidmarcus and if you don't want the US Dollar or banking system, put all the energy on crypto) and nothing else.

English

@Simonkhalaf @davidmarcus +1

product focus, scale/connectivity, and narrative cohesiveness are massive challenges across all of tech these days -- and nowhere moreso than in fintech

English

Great write-up. I would also offer another perspective. Lack of focus under the departing CEO, I even couldn't keep up with what paypal is doing and I know software and payments. Between Venmo, PayPal (the app sucked), ads, Crypto, SMB lending, SMB non-lending, Braintree, FastLane, PayPal World, PayPal Debit, PayPal Open (which I never understood) and AI (Lip Service). This is a sum of parts. This is not product.

English

@torovictorioso @CashApp Lots of really good ideas! Happy Thanksgiving

English

How will @CashApp UX evolve over the coming years .. here is what I think. Happy thanks giving to all .. enjoy 👇

open.substack.com/pub/torovictor…

English

@nachunja "To summarize: The percent of national commerce with a Cash App customer on one side and a Square merchant on the other is tiny."

^ if you change this to an "or" statement, that number is huge.

the gap between "and" and "or" is...kinda the point of Neighborhoods

English

@KevinTCottrell For once, I see where MJ is coming from. I'd consider that comment intentionally antagonistic.

English

I was kind. I didn't tell him directly that he needs to be fired. I didn't bring up the supposed tax fraud. I didn't talk about how he ruined our athletic department or how he botched coaching hires. I shared my opinion and repeated his own line he gave us 2 years ago.

English

Before the game today, I ran into Martin Jarmond and said to him

"Hey Martin, read the room. We don't want to go to SoFi."

His response was

"Why do you tell me to read the room? Why cant you be kind?"

#firemartinjarmond

@UCLAFootball @UCLAchancellor

English

$XYZ

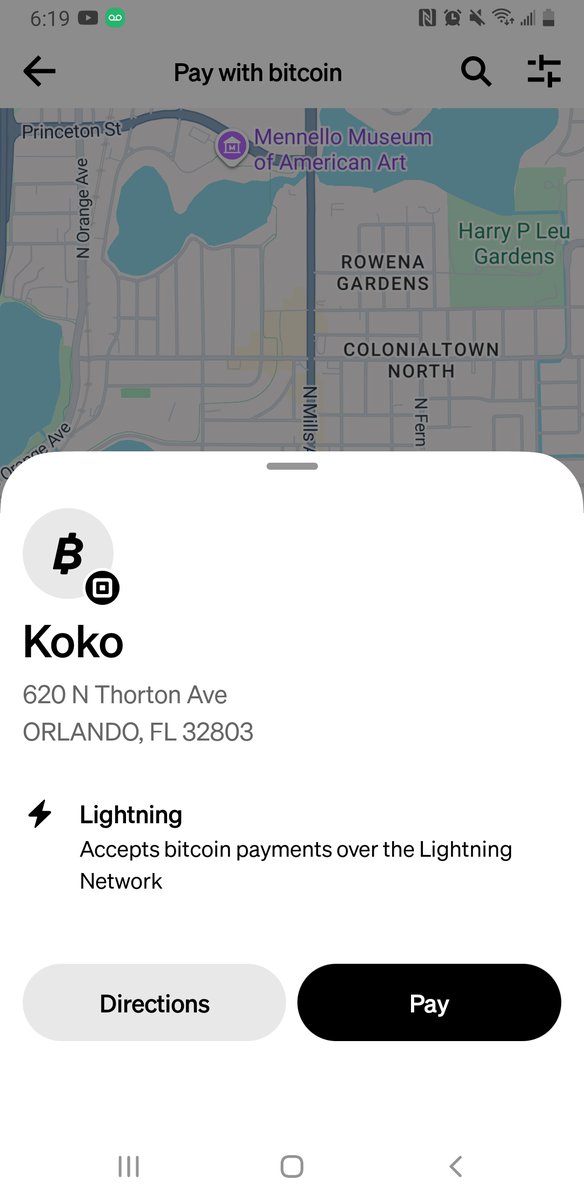

• Converted Koko Kagigori Cafe (Orlando, FL) to a bitcoin Seller. Amazing drinks - check them out.

• Added +2 to Cash App MAU

• Introduced Neighborhood on Cash App

The owner heard of bitcoin, but didn’t know or care about them (99% of ppl probably). When I asked him whether he turned on bitcoin payments, I was met with a ‘wtf is this guy talking about’ look.

But when I told him he would

1. not pay 3% processing fees

2. his cafe would show up on Cash App Map

3. bitcoin fans will seek out his cafe

His attitude changed 180 degrees. He started complaining about payment fees and how he is sick of them. I showed him Cash App Map and he was amazed.

Suddenly he became a motivated person eager to turn it on.

Then he asks, “so I have to make a bitcoin wallet and connect to Square or something?” I told him it takes two clicks from his Square Dashboard. His face was 🤯

While I’m having the delicious shaved ice, he comes out and says he got it to work. I happily go and pay but QR code method was very finnicky and didn’t work right away, not because it was bitcoin but just the nature of QR codes. Ensured him NFC is coming.

Ofc, I shill Neighborhood on Cash App while I’m at it. His interest level was at max. “You know how Uber Eats charges you 15-30%? Cash App will charge you 1%” His mind was 🤯.

As I walk out, I can hear him ask his employee whether she has Cash App and telling her to download it.

There are hundreds, if not thousands like me, that will shill Square and Cash App without being an employee. CAC will stay low.

English

@nachunja people will rightly key in on visa and mastercard, but there are companies everywhere that fleece merchants and consumers while offering little of value: fico, ticketmaster, etc etc

English

Watched the entirety of Block's $XYZ investor day today. I think that it will become the pre-eminent fintech company in America.

When I say fintech, I mean they will enable access to capital to everyone everywhere all the time. They will become THE financial platform for individuals and businesses.

One thing that stood out to me was @jack saying he wanted to automate the entire company. I believe that is possible and I believe they will essentially do that—only a matter of how quickly.

I believe they are focusing on the one metric that matters: iteration cycle times.

The companies that enable themselves using AI will drastically cut down iteration times, allowing them to ship faster, better, and cheaper than competitors. This growth will only compound over time, and the companies that get started early will become magnitudes more powerful than their peers.

I believe Block is nonpareil when it comes to reducing iteration cycles as an entire organization across all departments in their vertical. I am talking marketing, sales, operations, finance, etc.

In my opinion, Block is one of the most exciting companies in the world.

Neighborhoods is also a moat in the making.

English

@bobspaysubstack Good take! Only point of disagreement is that opportunities for long-term differentiation in Cash I think are actually material 👀

English

Block $XYZ Quick Hit:

$XYZ is a name I’ve warmed to recently. My main concern with $XYZ will always be with Cash App and the durability of its growth in an increasingly competitive market for basic financial services, where opportunities for long-term differentiation are limited. On the other hand, I’m more optimistic about @Square medium-term prospects than I have been in some time. I believe the company’s renewed focus on innovation and investments to expand distribution have put @Square at the front-end of a period of above-market growth in the U.S. and highly attractive growth in international markets, where the secular opportunity from combining payments and software is more significant. My decision point on $XYZ remains an acceleration in Cash App Card volume growth. While there are initiatives in flight to facilitate this turn, I believe, based on all the evidence I have seen, that Cash App Card volume growth is still slowing. A final word on $XYZ: I believe that when one looks objectively at my Payments Scorecard and eliminates any personal biases, which I admittedly may have, Block screens as among the best opportunities.

bobhammel.substack.com/p/the-week-tha…

English

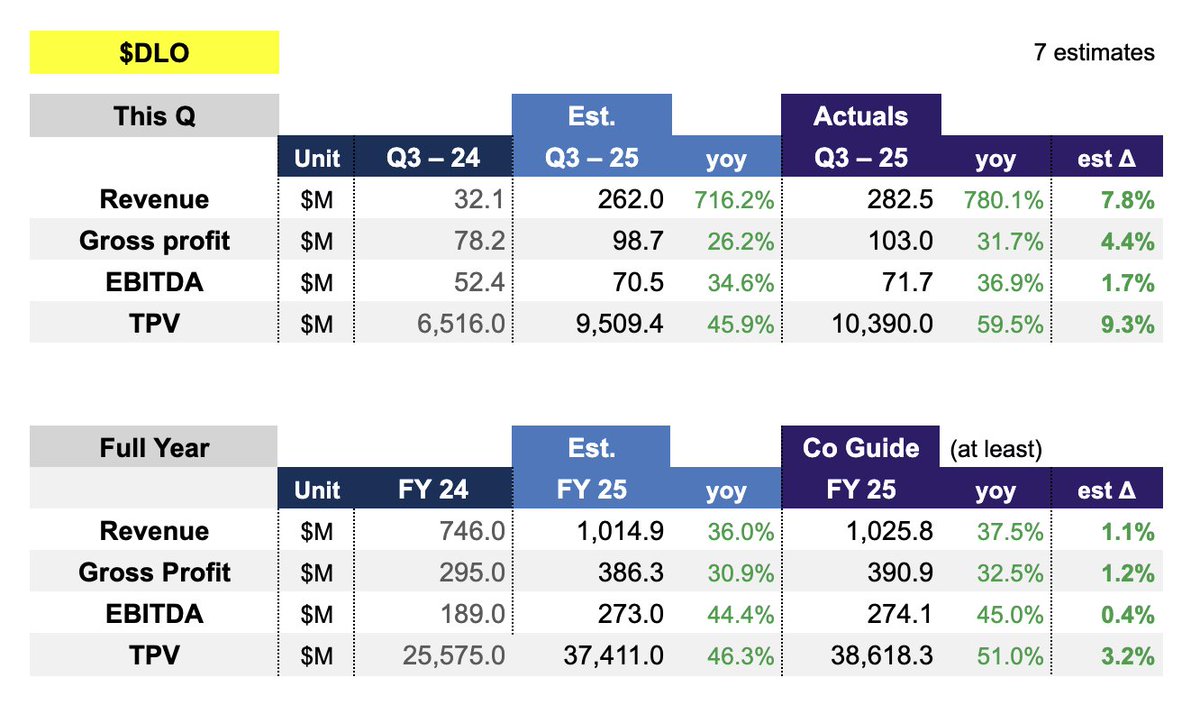

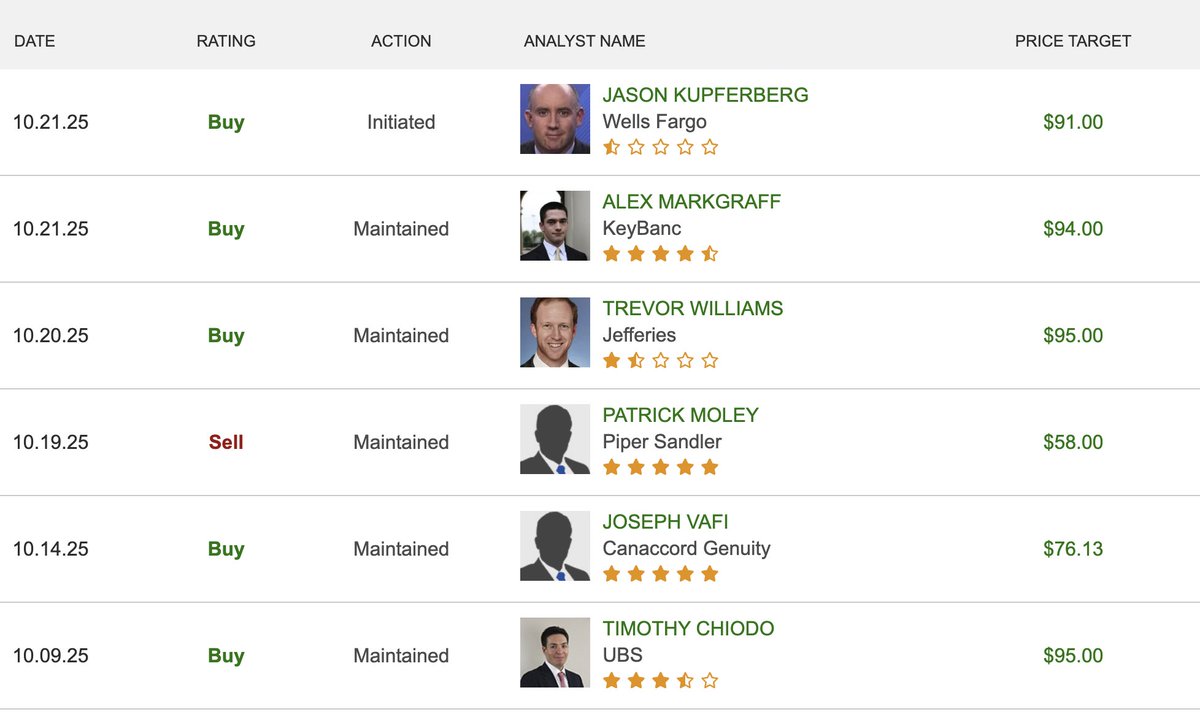

$XYZ – Latest Analyst PT

• Piper Sandler with a "SELL" rating

• Weird PT by Canaccord

Good to have some mixed views going into earnings.

Cute Baby@nachunja

$XYZ – Latest Analyst PT

English

Come to think of it, this is where $XYZ / @blocks could really shine.

@Square just launched Square AI to help sellers answer questions and better analytics, why not extend that to @CashApp with a buyer-facing agent?

Imagine buyers chatting with sellers (or their agents) directly in Neighborhoods for recommendations/discovery, order placements, real-time support.

With both sides of the neighborhood network, Block could bridge LLMs and payments better than anyone.

ValueHodler@ValueHodler

"Internet hands" assumes three miracles will happen simultaneously. 1. Perfect automation of intent (LLMs understand context deeply enough to transact safely) 2. Universal API access + trust 3. Zero-friction monetization alignment across industries. None of these exists today. It is a poetic analogy, but it's also a bit "misleading". Booking, insurance, jobs all involve risk, identity, and money. Delegation to LLM agents require trust and liability frameworks, not just UX. Most "doing" online requires structured contracts, compliance, payment auth, refunds, customer support etc. None of which LLM can natively solve. Agents can only assist today, not auto replace the whole stack. But this will be the next $100B frontier, rebuilding the economic rails that make the automation profitable, compliant, and reliable.

English

Incredible to see how much $XYZ has grown, when you zoom out

From card swiper gadget to payments powerhouse

Hopefully one day price action will reflect that 😂😂😂

Cute Baby@nachunja

34 year old @jack pitching @Square when revenue was $0. 15 years later, it's a S&P 500 company, doing $10B in annual revenue. $XYZ

English

@cam_mulvey once late on an afterpay payment plan, you cannot place another order with afterpay

the NYT piece curiously mentions neither of these things.

the affirm ceo summarizes it well here: x.com/mlevchin/statu…

Max Levchin@mlevchin

Are you noticing more "opinion" pieces decrying BNPL for "normalizing debt" while overlooking that credit cards do the same, but cost you much more? With @Affirm you pay less (if any) in interest and no fees of any kind. So who benefits from these hit pieces? You? Or the banks trying to protect their credit card profits?

English

Klarna' means 'to become clear' in Swedish.

What's become clear: they designed a system where user debt spirals fund billion-dollar IPOs.

The confusion isn't accidental. The exploitation isn't collateral damage.

It's the product.

English

This NYT piece does solid work documenting how BNPL trapped a woman in $50K of debt.

But it misses the most important part: these aren't accidents. They're features.

Klarna went public at $19B while their users went broke. That's the business model.

Here are 3 tactics they used:

English

@cam_mulvey genuine question: how do you reconcile BNPL repayment rates against CC repayment rates?

at Afterpay, 98% of purchases incur no late fees and 95% of installments are paid on time.

English

Block Inc will be the leading provider of $BTC infrastructure. It‘s becoming more and more obvious. The rate of bringing Bitcoin product to market has been staggering lately.

Bullish $XYZ

Strike@Strike

Strike + Bitkey Buy bitcoin with no fees and automatically withdraw it to cold storage for free.

English