@thechartist Yes, refer to "Tickers" under the help section for reference of data length

testfol.io/help

English

QuantMechanic

165 posts

Govt to move ahead with plan to control rising rental costs The Namibian government will proceed with plans to cap housing and rental prices, with newly appointed Minister of Industrialisation, Mines and Energy, Modestus Amutse, confirming that finalising and tabling the long-awaited Rent Control Bill is among his immediate priorities. Amutse said housing costs have reached unsustainable levels, leaving many citizens unable to secure affordable accommodation. He stated, “Namibians are crying about high housing costs. We must work towards a bill that puts a cap on prices so that ordinary people can afford decent housing. This must be done in collaboration with the Ministry of Urban and Rural Development.” thebrief.com.na/2025/12/govt-t… #namibia #rentals #accommodation @MME_Nam @neab90091

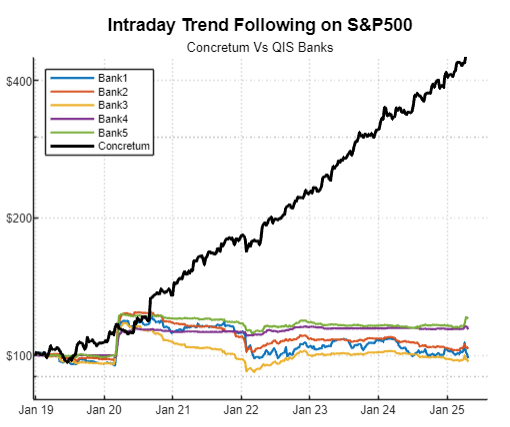

For the majority of stock traders trying to follow a systematic approach, this ... one ... thing ... : ) That is, if you want a 10 year CAGR = 22% like @thechartist ; ) Full Show: youtu.be/QOXwYn-lLNU