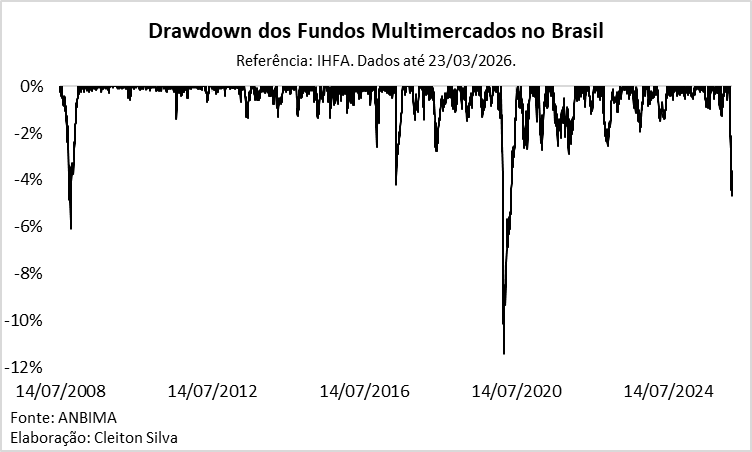

@Cleiton_CSJ O drawdown da série em excess return é mais válida para comparação histórica já que elimina o carrego.

Português

QuantBr

1.6K posts

@Quant_Br

Quant, PhD, machine learning. Finding signals in a noisy market.

@PeterHomer14 Calculate returns on each contract by doing ret(t) = price(t)/price(t-1) - 1, splice together the sequence of returns for each contract to get a continuous series, form a cumulative return index cumprod(1 + ret) and never think about prices again.