Rk Venkat

554 posts

🚨SpaceX set to IPO under the ticker $SPCX

SpaceX to begin trading June 12

🚀 THE NEW SPACE RACE IS ABOUT DATA CENTER

📈THE ANTHROPIC × SpaceX SIGNAL:

This is why every hyperscaler is moving up:

∙$AMZN → Project Kuiper

∙$GOOG → Starlink partnership + investments

∙$MSFT → Azure Space

∙Anthropic → infrastructure deals expanding into sovereign + edge compute

When SpaceX launches Starlink Direct-to-Cell and starts deploying V3 satellites with 1Tbps capacity — that’s the network layer of AI being rebuilt above the atmosphere.

The convergence is already happening:

∙Starshield (SpaceX’s classified gov division) is building dedicated DoD + intelligence constellations

∙Starlink is becoming the global low-latency backbone for AI inference at the edge

∙Lunar + LEO data centers are being prototyped (Lonestar, Axiom, Starcloud) — solar power is infinite in orbit, cooling is free in vacuum

HOW THESE 35 COMPANIES FIT THE ECOSYSTEM :

Think of the space economy as 5 layers stacked vertically — same logic as the AI stack:

LAYER 1 — RAW MATERIALS & COMPONENTS (the “semis” of space)

$HXL · $BWXT · $TDY · $HEI.A · $KULR · $ATRO · $RDW

Carbon fiber, nuclear cores, sensors, batteries, composites. Without these, nothing flies.

LAYER 2 — PRIMES & MANUFACTURERS (the + Foundry” layer)

$LHX · $LMT · $NOC · $RTX · $BA · $GE · $HON · $ESLT · $BAESY · $EADSY

Defense + aerospace giants that build the actual spacecraft, missiles, and satellite buses. Backlog, government cash flows.

LAYER 3 — LAUNCH moving (payloads to orbit)

SpaceX · $RKLB · $FLY · $SPCE

The cost of access. SpaceX has collapsed $/kg by 20x. Rocket Lab is scaling Neutron. This is the enabling layer for everything above.

LAYER 4 — DATA & CONNECTIVITY (the “cloud” layer)

$AMZN · $IRDM · $GSAT · $VSAT · $TSAT · $SATS · $SPIR · $PL · $ASTS · $SATL · $BKSY

Satellite networks. Earth observation. Direct-to-cell. This is the AWS of space — recurring revenue, subscription models, AI-ready data pipelines.

LAYER 5 — APPLICATIONS (the “AI/SaaS” layer)

$PLTR · $LDOS · $TRMB · $KTOS · $SIDU · $LUNR · $VOYG · $MNTS

Mission software, geospatial intelligence, lunar infrastructure, in-space services. Where the margin lives.

English

Play to watch in Physical AI

🤖 Robotics & Automation

Humanoids, service robots, warehouse bots, field robotics

Core Platforms & Robotics Builders

$TSLA – Optimus humanoid platform

$XPEV – Humanoid robotics + autonomy

$HYMTF – Advanced humanoid R&D

$RR – Service & field robotics

$SERV – Last-mile delivery robots

Warehouse & Logistics Automation

$SYM – AI-powered warehouse robotics

$AMZN – World’s largest robotics deployment

$ZBRA – Vision, tracking, automation infrastructure

🚗 Autonomous Vehicles

AI that drives, navigates, and makes real-time decisions

Autonomy & Driving Intelligence

$TSLA – Full-stack autonomy

$XPEV – AI-driven autonomous driving

$MBLY – Vision-based autonomy platform

$QCOM – Edge AI compute for vehicles

Perception for Autonomy

$INVZ – Automotive LiDAR

$LAZR – Long-range LiDAR

$OUST – Digital LiDAR

$ARBE – 4D imaging radar

🏭 Smart Factories

Industrial robots + AI-driven production systems

Industrial Robotics & Control

$ABB – Industrial robots & automation

$TER – Collaborative robots (cobots)

$HON – Industrial controls & sensing

$ROK – Factory software & automation

Manufacturing Intelligence

$PATH – Process automation bridging digital → physical

$PLTR – AI-driven industrial decision orchestration

🏥 Healthcare

Precision, repeatability, and high-margin Physical AI

Medical Robotics & Surgical Systems

$ISRG – da Vinci surgical robotics leader

$PRCT – Next-gen robotic surgery

$SYK – Robotic surgical instruments

$MDT – Robotic-assisted medical devices

🛰️ Defense & Space

Autonomous systems in high-risk, high-complexity environments

Autonomous Defense Platforms

$AVAV – Unmanned aerial systems

$RCAT – Autonomous drones

$UMAC – Tactical autonomous vehicles

$ONDS – Secure AI communications

Field, Extreme & Space-Adjacent Robotics

$OII – Subsea robotics & offshore autonomy

$FARO – 3D sensing, mapping & inspection

$RR – Robotics for extreme environments

🧠 Foundational Layer (Powers All Categories)

Brains behind Physical AI

$NVDA – AI compute backbone

$AVGO – Custom silicon + AI networking

$QCOM – Edge AI processing

Physical AI isn’t one sector.

It’s a stack deployed across five massive industries, each monetizing autonomy in different ways.

Most capital is still chasing software AI.

Robotics + real-world deployment is the next leg.

Not a financial advice,

Like and share if you like .

English

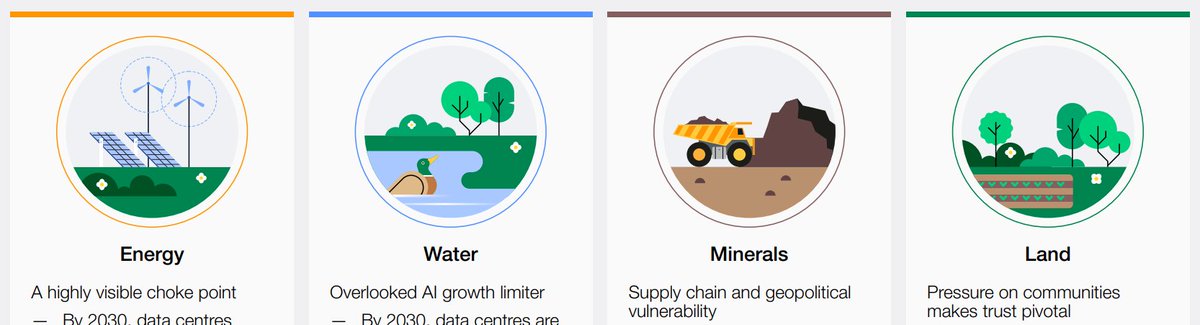

Overlooked AI supply chain chokepoints:

According to new analysis from World Economic Forum.

1. Energy

2. Water/Cooling

3. Minerals

4. Land

List of key names in each chokepoint:

-

1. Energy:

- $GEV: one of only Western HD gas turbine OEMs + $163B AI backlog.

- $VST: 2nd largest U.S. nuclear operator + 20 yr PPAs w/ $META & $AMZN AWS.

- Mitsubishi Heavy (7011): HD gas turbines, Sold out into 2028 w/ 2x capacity expansion planned to meet demand.

- Siemens Energy: huge order book €136B w/ 60% of turbine orders tied to data centers.

- $BE: 2.8 GW MSA for $ORCL fuel cell capacity + Brookfield $5B AI infra partnership to deploy fuel cells across AI factories globally.

- $FLNC: battery energy storage systems + software e.g. Mosaic. MSA w/ 2 hyperscalers.

-

2. Water/Cooling:

- Daikin Industries (6367): Critical fluoro/refrigerant supplier for low-GWP coolants used in direct-to-chip systems.

- AGC (5201): fluorochemicals + electronic materials (CMP slurries, mask blanks).

- $MOD: chillers + CDUs + data center coils. DC segment growing 50%+ + approaching ~30% of rev.

- $NVT: liquid cooling enclosures + busways, Partner in $NVDA Blackwell ecosystem.

- AVC (3017): named by $NVDA at GTC 2026 as one of four standardized cold-plate suppliers for Vera Rubin.

- Auras Technology (3324): $NVDA GB300 cold plates 25% mkt share. $AMD vapor-chamber certified.

- Delta Electronics (2308): Co-leader w/ $VRT in CDUs for GB200 racks.

- Wiwynn (6669): hyperscaler ODM rebuilding around liquid-cooled MGX/HGX racks.

-

3. Minerals:

- $FCX: largest publicly traded copper producer

- $MP: permanent magnets critical in DC HVAC + robotics.

- $AXTI: InP, GaAs substrates for optical interconnect (CW laser sources for CPO)

- $IQE: Epi wafers for VCSELs.

- $VNP: Gallium/germanium oxides for semiconductor substrates.

- Tri Chemical Laboratories (4369): Hafnium precursors for high-K gate dielectrics. Sole-source positioning into $TSM / $INTC / Samsung.

- Tokuyama (4043): Japanese poly + IPA + photoresist materials. Multi-product AI semi supply chain exposure.

-

4. Land:

I don't personally see much alpha in land.

But AI campuses need large footprints for compute, power + cooling.

-

There are honestly so many names in each chokepoint lol.

So have to focus on purer-plays where AI-driven revenue drives a significant % of company growth.

English

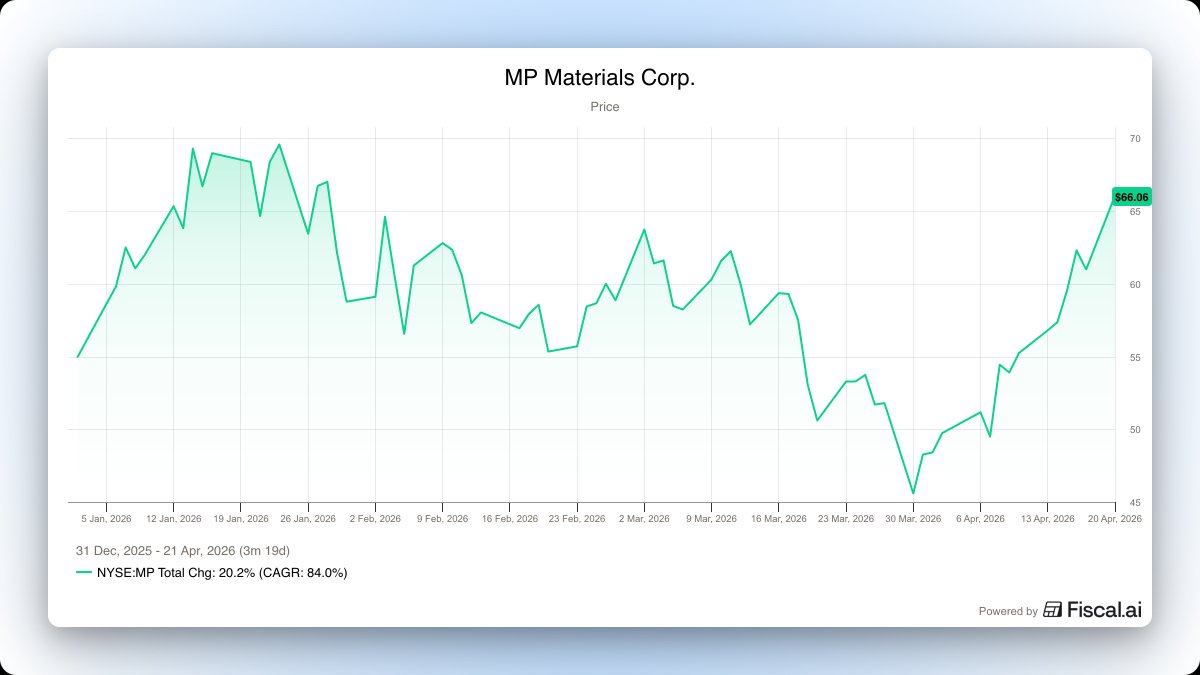

5. $MP - MP Materials

The Pentagon invested $400M and signed a 10-year off-take agreement. The DoD is now MP's largest shareholder. Only vertically integrated rare earth mine-to-magnet supply chain in the U.S. Building a $1.25B+ manufacturing campus in Texas with 10,000 metric tons of capacity by 2028. The U.S. can't build missiles, jets, or guided weapons without rare earth magnets. MP is the domestic answer to China's supply chain.

English

The White House is telling you exactly where to invest with the new $1.5 trillion defense budget.

Here are 5 stocks I'll be watching closely:

1. $PLTR - Palantir

The Pentagon just designated Palantir's Maven AI as an official program of record across all five military branches. $13B in total Pentagon investment across all Palantir programs, up from $480M in 2024. Over 20,000 active military users. $10B Army contract consolidating 75 existing agreements into one. Palantir is becoming the operating system of the U.S. military.

English

$TEM The Market Still Misunderstands Tempus AI’s Role in the Frontier AI Era

Tempus AI is becoming one of the clearest examples in the market of a "stock lagging the company."

The share price has declined from highs and chopped around. The business keeps stacking material progress. Revenue growth remains strong. Diagnostics volumes are growing. Data & Applications is accelerating. Major pharma collaborations keep expanding. Tempus is building one of the most important proprietary AI moats in healthcare, and I think the market is still struggling to classify what it owns here.

The stock gets treated like a long-duration software name, healthcare growth name, or generic AI application company at a time when the market prefers semis, power, data centers, and obvious AI capex beneficiaries. That valuation bucket has worked against $TEM.

Tempus looks far more like proprietary healthcare intelligence infrastructure than a conventional SaaS company.

Its value is rooted in a scarce asset: longitudinal, multimodal, clinically integrated healthcare data that is extraordinarily difficult to reproduce. That data is paired with proprietary AI models, diagnostic algorithms, sequencing infrastructure, physician workflow integration, and life sciences tooling. The rise of frontier AI may increase the strategic value of Tempus’ data moat.

Eric Lefkofsky @lefkofsky made the point directly at the recent Morgan Stanley Technology, Media & Telecom Conference on March 3rd:

“But I think there’s pretty good consensus in like ’27, ’28, they’re hitting the ends of that. So more and more of those companies are coming to people like us saying, what data do you have? And I think the next frontier of fun is going to be the big frontier modelers trying to garner access to more and more proprietary data like the kind of data Tempus has to train their models. In our case, the data we have is really hard to replicate. First, you have to go to, in our case, I think, 5,500 of the roughly 8,000 hospitals in the United States and convince them they should give you their data, which is not quick.”

That quote is central to the thesis.

Frontier model companies like Anthropic, OpenAI, and Google Gemini, are increasingly going to need scarce, proprietary, domain-specific datasets as public training data becomes less useful at the frontier. Tempus owns one of the most valuable and hardest-to-replicate healthcare datasets in the world. Lefkofsky goes on to explain the process: legal approvals, hospital IT bottlenecks, systems integration, longitudinal patient data, structured data, unstructured data, physician progress notes, and other forms of clinical information that have to be assembled over time.

This is why the SaaS comparison misses the heart of the business. Tempus looks far more like proprietary healthcare intelligence infrastructure than a conventional software company. It monetizes data, diagnostics, clinical workflows, AI models, and diagnostic algorithms built on top of a healthcare dataset that took years of institutional integration to assemble.

I also would not be surprised if $GOOG Google/Alphabet, which still reported 1.55M $TEM shares worth roughly $70.1M in its latest 13F portfolio, eventually announced some kind of Gemini-Tempus partnership around healthcare AI and proprietary multimodal data. This is purely my speculation. The logic is easy to see from Lefkofsky’s comments. Frontier model companies increasingly need scarce, domain-specific proprietary datasets, and Tempus owns one of the most valuable healthcare data assets in the world. Alphabet’s continued Tempus position makes that possibility especially interesting to watch.

The financials are beginning to show the power of that structure.

Diagnostics generated $261.1M in Q1 2026 revenue, up 34.7% YoY, driven by 28% oncology volume growth and 54% hereditary volume growth. This is the clinical engine. It keeps Tempus embedded in real patient care, physician decision-making, molecular testing, and healthcare workflow.

Data & Applications generated $87.0M, up 40.5% YoY, with Insights growing 44.1% YoY. This is the higher-value AI, data licensing, modeling, and biopharma enablement layer. It shows Tempus evolving into a platform company with multiple compounding engines rather than a single-product diagnostics story.

The flywheel is getting harder to ignore:

• Diagnostics deepen the proprietary data asset

• The data asset improves AI models and diagnostic algorithms

• Those models and datasets support biopharma R&D

• The partnerships generate more revenue, strategic validation, and product pull-through

• More clinical activity strengthens the entire system

The 2026 news flow has been excellent:

• Q1 revenue rose 36.1% YoY to $348.1M, with gross profit up 43.1% to $222.0M

• Tempus raised 2026 revenue guidance to $1.59B-$1.60B and maintained an expectation of approximately $65M in adjusted EBITDA

• Merck expanded a multi-year strategic collaboration with Tempus focused on AI/ML-driven precision medicine, biomarker discovery, cancer resistance mechanisms, and oncology development

• Gilead expanded its multi-year collaboration with Tempus, including enterprise-wide access to its AI-driven Lens platform and broader multimodal datasets to support oncology R&D and real-world evidence generation

• Daiichi Sankyo entered a strategic oncology collaboration using Tempus’ proprietary foundation models, including PRISM2, to support biomarker discovery and patient stratification across an ADC clinical program

• Bristol Myers Squibb expanded its strategic collaboration with Tempus to apply AI, multimodal real-world data, and data science techniques across oncology and neuroscience clinical development programs

• USC and Tempus announced a strategic collaboration aimed at accelerating AI-driven precision medicine across patient care and research, with the USC system representing more than 1.5M annual patient visits

• NYU Langone Health entered a multi-year strategic collaboration centered on precision oncology, serial molecular profiling, and the development of AI-powered diagnostic tools and personalized therapies

• Northwestern Medicine selected Tempus to expand genomic testing access for oncology patients, including DNA and RNA profiling, liquid biopsy, MRD, and broader next-generation sequencing access

• Tempus launched automated Active Follow-Up, an AI-enabled clinical update service designed to provide ongoing therapy monitoring and context-aware notifications through its physician portal

• Tempus reported Total Remaining Contract Value above $1.1B at year-end 2025 and 126% net revenue retention. It also disclosed that it signed data agreements with 70+ customers during 2025, including $AZN AstraZeneca, $GSK GSK, $BMY Bristol Myers Squibb, $PFE Pfizer, $NVS Novartis, $MRK Merck, $ABBV AbbVie, Daiichi Sankyo, $LLY Eli Lilly, and Boehringer Ingelheim

That pharma list matters.

These are some of the largest pharma and drug developers in the world. They are increasingly using Tempus’ multimodal datasets, AI-enabled analytics, and platform capabilities for biomarker discovery, drug development, clinical trial design, patient stratification, and real-world evidence.

I think the market is still underappreciating what $TEM is becoming.

Diagnostics is growing. Data & Applications is growing faster. Insights is compounding at a high rate. Major pharma relationships are broadening. Proprietary models and diagnostic algorithms are expanding. The dataset keeps getting larger and more valuable. Frontier AI companies themselves are beginning to recognize how important proprietary data assets like Tempus’ could become.

The price action has been frustrating. The thesis has kept improving.

At some point the rotation changes. Long-duration AI platforms regain attention. Healthcare AI gets reassessed. Investors begin to understand that Tempus belongs in a different strategic category from SaaS or legacy diagnostic names.

$TEM is building proprietary healthcare intelligence infrastructure for the AI era, and I think the market will eventually pay much more attention to that reality.

I have no idea when the rotation will hit, but I'm positioned and adding to my position until it does.

J Keynes@JKeynesAlpha

$TEM Tempus AI again expands AI collaboration with $BMY and has 80% of big pharma locked up with AI/data contracts and the market is like 💤💤💤💤🥱🥱🥱🥱 “I only care about semis”

English

1. $NBIS - 3Y revenue CAGR: 206%

Nebius Group N.V. is an Amsterdam-based tech company building full-stack infrastructure, cloud platforms, and large-scale GPU clusters for AI.

English

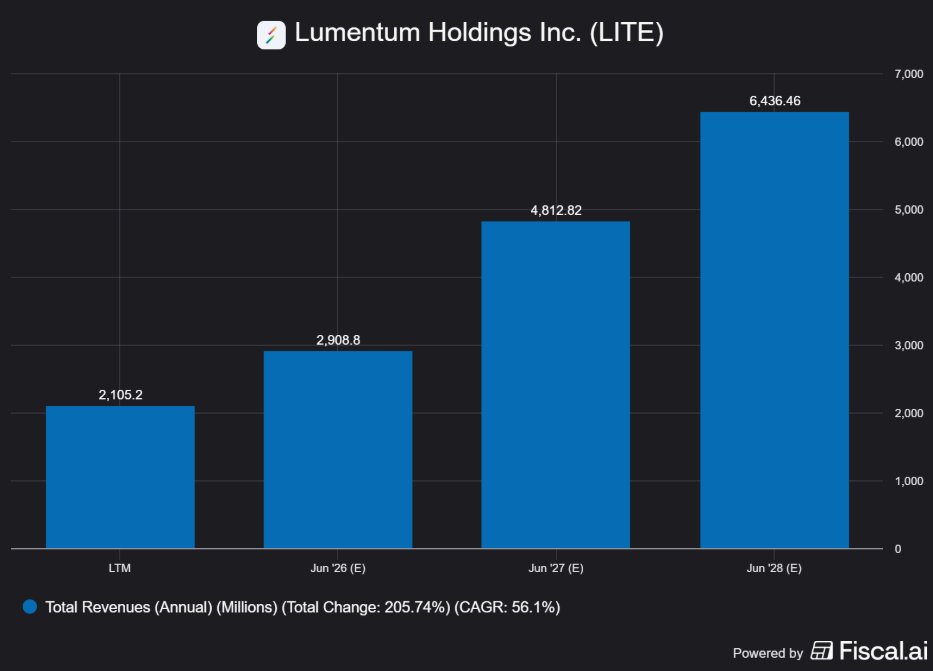

Here are 10 companies with an average revenue growth of +50% in the next 3 years.

10. $LITE - 3Y revenue CAGR: 56.1%

Lumentum is a San Jose-based manufacturer of advanced optical and photonic products powering AI data centers, telecom, and commercial lasers.

English

1 year ago, SNDK was under $30, its up 5200% at $1560.

SNDK lost $2 billion every quarter, but GOOG AMZN needs their chips.

Right now, there's 7 companies under $30 exactly like SNDK:

1. $POET — $11.19 🎯 PT: $80

Optical interconnects that replace copper inside AI data centers.

Customers: Lite-On, $SMTC, NTT now targeting Marvell's ecosystem

Catalyst: Malaysia plant ramping 30,000+ Infinity optical engines in 2026

2. $NOK — $12.82 🎯 PT: $15

5G + optical networking backbone for every hyperscaler buildout.

Customers: Amazon, Google, Microsoft €1B in orders from them in Q1 alone

Catalyst: Raised optical network growth outlook to 18–20% on exploding AI demand

3. $EOSE — $8.70 🎯 PT: $30

American-made zinc batteries powering the grid AI data centers drain.

Customers: Utilities, IPPs, CAISO & ERCOT grid operators

Catalyst: $303.5M DOE loan finalized — funds 8 GWh annual production by 2027

4. $DGXX — $6.45 🎯 PT: $30

Building GPU data centers to rent compute directly to AI companies.

Customers: Cerebras Systems (AI chip maker)

Catalyst: $1.1B, 10-year colocation deal signed $2.5B potential with expansion

5. $LWLG — $16.41 PT: $120

Electro-optic polymers that make AI fiber speeds physically possible.

Customers: Tower Semiconductor, GlobalFoundries, 4 Fortune 500 companies in Stage 3

Catalyst: PDK 1.1 ready for high-volume foundry transfer tape-outs begin H2 2026

6. FLNC — $24.50 🎯 PT: $28

Battery storage that keeps AI data centers powered without grid failure.

Customers: Two major hyperscalers (MSAs just signed), utilities globally

Catalyst: Record $5.6B backlog + first hyperscaler order converting Q3 2026

7. $PLAB — $49.50 🎯 PT: $55

Photomasks for every advanced AI chip no mask, no chip, period.

Customers: $TSM, $INTC, Samsung, UMC the entire chip foundry food chain

Catalyst: Record high-end IC revenue driven by AI chip packaging and advanced logic nodes

Remember, these have 1000%–2000% potential like $SNDK. My favorite is POET, but I like PLAB too since it makes photomasks which is needed in every chip on earth.

♻️ RESHARE this post and share 1 comment, and I'll DM you my BUY ZONES for each of these.

English

AI data center comparison:

$CRWV CoreWeave — $57B market cap. 3.5 GW contracted. Roughly $16 per watt.

$NBIS Nebius — $44B market cap. 2+ GW contracted, targeting 3 GW. Roughly $15 per watt.

$IREN IREN — $19B market cap. 5 GW secured power. Roughly $3.80 per watt.

$MARA Mara — $4.87B market cap. 2.2 GW pipeline. Roughly $2.22 per watt.

$HUT Hut 8 — $11B market cap. 597 MW contracted, 8.4 GW pipeline. $1.18 per watt contracted.

$KEEL Soluna — $2.4B market cap. 2.2 GW pipeline. Roughly $1.09 per watt.

$VIVO VivoPower — $50M market cap. 358 MW operational and 18-month pipeline. Roughly $0.14 per watt.

English

Last week, we opened a position in one of the "picks and shovels" names powering AI infrastructure.

A company building the electrical backbone for data centers - switchgear, transformers, distribution systems, and grid infrastructure.

Full deep dive with our position- link attached below

English

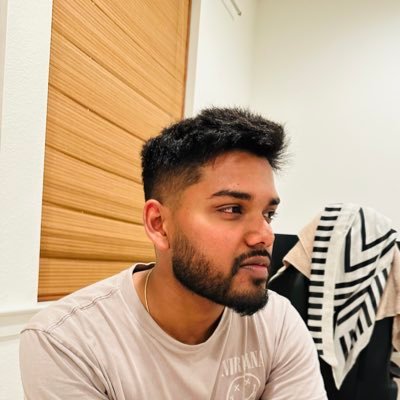

8/As someone who has been writing extensively about the Gene Editing and CRISPR field It’s hard to underestimate the magnitude and the significance of Prof @davidrliu’s work. From inventing Base Editing to Prime Editing, from discovering multiple delivery platforms aimed to carry genetic payloads to Prof Liu’s recent discovery of a new tRNA platform called PERT 🧵👇 - Prime Editing-mediated Readthrough of premature termination codons, the scale of Prof Liu’s innovation is overwhelming! Yet the big challenge remains how to make this unprecedented innovation and life-saving platforms available to millions of patients who are waiting to be cured!

Yair Einhorn@yaireinhorn

IMO the most important scientific event this week was the publication of @davidrliu’s new Nature article 🧵👇in which he presented a new and promising Gene Editing modality named PERT - Prime Editing-mediated Readthrough of premature termination codons. This new modality - which uses Prime Editing to converted a regular tRNA gene into a highly optimized suppressor tRNA thus enabling permanent readthrough of premature stop codons, could potentially provide a one-time curative treatment for countless nonsense mutations which are responsible for almost one-third of all human genetic diseases! Here is an excellent lecture by Prof. David Liu - one of the most important scientists and innovators of our lifetime and the person who invented both Base editing and Prime editing - the 2 top leading modalities of Gene Editing, in which he throughly explains this huge scientific breakthrough. $PRME $BEAM

English

1/The @washingtonpost “Post Next 50” is an annual list of people who are actively reshaping America’s future and who are at the spearhead of America’s innovation and entrepreneurship. Prof. @davidrliu - the inventor of the most advanced Gene Editing platforms Base Editing $BEAM and Prime Editing $PRME, was named as one of these exceptional leaders. Prof Liu was chosen to be displayed at the cover of the 2026 WAPO list due to an unprecedented medical breakthrough that was achieved last year when a personalised and custom-made genetic Base Editing treatment was able to fix the DNA thus curing a new born baby named KJ Muldoon which suffered from an incurable genetic disease. Another inspiring reason for this recognition is Prof. Liu’s new initiative to build a non-profit center for genetic surgery at the Broad institute! Today there are about 8,000 to 10,000 different genetic diseases which affect more than 400 million patients worldwide. Many - if not all of these rare genetic conditions, are “too rare” and lack the commercial potential which could lead BioTech and Pharma companies to invest in developing a cure for these patients. I couldn’t agree more with Prof Liu that this is a global health crisis and that the only thing which prevents these state of the art platforms from curing patients is the lack of sufficient funding. In order to overcome this issue and to use to these novel state of the art platforms to cure patients - a government funding and support is needed in order to confront this global health crisis! 🧵👇

Yair Einhorn@yaireinhorn

Here is a much needed dose of optimism by @davidrliu about the huge potential of Gene Editing & how it is changing our lives. The remarkable advancement in the Gene editing field & specifically in Base Editing - $BEAM & Prime Editing $PRME is providing hope to so many patients!

English

Neden Amerikan borsaları önümüzdeki 2 yıl yükselmeye devam etmelidir (ve bunun arkasındaki mantık)

ABD için borsaların sağlam kalması yalnızca piyasa konforu sağlamıyor — bu, ülkelerin geleceğini belirleyecek AI altyapı yarışının finansman mekanizmasının kilit parçası. Eğer piyasalar bu yatırım dönemi boyunca çökerse, ABD hem sermaye hem de stratejik avantaj kaybeder. Aşağıda adım adım nedenleri ve sonuçları anlatıyorum.

1) Büyük tez: AI dönüşümü bir ‘lüks’ değil, stratejik zorunluluk

AI sadece şirketleri daha karlı yapma projesi değil; altyapı, çip üretimi, veri merkezi kapasitesi, elektrik/enerji yatırımları ve devlet destekli büyük araştırma programları gerektiren bir ulusal seferberlik. Bu yatırımlar tamamlanmadan ABD’nin teknoloji liderliğini sürdürmesi zor — ve bunun finansmanı büyük ölçüde sermaye piyasalarına bağlı.

2) Küresel yatırımcı ilgisi artıyor — dış talep hala güçlü

Yurtdışından gelen sermaye, ABD hisse senetlerine olan talebi canlı tutuyor; son dönemde yabancı alımların gücüne dair veriler ve piyasa yorumları bunu doğruluyor. Bu, sadece ABD içindeki alıcılarla sınırlı olmayan, küresel bir sermaye akışı demek. Amerika tüm dünyadan olan yatırımcıları kullanarak kendi AI dönüşümünü finanse ediyor.

3) Perakende yatırımcı erişimi gerçekten eskisinden çok daha kolay — bu geniş bir sermaye tabanı demek

Fraksiyonel paylar, komisyonsuz platformlar, mobil uygulamalar ve düşük bariyerli arayüzler sayesinde bireylerin küçük miktar parayla bile dev şirketlere girmesi mümkün oldu. Araştırmalar ve şirket raporları, bu yeni erişimin yatırımcı tabanını genişlettiğini gösteriyor; ayrıca büyük platformların büyüme rakamları bunun kanıtı. Bu, sermaye toplamanın daha demokratik hale geldiği; şirketlerin halka veya ortak satışlarla fonlama yaparken daha geniş bir alıcı havuzuna güvenebileceği anlamına geliyor. Altda olan qrafikden de görüceğiniz üzere 2019-2020 arasında bu alanda nasıl bir devasa sıçrama var kendiniz görün. Bilinçli olarak perakende yatırımcıların sayısı borsada artırılarak daha kolay para bulmanın önü açılıyor.

4) Finansman mekanizması — neden piyasaların ‘çökmesi’ yatırımları durdurur

Şirketler büyük sermaye gerektiren AI projelerini finanse ederken sıklıkla:

-- Halka arzlar, ek hisse satışları veya kurumsal tahvil ihracı yoluyla sermaye toplar.

-- Bu araçlar istikrarlı bir talep ve ‘sıcak’ piyasa koşulları gerektirir.

Eğer piyasa sert düşüş yaşarsa:

-- Halka arzlar ertelenir veya fiyatlandırma çok maliyetli olur,

-- İkincil arzlar başarıya ulaşamaz,

-- Şirketler ihtiyacı olan sermayeyi zamanında bulamaz.

Sonuç: Büyük AI tesisleri, çip fabrikaları, veri merkezleri ve enerji bağlantıları ya gecikir ya da küçültülür — ve bu da teknoloji liderliğini tehlikeye atar.

5) Devlet rolü ve doğrudan destek — ABD bunu üstleniyor

ABD federal yönetimi, AI liderliğini bir ulusal hedef olarak gördüğünü açıkça ifade ediyor; son yıllarda federal düzeyde AI için politika, platformlar ve kaynak kanalize edilmeye başlandı. Devletin aktif desteği, özel sektör yatırımlarını tamamlayıcı nitelikte ve riskleri azaltıcı. Bu da hükümetin, yatırımlar tamamlanana dek piyasaların kırılgan olmasına izin verme isteğinin düşük olduğunu gösteriyor

6) ABD bu süreçte petrolü baskılamaya ve FED faiz indirimlerine devam etmek zorunda.

Çünkü AI yatırımları yüksek enerji ve ucuz sermaye gerektirir. Petrol yükselirse maliyet ve enflasyon artar, faizler yüksek kalırsa finansman durur. Bu da AI yatırımlarını yarım bırakır. ABD, AI yarışı bitene kadar ne enerji maliyetlerinin kontrolden çıkmasına ne de finansal koşulların sertleşmesine izin verebilir.

7) Jeopolitik arka plan: Çin ile rekabet

AI halihazırda ekonomik ve stratejik bir rekabet alanı. ABD için AI’da geri kalmak sadece birkaç şirketin kaybı değil; teknolojik üstünlüğün kaybı, tedarik zinciri ve ulusal güvenlik risklerini beraberinde getirir. Dolayısıyla hem kamu hem özel sektör, yatırım zincirini devam ettirmek için güçlü motivasyona sahip.

8) Uygulamalı örnek akış (adım adım)

-- Yatırımcı talebi + likidite → şirketler fazla düşük maliyetle sermaye bulur.

-- Sermaye → çip yatırımları, veri merkezleri, yeni fabrikalar, eğitim & araştırma programları.

-- Bu altyapı tamamlandığında: verimlilik artar, şirket karları büyür, ihracat kapasitesi yükselir.

-- Kısacası döngü tamamlanana kadar piyasa bozulmalarına izin verilmemesi gerektiği mantığı buradan gelir.

9) Karşı argümanlar ve riskler (dürüstçe değerlendirme)

Evet, teori güçlü ama bazı riskler var:

-- Aşırı değerleme/balon riski: AI beklentileri bazı varlıkları yüksek fiyatlandırdıysa, rasyonel düzeltmeler piyasalarda sert düşüşe sebep olabilir ama bence bu düşüşler uzun sürmez. (Bunu hafife almamak lazım.)

-- Enerji ve altyapı darboğazları: AI altyapısı enerji-intensif; şebeke kapasitesi sorunları veya maliyet artışları projeleri yavaşlatabilir.

-- Jeopolitik sürprizler: Ticaret kısıtları, teknoloji ihracat yasakları veya beklenmedik yaptırımlar sermaye akışını ve tedarik zincirini bozabilir.

-- Makroekonomik riskler: Tüketici talebinin çökmesi gibi faktörler yatırım maliyetini yükseltir.

Bu riskler gerçek; ancak ABD hem kamu politikası hem de küresel sermaye çekimi sayesinde riskleri yumuşatma kabiliyetine sahip.

10) Sonuç — neden “borsalar yükselmeye devam etmeli” argümanı

-- AI dönüşümünün başarısı büyük sermaye ihtiyaçları gerektiriyor.

-- Hem yabancı sermaye hem perakende yatırımcılar bu sermayeyi sağlayacak genişlikte.

-- Federal politika ve doğrudan yatırımlar (araştırma programları, altyapı destekleri) süreci tamamlamaya çalışıyor.

-- Eğer piyasalar bu aşamada çöküp finansman kanalları kapanırsa, ABD hem ekonomik hem de stratejik olarak geri kalma riski alır — bu yüzden politika yapıcılar/piyasa aktörleri sürecin devam etmesi için elverişli koşulları korumaya çalışır

Yani -- Borsaların güçlü kalması, AI yatırımlarının tamamlanması için stratejik bir zorunluluktur. Amerika bu kadar borç ve AI yatırım döngüsü ile ülkenin resesyona girmesine ya da piyasaların çökmesine izin veremez.

Yatırım tavsiyesi değildir. Bu sadece benim önümüzdeki yıllar için tezim. Borsalar arada düzeltme yapa bilir ama yönün yukarı olduğunu düşünüyorum.

#AI #Investing #USMarkets #CapitalFlows #TechRace #Macro #YatırımMantığı

Türkçe

A custom ETF I'd build today if I were to start from scratch:

Highly diversified for those who can't stomach daily 10% swings. But with a tilt to AI for growth to confidently outperform $SPY / $QQQ.

Equal-weighted ETF:

Hyperscalers + neocloud:

1. $GOOGL - Q1 capex 2x'd w/ Google Cloud backlog going haywire to $461B. Durable 20%+ growth locked in to 2028.

2. $META - on track for record ad rev (already +33% YoY) while scaling Blackwell GPUs for Llama 4. Really strong user engagement metrics despite capex ramp.

3. $NBIS - hyperscaler partnerships and $NVDA-backed capacity ramp. Eigen AI acquisition = fatter Nebius margins.

Memory + semis:

4. SK hynix - HBM3E/HBM4 fully sold out through 2027+ due to Nvidia/AMD GPU demand. Clear leader.

5. $MU - US HBM exposure also w/ supply locked + capacity expansions.

6. $TSM - manufacture basically every advanced AI chip w/ CoWoS capacity ramping now. CoPoS set for ~June with ~2028 ramp ups. CHIPS Act fabs on schedule.

7. $INTC – CHIPS Act + Trump administration backing. 18A process hit commercial yields. Partnering w/

$TSLA + SpaceX to make chips for Terafab. Onshoring + process catch-up makes Intel a multi-yr recovery story.

8. $AMD - winning Meta/Google cluster deals. Agentic AI driving CPU demand fcst to $120B mkt by 2030. Only credible alternative to $NVDA in both training + edge/robotics compute.

Energy:

9. $BE - fuel cell backup/complement to nuke baseload delivering 24/7 reliable AI power. New msa w/ $ORCL.

10. $GEV – nuclear services/turbines = direct beneficiaries of hyperscalers wanting clean energy. Equipment backbone of nuclear renaissance.

Defence + space:

11. $RKLB - q1 rev $123M (+32% YoY) w/ $1.1B backlog. Neutron added to $5.6B NSSL program. 20+ launches targeted for 2026. Small-sat launch + Neutron = commercial scale pre-SpaceX ipo.

12. $ASTS - d2c satellite broadband launching this year. New carrier partnerships. Global connectivity via space is a multi year infrastructure buildout.

Software (names irreplaceable by AI imo):

13. $NOW - huge nrr metrics. Strong crpo growth of 21% + early AI workflow wins across every business line. Every company uses their platform to automate workflows, w/ 20%+ growth locked in till 2028 & upside from platform pull-thru.

14. $APP - purest AI powered adtech compounder - their ML platform delivers better ROAS for mobile advertisers. AI advertising is the future.

Health:

15. $HIMS - Q4 subscribers >2.5M. Strong non-GLP-1 momentum (weight loss headwinds already priced in). Overseas expansion too. AI personalisation = sticky subscription model with 2030 targets of $6.5B+ rev.

16. $LLY - GLP1 leader. Huge multi year runway. Recent news of new indication expansions.

Fintech + banking:

17. $SOFI - Q1 members reached 14.7M (+35% YoY) and products hit 22.2M (+39%). Record $12.2B loan originations + deposit growth while maintaining guidance. They do everything; lending, banking, investing, and tech platform all on one app.

18. $JPM - i see them as a quasi-tech company now - led a $3.8B datacenter bond (Nvidia backed) that drew $14B in orders. Continues financing hyperscaler infra while expanding its own AI payments/fraud platforms.

Physical AI / automation:

19: $CAT - huge AI build-out tailwinds in their power/energy + construction segments. Alliance with Microsoft/Nvidia for 2 GW of dedicated power infra in West Virginia.

Grid modernization:

20. $NEE - closed $2B+ in new AI data-center renewable + storage deals. Largest U.S. renewable generator + utility w/ nuclear exposure = visible cashflow growth from the fastest/cheapest power solutions hyperscalers need.

English

(Stocks 21-27 are in the last post; it was getting too long for the thread.)

But if you liked this, please consider signing up for Grow or Die, where I post growth stock insights every week with @C_Reilly5. We're growing fast.

Join us: growordieinvesting.substack.com/p/join-us

English

27 stocks...

Here are 27 stocks set to benefit from what I'm calling "Elon's Endgame"

I'll provide tickers and quick descriptions of each stock below in this megathread 🧵

But first... here's my thesis, and why you as an investor might want to start positioning yourself. ⬇️

English

AI isn't a single stock. It's an entire supply chain from the machines that make the chips to the robots they power.

If you found this useful, follow me @JasonL_Capital for more breakdowns on the stocks and strategies building long-term wealth.

English

The AI supply chain is massive. From the machines that make the chips to the software that runs on top of them.

Here are 15 stocks that make up the entire AI stack:

1. $ASML - ASML Holdings (Chip Equipment)

The only company on earth that makes EUV lithography machines. Every advanced chip from NVIDIA, Apple, AMD, and Qualcomm requires ASML's equipment to exist. Q1 revenue hit 8.8B euros with a backlog of 38.8B euros - roughly a full year of revenue already locked in. Just raised 2026 guidance to 36-40B euros. High-NA EUV is now entering high-volume manufacturing. No ASML, no AI chips.

English

Costco sells CASKETS

Starting around $1,300 with shipping included. Funeral homes are legally required by the FTC to accept caskets purchased from outside sellers. No extra fees. No penalties.

Costco said we will save you money cradle to grave and they MEANT it.😩🤣

English

Michael Burry went long $ADBE.

43 things every Adobe investor should know before you write it off.

The basics. The numbers. The CEO Leaving. Michael Burry. The moat. The hidden assets. The risks.

All of it. Bookmark this.

THE BASICS

1. Founded in December 1982 by John Warnock and Charles Geschke in Warnock's garage. Both left Xerox PARC after Xerox refused to commercialize their graphics language. Named the company after a creek behind their house.

2. Steve Jobs tried to buy Adobe for $5 million in 1982. They refused. He bought 19% instead at five times the valuation plus a five-year PostScript license fee, paid in advance. Adobe became profitable in year one. First company in Silicon Valley history to do that.

3. Adobe invented PostScript in 1983. The first universal language for digital printing. Then invented PDF in 1993. Code name: "The Camelot Project." Two global standards, same company, still dominant 40 and 30 years later.

THE NUMBERS

4. Revenue: $23.77 billion in FY2025. Up 11%. Q1 2026: $6.40 billion. Up 12%. No down revenue years in the last decade.

5. North of 96% subscription revenue. Annual recurring revenue exiting Q1 2026: $26.06 billion. Growing 11%.

6. Free cash flow: $9.85 billion in FY2025. Up 25%. FCF margin of 41%. Among the highest in all of software. This is a toll booth business.

7. Non-GAAP EPS: $20.94 in FY2025. Up from roughly $5 in 2017. A 4x increase in eight years. Revenue tripled. EPS quadrupled.

8. IPO in August 1986. $10,000 invested at IPO is worth roughly $6.8 million today. At the 2021 high of $699 it was nearly $20 million. Current price: ~$246. Down 65% from that high.

THE STRUCTURE

9. Digital Media: ~$17.6 billion in annual revenue. The crown jewel. Creative Cloud and Document Cloud. About 73% of total revenue.

10. Creative Cloud is the professional creative workflow standard for 40 years. Every design school teaches Adobe. Every major agency, studio, and publisher runs on it. This is not brand loyalty. This is infrastructure.

11. Document Cloud: growing mid-teens. Adobe didn't just invent PDF. They still own the tooling around it. Acrobat, e-signatures, AI document assistants. The PDF standard is open. The monetization layer is not.

12. Digital Experience: ~$5.5 billion. 99% of Fortune 100 companies are Adobe customers. More than 150 pay $10 million or more annually. That cohort grew 25% year-over-year.

THE TRANSFORMATION

13. In 2012, Shantanu Narayen bet the company. Killed the perpetual license model. Moved everything to subscriptions. The stock crashed 17% the week of the announcement.

14. Revenue at the time: ~$4.4 billion. Revenue today: $24 billion. Stock went from $28 on announcement day to $699 over the next decade. The most successful business model transformation in software history.

15. Firefly is Adobe's generative AI model. Trained exclusively on licensed content. IP indemnification included. Every Fortune 500 legal team's nightmare is AI-generated content violating copyright. Firefly solves this.

16. 80 million+ creative freemium monthly active users. Growing 50% year-over-year. The funnel nobody models. Is it genius funnel building or paid seat cannibalization? Both sides have evidence.

17. Adobe has raised Creative Cloud prices multiple times over the past decade. Retention held above 97% every time. That is pricing power. The kind you only get when switching costs exceed the price increase by orders of magnitude.

THE CFO

18. Dan Durn became CFO in October 2021. Before that: CFO of Applied Materials, where he reduced the share count by roughly 30%. The stock 4x'd. Before that: Goldman Sachs M&A. Naval Academy. Columbia MBA. This is a capital allocator with a pattern.

19. Since arriving at Adobe, the pattern is identical. Shares have declined from nearly 490 million a decade ago to roughly 400 million today. Adobe retired 8.1 million shares in Q1 2026 alone. FY2025: $12 billion in buybacks. Largest repurchase year in company history.

20. Adobe spends roughly $2 billion annually on stock-based compensation. 8.5% of revenue. Not zero. But Durn buys back MORE than the dilution. Your ownership grows every quarter. Compare to ServiceNow at 16% SBC with shares GROWING 2% a year.

SHANTANU NARAYEN

21. Born in Hyderabad, India. Joined Adobe in 1998. Became CEO in 2007. Over 18 years at the helm. Market cap from $20 billion to over $200 billion at its peak. Revenue from $3 billion to $24 billion. He is the architect of everything modern Adobe.

22. Navigated the Figma acquisition honestly. Bid $20 billion. Regulators blocked it globally. Paid a $1 billion breakup fee and walked away. No ego. No hostage negotiation. $1 billion bought clarity, not Figma.

23. Key acquisitions: Macromedia in 2005 ($3.4 billion, brought Flash and the web), Omniture in 2009 ($1.8 billion, foundation of Digital Experience), plus a dozen more. Now pending: Semrush for ~$1.9 billion. Strategic M&A, not empire building.

24. On March 12, 2026, Adobe announced Narayen would step down as CEO. Stock dropped 9%. He remains as Chairman. Not a health emergency. A planned succession at the worst possible time for optics.

THE SUCCESSOR

25. The Board is vetting internal and external candidates. Internal frontrunners: David Wadhwani (President of Digital Media) and Dana Rao (General Counsel). No timeline disclosed.

26. If they pick a product person, they're worried about AI. If they pick an operator, they think the moat holds and execution is the game. Watch the choice. It tells you what the Board actually believes.

THE MOAT

27. Enterprise workflow entrenchment. I've done enterprise software sales for 15 years. Ripping out Adobe from a Fortune 500 content workflow takes years. It's not a tool swap. It's an infrastructure rebuild.

28. File format lock-in. .PSD, .AI, .INDD, and .PDF are industry standards. Agencies have 10+ years of templates and brand guidelines built on them. The migration cost isn't the license. It's the decade of work that lives in Adobe formats.

29. Training and muscle memory. Every design school teaches Adobe. 40 years of graduates. The shortcut keys are in muscle memory. Institutional inertia built over decades. Every graduating class deepens it.

30. Commercial AI safety. Firefly is trained on licensed content. Midjourney and DALL-E offer no IP indemnity. Adobe offers commercially safe AI at enterprise scale. The legal department is part of the moat.

31. The Canva and Figma fear is a category error. Canva wins prosumers who were never paying $70/month. Figma dominates UI/UX where Adobe's XD already failed. Neither takes share inside the enterprise. The market prices Adobe as if its core customer is a freelancer. It's not. It's AstraZeneca, JPMorgan, GM, and Costco.

HIDDEN ASSETS

32. PDF is the most under appreciated asset in software. Adobe created it in 1993. The format is free. But Acrobat, e-signatures, security, and AI document intelligence sit on top. Courts, banks, governments, hospitals. They don't switch document formats. This is a toll bridge.

33. Remaining performance obligations: $22.2 billion exiting Q1 2026. Growing 13% year-over-year. Contracted revenue that will hit the books. Ferrari gets credit for its order backlog. Adobe has the same thing in software form and nobody talks about it.

34. Adobe Stock and Behance. 250 million+ licensed assets. Adobe trains Firefly on its own library. The training data IS the competitive advantage. Every competitor training on scraped internet data has a legal liability Adobe doesn't.

35. $8 billion+ in cash. Net debt near zero. Even if growth went to zero, Adobe generates enough cash to buy back 10%+ of its market cap annually and still fund R&D.

MICHAEL BURRY

36. In early March 2026, reports surfaced that Burry took a long position in $ADBE. Unconfirmed because Scion deregistered in November 2025. No more 13F filings. The market moved on rumor alone. Stock jumped nearly 4%.

37. Burry tweeted: "Adobe $ADBE should buy Midjourney. And any other small creative software company with a creative founder." Then: "Adobe, you have the cash flow to protect your franchises." The man warning about the AI bubble is telling Adobe to buy MORE AI.

38. Connect the dots. Burry shorted Nvidia. Shorted Palantir. Called AI a bubble. Then reportedly went long the one company the AI narrative says is dead. AI hysteria mispriced a $24 billion revenue machine at 12x forward earnings. That's Burry's entire career in one trade.

THE RISKS (HONEST)

39. AI commoditization is real. Google offers pro-grade image generation for free. DaVinci Resolve is eating Premiere Pro in the indie tier. The question isn't whether AI disrupts creative tools. It's whether Adobe's enterprise moat is wide enough that it doesn't matter.

40. CEO succession during an existential narrative crisis. Narayen had 18 years of trust. The new CEO starts with zero. And Adobe still doesn't have a Figma competitor. The collaborative design gap is real.

41. Adobe paid $75 million to settle FTC charges about cancellation practices. The UK is separately investigating. Their 97%+ retention might partly reflect cancellation friction, not product love. If cancellation becomes frictionless, we find out the real number.

42. The generational risk nobody models. There's real grassroots backlash against Adobe's subscription model among younger creators. If the next generation grows up on Canva and free AI tools and never learns Photoshop, Adobe's moat doesn't break overnight. It erodes over a decade.

THE BOTTOM LINE

43. Three fear events priced simultaneously: AI Disruption + CEO Departure + SaaSpocalypse.

I'm not long $ADBE yet. But it really does look cheap.

English

@SJCapitalInvest @threadreaderapp Saving it for later reference (easier than if bookmark keeps growing)

English

$TEM 🔥Tempus AI, March 3 Morgan Stanley Recap: The Thesis Is Getting Stronger

The Morgan Stanley conference added a great deal to the Tempus story for investors trying to understand what this company is becoming. Eric Lefkofsky gave the clearest high-level framing yet: “Today we are absolutely an AI company.” What matters is how he defined that statement. He said Tempus does not approach the business by saying, “Oh, we’re gonna build models, and that’s our core business.” The company’s real objective is to “garner access to proprietary data,” use that data “whether it’s enhanced by our own models or other people’s models,” then “generate insights and deploy those insights back into the clinic.”

Lefkofsky also explained why the market still struggles to place Tempus. He said the company operates in “both of these worlds,” as an NGS business generating proprietary molecular data and as a “data AI company” that “takes that data and generates insights, licenses the data, licenses the models.” He added that diagnostic investors often do not get the data and AI side, while AI investors are uneasy with diagnostics. That split matters because it helps explain why Tempus can still be misunderstood even as the underlying asset base keeps getting stronger.

The data moat came through very clearly. From the beginning, Tempus did not want to sequence patients and stop there. Lefkofsky explained that the company went to providers and effectively said they would sequence patients, but they also needed the clinical data, because the real prize was learning whether insights generated from the sequencing actually worked in practice. He described the essential feedback loop in direct and practical terms: if Tempus found a mutation and recommended a drug, did the patient actually go on that drug, and how did the patient respond over time. That is the foundation of the dataset: rich molecular data connected to real treatment and response histories.

He then described what had to be built on top of that dataset to make it commercially useful. Once Tempus had amassed the data, handing raw files to customers was never going to be enough. The company had to build tools that let pharma interrogate the data, construct cohorts, refine those cohorts, and extract insight. Investors should pay attention to that because it means Tempus has spent years building software and workflow infrastructure around the data asset itself. That kind of work deepens the moat and raises switching costs.

He backed that up with one of the more revealing comments in the transcript. Tempus has “700 software engineers and product folks,” and it has made cloud investments “five or 10 times” larger than others in the space. Those are meaningful clues about what kind of company Tempus has been building all along. It has been investing like a technology platform that expects software, infrastructure, data operations, and AI deployment to sit at the heart of the business.

The Merck discussion was especially strong. Lefkofsky said, “you just don’t have people like AstraZeneca and GSK and BMS and Merck and others signing these $100 million plus deals unless the data is both incredibly useful and they can generate real insights from it.” That line deserves investor attention because it frames these pharma relationships as hard validation of utility. Big biopharma is paying for data and insight that can shape research, development strategy, trial design, and commercial decision-making.

He also described how those relationships deepen over time. “Merck’s a great example,” he said. These deals often begin relatively small, then expand as customers discover more use cases and eventually realize they want broad access to the data and tools. In Merck’s case, “it’s a five-year agreement, but four years are committed.” He compared the commercial structure to AWS, GCP, or Azure, where customers can buy a little or a lot and what changes is mainly access and pricing. That sounds like a relationship model with room for meaningful expansion as usage and dependence grow.

Another telling section came when Lefkofsky discussed competition. His comments suggest Tempus is playing in a lane where the customer decision is about strategic value rather than commodity pricing. The implication was that pharma customers come to Tempus when they want a dataset and insight layer capable of changing oncology programs in a meaningful way. That matters because strategic data assets with workflow relevance and trust embedded into them tend to command better economics and stronger customer stickiness over time.

The AI model section was the most exciting part of the transcript for me. Lefkofsky said large frontier model companies are increasingly coming to Tempus asking, “What data do you have?” He said their interest in this kind of data “on a scale of one to 10 was a one” and “it’s now like a five.” Then came the key line: “every one of these companies that we’re engaged with… is asking the exact same question. They want longitudinal patient histories at scale.” That is a very important signal. It suggests the next wave of healthcare AI is running directly into the scarcity of proprietary longitudinal real-world data.

He pushed the point even further with one of the best quotes in the session. These models, he said, are already extremely good at predicting the next likely word. With enough proprietary patient data, the opportunity is to “predict the next likely drug or the next likely therapy that would work for a patient.” That is the statement that should make investors pause. He is pointing toward a future in which model capability becomes clinically actionable in a much more direct way. The promise here is not abstraction. The promise is better therapeutic prediction and better individualized care.

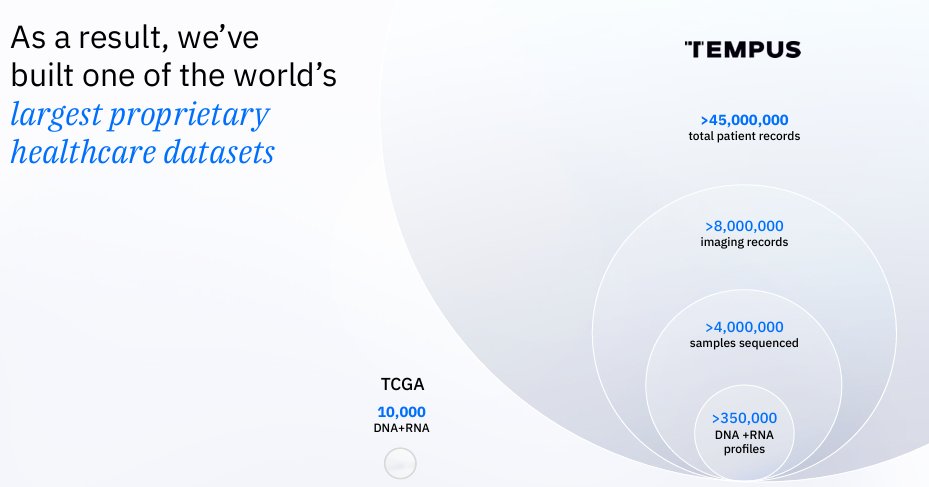

The moat discussion around the data was equally strong. Lefkofsky said the dataset is hard to replicate because you have to integrate with thousands of hospitals, get through legal and IT bottlenecks, gather multiple time points, collect structured and unstructured data, and connect all of that to Tempus’s own proprietary sequencing files. He said the dataset is “approaching 500 petabytes,” and he was blunt about the competitive history: efforts by others to bolt clinical and molecular datasets together have not gone well. Those remarks help explain why Tempus may occupy a uniquely strategic position just as model builders go looking for real-world healthcare data at scale.

Lefkofsky’s gave a lot of clarity on consumer AI and Tempus' differentiation. He said, “On the consumer side, I suspect those models will be delivered by the big consumer companies. Like, we have no aspiration to be that company.” He explicitly named “Apple and Google and OpenAI and Anthropic or whoever.” That is useful because it removes a category error some investors may still be making. Tempus is not trying to win a mass-market consumer health assistant battle. Lefkofsky is placing the company on the provider and pharma side, where the moat comes from trust, data custody, healthcare system integration, and existing relationships.

He sharpened that point further by explaining why the provider and pharma side belongs to companies like Tempus. In order to connect into the U.S. healthcare system, you have to be a covered entity. It is complicated. It involves deep logistical and regulatory complexity. He then made what may be one of the most important strategic comments in the whole transcript: “I just don’t see a world anywhere in the near term where the biggest pharmaceutical companies are uploading their critical clinical trial data to OpenAI or Google or whoever. I just think it’s too invaluable.” For investors, that is a very crisp articulation of where he thinks defensibility sits in healthcare AI.

Lefkofsky expanded on the new foundation models, saying that Tempus is building 2 models, one with AstraZeneca and Pathos AI and another pan-disease model on its own. He said the company has established 2 compute clusters, one with about “1,000 H200s” and another roughly that size using GB200s. The purpose is to generate “multimodal insights that you just can’t see unless you have enormous amounts of data.”

His example in non-small cell lung cancer was one of the most compelling illustrations of where this can go. Today, a patient may be identified as EGFR positive and placed on an EGFR inhibitor according to guideline therapy. Lefkofsky described the opportunity to go much deeper by distinguishing which patients may respond exceptionally well, which may fall into the middle, and which may progress quickly despite fitting the broad biomarker category. That opens the door to a much more refined response-prediction layer on top of standard biomarker-guided care.

He also laid out a useful framework for where long-term value may accrue. The data remains the scarce asset for training models that can change physician and patient behavior. Over time, the applications and algorithmic outputs built on top of that data can become even more powerful economically. This is a big reason the story is so interesting for investors. Tempus already has a data-generation engine, a data-licensing and insight business, and a pathway toward increasingly valuable AI-enabled applications.

The other major addition worth emphasizing is Lefkofsky’s comment on market psychology. He said the broad AI euphoria from 7 or 8 months earlier had dissipated considerably. Then he made the point that matters: if someone asked whether AI in healthcare is overhyped in the short term, his answer would be “no.” He went even further and said “the opportunity of AI in the near term is probably underappreciated.” He then added, “It’s way underappreciated in the long term, but it’s probably also now underappreciated in the near term.” That is a very interesting shift in tone. He is saying the market mood has cooled just as the operating proof points are getting closer.

The line that gives that argument real weight is his prediction that “in 2026, you will start to see very tangible evidence that AI is going to impact healthcare at incredible scale,” both from companies like Tempus on the provider and pharma side and from OpenAI, Anthropic, Google, Apple, and others on the consumer side. He is clearly telling investors that the visible evidence should begin to emerge this year. Then he connects that to economics by noting that Tempus has projected 25% growth for the next 3 years, while saying the “data long-term prediction and the AI long prediction is much higher than 25%.” Near-term evidence, long-duration upside, and an increasingly valuable data/AI segment is a powerful setup if execution follows.

My read is that this transcript did more than reinforce the Tempus thesis. It sharpened it. What came through here is a company that may be sitting on one of the most strategically valuable proprietary data assets in public-market healthcare at exactly the moment frontier model development is running into the need for proprietary longitudinal patient histories at scale. The Merck expansion matters because it shows large pharma wants deeper access once it understands the utility. The frontier-model angle matters because Lefkofsky is saying the world’s largest model builders are increasingly coming to companies like Tempus asking what data they have, and that every one of the major players they are engaged with wants longitudinal patient histories at scale. That is a big statement. It suggests Tempus may control part of the training substrate serious healthcare AI increasingly needs. And the line about predicting “the next likely drug” matters most of all because it points toward a future where Tempus is helping drive actual therapeutic decision-making in medicine.

What excites me is that Lefkofsky also made clear they are not trying to become some broad consumer health AI app in the mold of OpenAI, Anthropic, Google, or Apple. He effectively said that lane belongs to the big consumer platforms. Tempus is going after the part of healthcare AI where the real defensibility lives: provider workflows, pharma relationships, data rights, covered-entity trust, and infrastructure that took years to build. If that vision keeps executing, Tempus has a path to becoming far more than a diagnostics company with an AI story attached. It can become a core intelligence layer for precision medicine and biopharma, with the business mix moving toward higher-value data, models, and algorithmic applications. To me, that means the market may still be valuing Tempus below the scale of the platform it is actually becoming.

English