Randy Adams retweetledi

The leadership rotated, but the trend did not. The super cycle powers ahead.

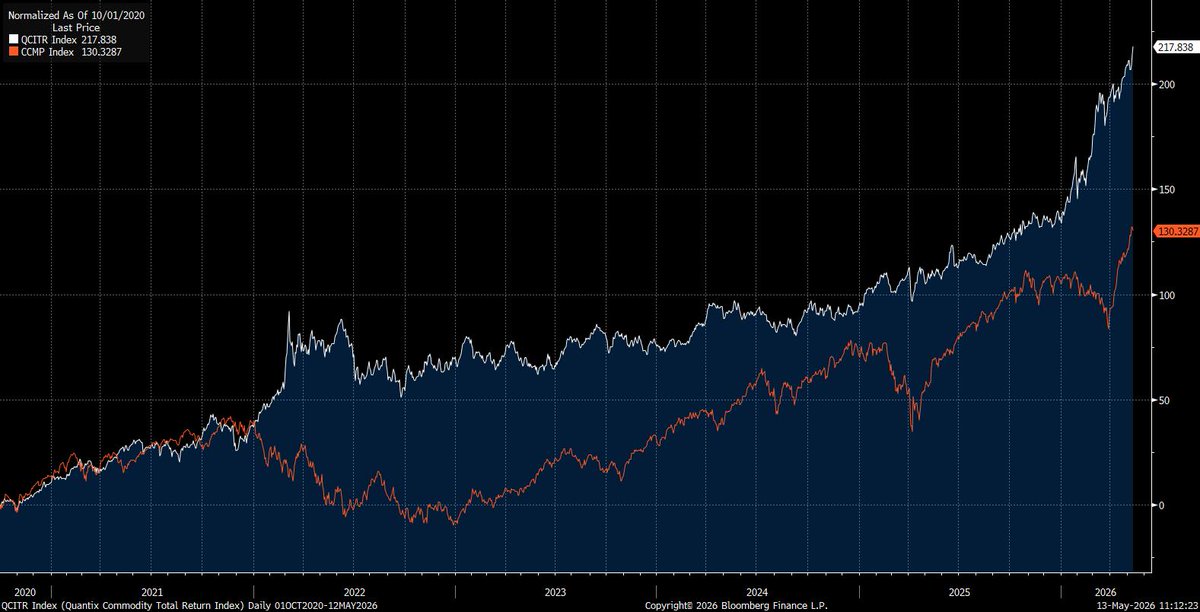

The Quantix Commodity Index (QCI, the modern GSCI) Total Return is up 217% since October 2020, when we called the super cycle. The names rotated — gold, silver, copper, oil, live cattle, coffee, cocoa, aluminium. But not the trend. Nasdaq returned 130%. The S&P 500, 85%.

Commodities were the top asset class. Nobody allocated. Capital piled into the Mag 7 — $770 billion of 2026 capex, nearly half of it commodities. Amazon alone consumes more than 3 million BOE/d of primary energy, more than most OPEC countries. The Mag 7 is the largest unhedged molecule short ever underwritten by an equity market...

…at the exact moment supply has never been more constrained. Hormuz is shut-in. China has weaponized the periodic table. Copper mines remain shuttered. Ukrainian drones push deeper into Russia, taking commodity supply with them. A multi-polar world demands thicker supply chains. Copper and the "atom" complex print fresh records this week. Every signal that should drive allocators into the "molecule" complex is flashing green simultaneously — for the first time since the 1970s.

And yet oil struggles to hold $105 — even as every signal points to a disruption that deepens and one we believe will outlast any "deal.” The energy sector trades 8% below its pre-Hormuz level and sits at 4.0% of the S&P 500 market cap. At $105 oil, its 2026 FCF yield is 13%. The S&P 500 is at 2.6% — the lowest since the GFC, 1,000bp below energy. The hyperscalers generate close to zero. Something has to give.

This paradox explains why oil struggles to trade higher. Capital is not rotating. The marginal dollar of investable savings still flows into the AI buildout, not the physical infrastructure that feeds it. Until that reverses, Brent faces headwinds. The ceiling on oil is not Washington. It is Exxon's cost of capital — woefully mispriced. Underbidding the equities is the same as underbidding the back end of the curve. The back end is suppressing the entire curve and spot prices.

1/10

English