Sabitlenmiş Tweet

(1/10) Excited to share a new blog post on the wave of trade in programs in China and what they tell us about Beijing's efforts to boost consumption.

csis.org/blogs/trustee-…

Long thread for those interested!

English

Ryan Featherston

1.2K posts

@Ryanfeath

Associate Fellow at @CSISCBE Thoughts are my own

🚨 The CSIS Trustee Chair is offering research internship opportunities for Summer 2026! This is a fantastic opportunity to learn more about China's economic trajectory, industrial policy, and U.S.-China relations. We are #hiring part-time paid Research Interns to support our program's analysis. To apply, visit the link here: careers.csis.org/opportunities/… How to Apply: Submit your resume, cover letter, writing sample, academic transcript, and a list of 3 references in one PDF. Applications will be reviewed on a rolling basis.

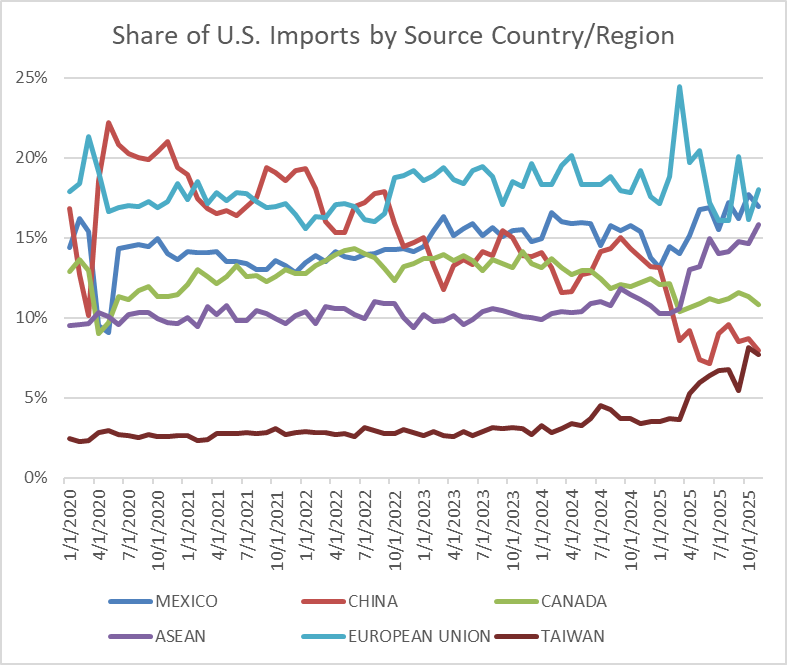

Taiwan's massive exports to the US are actually a sign that the AI boom/ bubble is making Taiwan's already unbalanced economy even more unbalanced ...

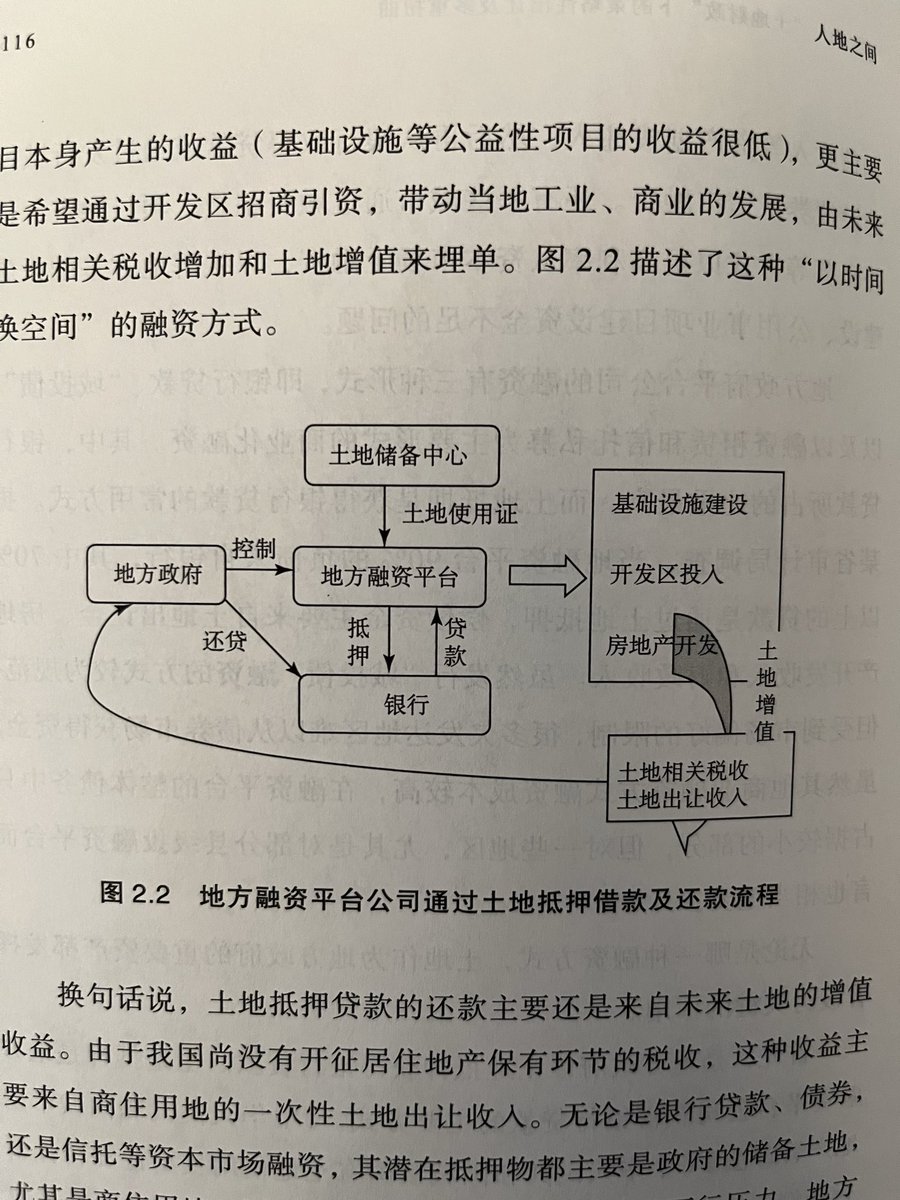

The book John is referring to is "How China Works," which I've recommended many times on my account, and truly the only must read book on the Chinese economy, no exaggeration. It's available on Kindle for $81

I don't know if Chinese manufacturers will ever make money but I came away not wanting to invest in any manufacturing business in the rest of the world. 7/x