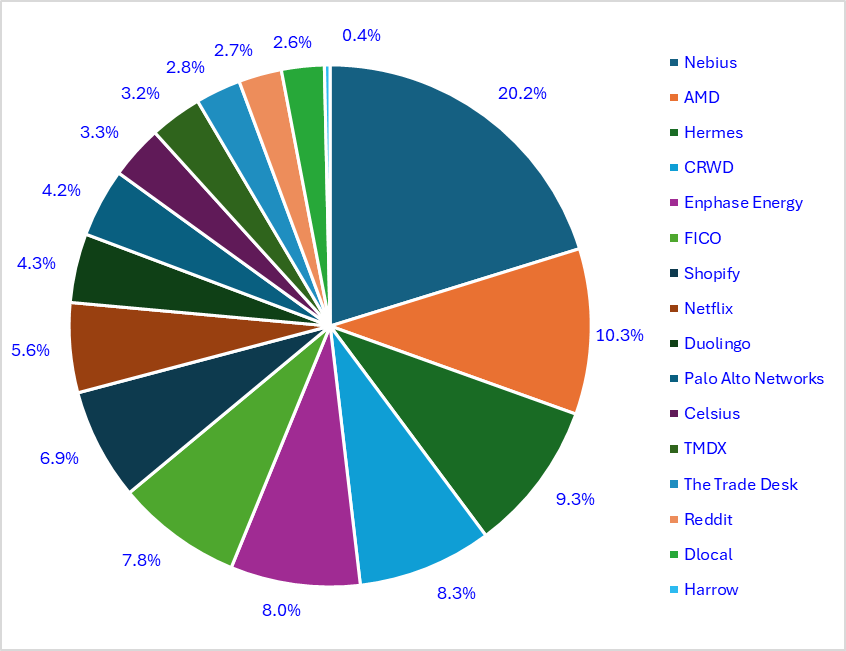

Five Points Capital@fivepointscap

$RDDT is still down 32% YTD despite just minting their 7th consecutive quarter of 60%+ revenue growth.

The company can drive significant ARPU growth through increased ad loads, and AI driven improvements in ad targeting and conversion rates.

Operating margin is now 27.6% in Q1, up from 1% the previous year and will continue expanding into the 40-50% range.

Net dilution over the trailing twelve months is now just 0.62%

The business is extremely capital light, with just $1M (yes, million) of capex in Q1.

The forward P/E multiple is 29.9x and that’s based on a sandbagged EPS figure. True forward P/E is probably around 25x, for again, 7 straight quarters of 60% revenue growth, huge margin expansion, and extremely low capital intensity.

Not to mention, a durable moat that has been tested several times over the past twenty years. $RDDT may be new to the public market but reddit is NOT a new platform. They’ve been building their moat for over two decades and it’s extremely strong.

Add in S&P 500 inclusion which is only a matter of time, and $RDDT is set to explode higher.