Darius

306 posts

@aleabitoreddit My parents in China have been seriously talking about buying a robot to be their caregiver in a few years time when they fully retire, because robots “won’t steal from us or beat us”.

English

I told you making the robots look hot might be a bottleneck:

Today, UBTech has now announced its first full-size hyper realistic humanoid robot girlfriend.

For adults only to purchase for only ~$145,717.90.

-"The U1 series emphasizes attractive appearance and is only available for adults to purchase."

- "It Can Imitate Most Human Movements and Expressions, and Also Has Long-Term Memory"

- "U1’s surface uses bionic materials and a gel structure to simulate skin texture, elasticity, and a warm touch."

UBTECH founder, chairman, and CEO Zhou Jian said on stage that just before going up, he learned that orders had exceeded 11,000 units.

Half an hour later, UBtech said the number had been updated to more than 13,361 units.

Demand for attractive robots is uncomfortably high.

Serenity@aleabitoreddit

I wonder if humanoids is going to spark a new bottleneck/industry for robot cosmetics. Like a skin bottleneck. Or Aespa KPOP robot makeover as a service. So if $TSLA Optimus makes tens of millions of humanoids: Who’s going to make them all look hot?

English

听说现在外边夜场站满了人,非常卷,

去夜场消费的大哥都破产了,经济不好每年一千多万大学生毕业,一大半找不到工作,无数人挤破头想进去,

能消费的变少了,想赚夜场钱的仙女越来越多,歪路上都人满为患了。

中文

@ShanghaoJin @Flyer_Zz 小地方考个985211理工科(top 3%),出来干个工程师20-30w,干到中年50w薪资,虽买不起房但也算能体面生活了,相比于出身已经算是跨越class了吧,如果这样假设,class流动率达3%不知道算不算好?

中文

中国是非常“门阀”的社会:平常人怎么努力往往也不可能跨越阶级

中国人又很可怜:自媒体、网络一直在喂鸡汤给他们不切实际的希望

很多从小出生在社会底层的人,在一次次努力,一次次跌落后,双向扭曲中形成自我防御机制。只能用对精英的敌意来“呐喊”

——他们往往不敢看天有点多高,因为看了就会刺痛

Crblandet@crblandet

昨晚的讨论让我对🎈这类人及其粉丝有了更深刻的认识🤭 也就是,别人分享的经验,自己浅尝几下不成,就觉得别人是在胡扯,然后天天跟人过不去、到处打假🌚 我也纳闷为什么有人会形成这种思维,Claude 的诊断一针见血🤭 案例学完了,以后就不再跟抱有这种心态的人对牛弹琴了。谢谢各位的耐心🤭

中文

最近互联网大厂的 PDF 瓜有点多

一名网友发文称,女友在字节工作期间,被他两次发现出轨不同的男同事,最终分手闹掰,后续双方就财产分割问题对簿公堂,然后男方一口气把经过写成 PDF,传播到字节同事圈里。。

Meguro-ku, Tokyo 🇯🇵 中文

Darius retweetledi

@KissrZhang @masala11693 @RickyYu6612 从21 22年开始到现在才几年,并且有多少人被套的死死的? 房价这玩意就是兴奋剂,成果是城市更新,gdp飞涨。后果就是断子绝孙,几十万亿的城投债分到每个人的头上

中文

巧了,那天浙江的哥们分享了他们市妇幼保健医院的出生率,一个县级市2017年以前每年有2000多个婴儿出生,今年上半年只有41个,这样看今年全年破百都是一个问题...断崖式出生率真不是开玩笑的

Tim@clmtim

@RickyYu6612 挺好的。。看样子中国的结婚率和出生率还是太高。。。

中文

捷克输给韩国了😭我压了2:2 1:2 就是没压2:1

没事昨晚小赚今晚继续跳预言家

加拿大波黑 2:1 1:1

美国巴拉圭3:0 3:1

给我冲!

小桃今天止盈了嘛@richpeach888

简单拿下第一场🤓

中文

十分制 sndk8.8。nvda 10 tsm10 海力士10 mu9.5。

Jay@the604og

@BabybusFL 闪迪吧。Nand对token的beta最高。automated ai researcher出来后的token explosion会很恐怖的。

日本語

Darius retweetledi

Spent some time with @NoodleBobz on why the skills that made you money in crypto can actively hurt you in stocks. Here are some of them.

1. Being retail is a genuine advantage. No benchmark, no LPs, no risk committee, no forced rebalancing. Institutions are often forced to trade around positions that you can simply hold. Crypto trains you to stay active, but here the freedom to hold is the edge.

2. Understand valuation floors. In crypto, the "fair value is 0" fear is real. In equities there are actual metrics that can provide some level of support. Earnings, book value, cash flows, takeout value. Knowing even the basics helps you hold through drawdowns.

3. Zoom out from short-term price action, and let winners ride. Crypto conditions you to react to every candle. In equities, mechanical flows like EOM rebalancing, options expiry, and index rebalancing can move stocks around without changing the thesis, so it's completely normal for a stock to chop for weeks before continuing higher. The same reflex shows up on the upside: perps condition you to take profit every 10%, but momentum can persist much longer, and a stock can grind higher for months after strong earnings. Most people end up more frustrated from selling too early than holding too long. That said, always reassess after big events like earnings, guidance changes, or management shifts. Don't confuse holding through short-term PA with ignoring new information.

4. There are far fewer PvP dynamics. Your edge doesn't come from being faster than another trader. You don't need to top-tick entries or bottom-tick exits. If the thesis is right, focus on capturing the bulk of the move rather than optimizing every trade.

5. Build deep conviction on a small number of ideas. The crypto habit of chasing every rotation can be costly in equities. The trap is constantly jumping sectors because something else is moving. Build a focused watchlist and understand the thesis well enough to hold through volatility. The biggest winners are often the positions you know best.

6. Pay attention to what's actually working. Market leadership often tells you more than macro commentary. Watch where capital is flowing and which types of stocks are being rewarded. If low-quality names and retail favorites are ripping, that's useful information about the environment you're operating in.

7. Understand what's driving your position. Know how much of your thesis is idiosyncratic versus tied to sector or market beta. When macro becomes hectic, stocks with strong company-specific drivers often hold up much better than you'd expect. Not everything is tied to BTC here.

That said, don't underrate what you bring. crypto runs the same cycles as equities, just compressed into months instead of years. You have already sat through more euphoria, capitulation, and recovery than most equity traders see in a decade. You have just been trained for it at higher speed.

English

我知道的尾插有kklbs和hhj,我自己用的是前者,软件和硬件都很友好。先说优点和使用场景:

1️⃣ App和硬件界面简单易操作

2️⃣ 适配iPhone 13-17全系列,支持Type-C和Lightning接口

3️⃣ 支持iOS 17.3-26.5系统

4️⃣ 可用于发朋友圈定位,解锁App地域限制(券商、U卡、银行等)和部分游戏地域限制

操作方法:

1️⃣ 下载kklbs软件后插入设备,点击地图右侧信号连接设备

2️⃣ 选择定位地址,点击地图下方绿色按钮锁定

3️⃣ 开启飞行模式—关闭定位—等待10秒左右—开启定位—关闭飞行模式,大功告成

4️⃣ 切回原定位需拔掉尾插,重复步骤3即可

修改地址后就可以尽情飞了,是不是很简单。我不卖尾插,想买的自己去闲鱼,100元以内,认准品牌就好。早弄早享受,行动起来别懒,提高执行力。

星球🪐🪐☄️☄️@Lee_points

想要解决内地用户无法进行金融(券商)交易的问题不是没有办法。 更多人想到的是通过修改定位来达到目的。安卓操作简单,root后设备可随意篡改(0富vida用的是此方法),但我们做的是金钱交易,安全性会大打折扣。 iPhone用户之前可通过爱思修改定位或越狱实现,但现在这些操作已不符合大部分人的需求。 其实还有一种更方便、更友好、更安全的方式,那就是尾插,通过它可以随意更改iPhone手机的定位。 这里面信息差不少,不知你们是否有兴趣,今天我就写一篇推文好好介绍一下。

中文

@aleabitoreddit Historical revenue from illegal activities which is basically mainland Chinese clients that were able to pass through the gaps of compliance screeners of these brokers.

Rule of law is stronger than you think in China

English

Feels like $FUTU and $TIGR are kinda screwed? The Chinese Gov is going after their historical revenues.

There's basically no fair law in China (esp. with IP), so if Gov wants something done, courts will be rigged against them.

So no chance of an appeal, unless they make a hidden deal. Also don't think the brokerages are able to pull a $GOOGL like their 20 decillion fine, given local operations

So TLDR: Good lesson learned to avoid Chinese exposure from $BABA to $PDD as much as possible...

And (as seen with $META + Manus + this case), even if something looks cheap.

There's a reason why all the US equities have premiums, even if a little high.

English

@juzou12345 @xqt1688 家里老人不帮忙看孩子的话压力会非常大 非常大 非常大(有钱另外,不看孩子就代表会损失一个年轻劳动力三年左右的时间,或者请保姆那就是一个月至少5000~10000+的人民币)

中文

@biggav @South_Lu @BurggrabenH 可以给你举一个例子:

1.城投公司全产业链条操盘,实体业务从产->销做成闭环,流水扩充数倍

2.链条的每个节点都是融资渠道

3.上级城投绑定下一级,上层要钱,下级要流水

中文

@South_Lu @BurggrabenH Its the largest economy in the world and it's growing at 5%. Clearly more sectors of the Chibese economy are prospering than not (real estate isn't, for sure). Mostly western countries haven't seen 5% growth in a long time.

English

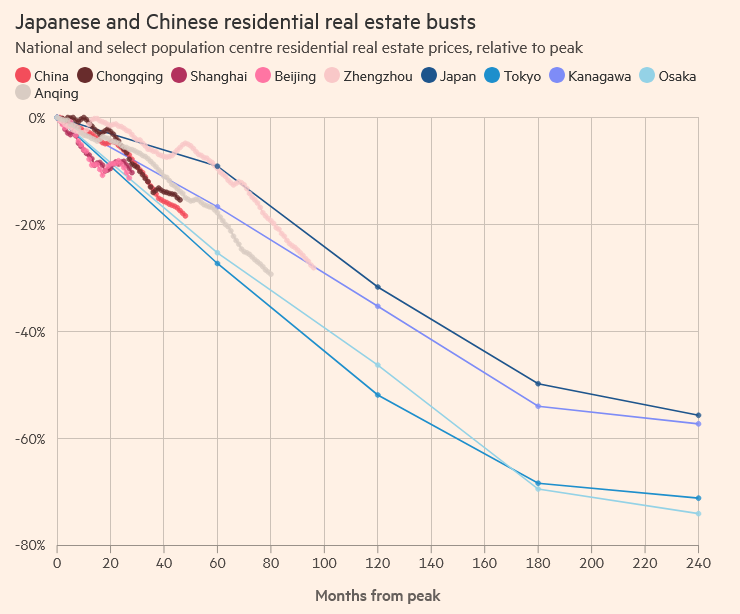

I explained the Chinese real estate & debt crisis in much detail in 2024 on my Substack. Nothing has changed since. China is in what we call "the largest balance-sheet recession the world has ever seen". And it will take years to get out of it and assuming the CCP's investment-led growth model does not dig the next hole in the meantime - a likely.

The FT published added some colour to it two days ago:

"Housing is important to every economy. But to China, it’s extra important. According to the PBoC, 96% of urban households own a home, and 41% own at least two. The average household owns 1.5 properties. And as such, property constitutes around 70% of China’s private wealth. The comparable figure for the US is around 30%. So when Chinese property prices fall, the authors make a pretty compelling case that this has all sorts of particularly bad economic spillovers. And fall they have.

The negative wealth effect is substantial, and “effects are amplified by elevated household debt, much of which consists of mortgage obligations”. This — and the weaker income expectations that the falls generate — goes some way to suppressing consumption.

Moreover, declining land-sale revenues constrain local government budgets, “limiting their capacity to finance developmental projects and maintain existing public infrastructure”. And this is even before any credit impacts from rising non-performing loans and mortgages on bank balance sheets are considered. Tl;dr: bad bad bad.

Of course, China isn’t the first soon-to-be-global-economic-hegemon-East-Asian-power staring down demographic oblivion to have piled its savings into a property boom. Back in 1991, the world was fretting over the rise and rise of Japan. And the Japanese were buying Japanese residential real estate at outlandish prices. Japan’s house prices peaked back in 1991 and spent the next 30 years on a downward trajectory.

We’re only a few years into the Chinese property bust, and its ultimate trajectory is both unknown and unknowable. But Rogoff and Yang have pulled together some cool data they kindly shared with Alphaville, allowing us to make this chart below.

So far, it looks like prices in Chinese cities are falling at around the same pace as they did over the first five-to-10 years of Japan’s bust. Japan’s property crash is associated with a lost decade (or two) of economic growth. In the 10 years leading up to 1991, Japanese real annual GDP growth averaged 4.4%. In the subsequent 10 years it averaged only 0.9% per annum.

The same numbers for China, with 2021 marking its property zenith, are 7.0% per year and 4.6% per year (so far). If the IMF’s forecasts turn out right, this latter number will fall to around 4.0% per annum. While the levels are different, the before-and-after drop looks comparable.

Was it housing wot dun it? Rogoff and Yang reckon that a 40% decline in house prices translates into a total consumption loss of 2-4% of GDP. Not nothing, but not a single answer explaining life, the universe and wiggles in the decadal pace of real economic growth.

To get here, they construct a historical dataset comprising subnational data across 47 prefectures, and input and output data at granular industry levels. They then use this to examine the macroeconomic implications of Japan’s real estate bust. And the authors argue that: a housing bust can generate substantial adverse effects on the economy via real channels. . . . overbuilding during the boom can trigger a demand-driven recession with limited reallocation and low output.

Unlike financial channels, which amplify shocks through leverage, bank balance sheets, credit constraints, or fire sales, real channels operate directly through investment, consumption, labour markets, or productivity. In Japan’s case, the housing market collapse depressed activity through three key real channels: investment, consumption, and sentiment. This is all pretty intuitive.

But using city-level and household-level Chinese data plus some whizzy maths, they put meat on the bone for these three channels. They find that Chinese cities that overbuilt housing the most are less keen on new building, suppressing investment. Sounds legit.

Chinese household consumption is estimated to be more responsive to house price changes than it was in either Japan or the US given its outsized role in private wealth. And it looks to the authors like people have scrambled to rebuild precautionary savings they thought they had amassed in property. Understandable.

Then, on the sentiment side, Rogoff and Yang use an LLM to gauge market perceptions of the housing market. And by incorporating city-specific perceptions, they double the estimated effect of house price changes on consumption. Huh.

While China is not Japan, 1991 was not 2021, and a *lot* of other things are/were going on, it’s interesting to see that the overall magnitude and pace of property price falls — as well as the aggregate drop in the pace of headline GDP growth — has (so far) been spookily similar. And as for the big question — are we there yet?

"If China’s adjustment unfolds in a similar way as Japan’s, it would mean China has not gone half way through the transition. By contrast, if China’s path is eventually comparable to the United States, it appears to have already covered roughly two-thirds of the adjustment before reaching the bottom."

So more to come.

English

@realExplosive @BurggrabenH 不好意思,有相当一部分购房者是欠着银行贷款的。我们国家里,很多在2019-2023年房地产高峰期买房的人,现在房价已经较买入时跌了30%-60%,不少人处于负资产状态,而且法拍房的数量也依然很多。

中文