StraightCap

74 posts

69 acres of private Tuscany for €690k ($797k).

The land includes an olive grove, a fruit orchard, a cork oak grove and 20 hectares of woodland. A natural spring produces 3,000 litres of water a day, solar panels cover the electricity and yes, it does have wifi.

It's also been renovated, 370m² (3,983 sq ft) across 3 floors, 3 beds, 3 baths, with a pool and a sauna. 50 km to Volterra.

Off-grid, self-sufficient, sauna, pool..what's missing here?

English

@evrgn11112231 Maybe not alpha but I materially have shortened the time it takes to do the other BS parts that come with working at an institutional fund

English

@RAMCOCAPITAL Idk a single bank who makes credit decisions off a FICO fwiw.

English

$FICO selling off on vantage score prices cuts? Customers are going rebuild their systems to use an inferior product to 10T and are confident the bureaus won’t take price? Banks get what they deserve.

English

FICO also soft on $TRU/$EFX taking VS pricing from ~$4 to $1 per score. My gut is this takes VS4.0 mortgage revenue at the Credit Bureaus from ~$0 before this cut to ~$0 afterwards because they are already giving away VS4.0 for free for anyone that buys FICO. Good PR though

English

@Larryjamieson_ Market share for 10T if Vantage is also in market will be less than 100% which is more my point

English

@StraightCap_ They haven’t even released Fico 10t, let alone vs 4.0 lol.

English

Discounting price is not a move you make when you’re in a strong position

Buyback Capital@Larryjamieson_

they used to give vantage scores away for free lol

English

@DrewCohenMoney Argentina profitability high mainly because there are no main competitors in ecom + have underinvested in logistics as a result. They’re now starting to invest there + ramping credit cards which hurts profitability upfront

English

Interesting

Yeah I had a suspicion given he left in 2022 (and that was a crazy time for commerce in latam and Shopee in particular)

But apart from his commentary just looking at the country level and segment disclosures, it still seems quite possible that Brazil ecomm isn't profitable

(now whether that is by choice and what happens to growth/ market share overtime if they decide to run it for profit is the real question)

English

So no one is making money in Brazil ecommerce?

Former Shopee Brazil President claims that nobody is making money in ecommerce in Brazil (Shopee or Meli)

(Says that Shopee doesn't attribute any shared overhead for tech to the Brazil segment)

Thinks that it is only $MELI's Mercado Pago arm that makes Meli profitable there

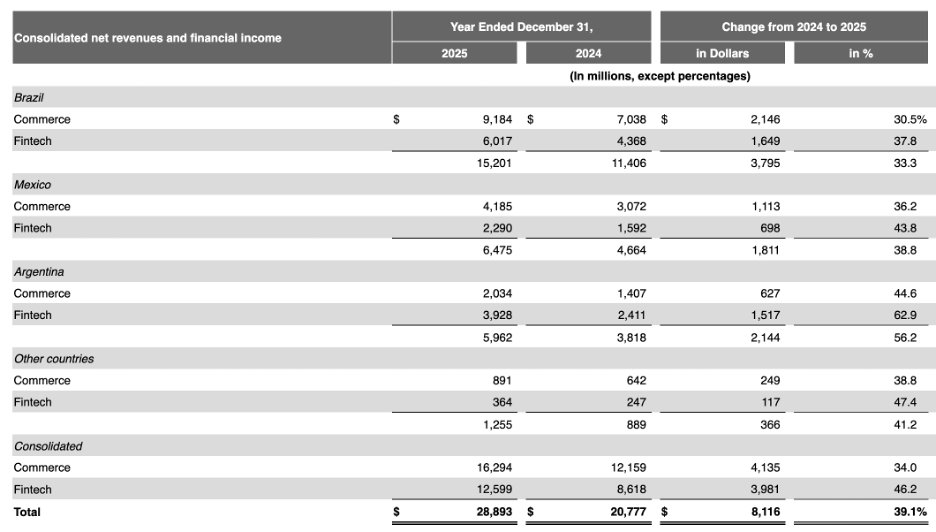

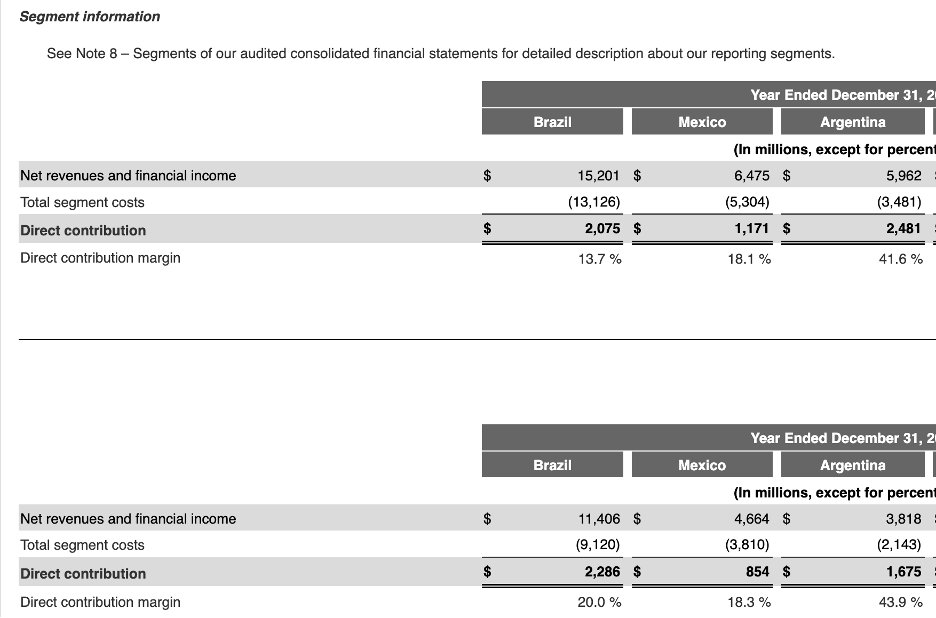

My take is that if you look at Meli's country level profits, Argentina generates $2.4bn in direct contribution profit versus Brazil at $2.1bn.

(Direct contribution profit is the country's revenues less all cost that can directly be attributed to that country... basically everything less shared corporate overhead)

This means they make more money in Argentina despite Brazil commerce being 4x larger.

How?

Fintech.

Argentina's fintech business is 2x as big as their commerce busines. In contrast, in Brazil, the fintech business is 1/3rd smaller than the commerce business.

While this doesn't rule out the possibility that Brazil ecomm is making some money, it does broadly support the Former Shopee Brazil president's claim that no one is making money in Brazil.

(One added complexity to this is Pix, which likely means Brazil is a worse market for Mercado Pago than Argentina.)

Now Brazil used to be at 24% direct margin in 2023 and now is at 13%... part of the bear case for Meli is that they were overearning before competitve intentisty picked up and now this new level of compeition from Shopee and also from Amazon re-entrentching could be permanent...

On the other hand, bulls will say they are purposely investing in the platform by cutting minimum delivery amounts and lower take-rates to gain more volume and thus build a more formidable moat overtime.

More to come.... new video dropping this weekend on Meli

per @AlphaSenseInc expert call $MELI $SE

English

@DrewCohenMoney I think Brazil e-commerce standalone is barely profitable but helped by a fast growing ads business. Credit card is unprofitable but the very large personal/smb loan book is extremely profitable. Acquiring biz/payments also very profitable.

English

@WaterworldCapi1 Why do you think the change in messaging on margins between previews and earnings? Something change dramatically?

English

@Fierce__beast Seems like a weird r/r where you either lose everything or make 300%. can't size it much

English

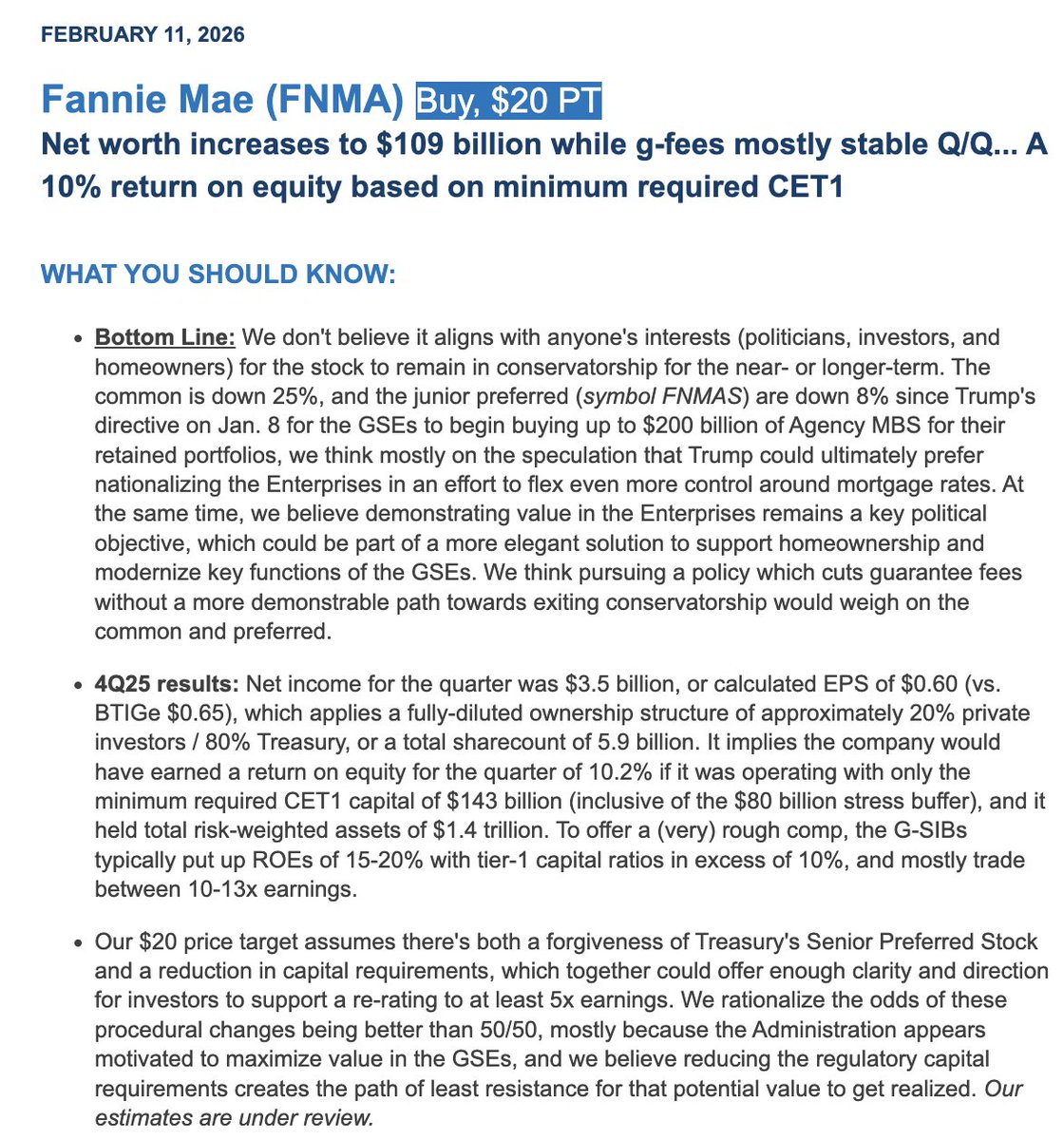

i am also long some $FNMA -- seems more like a political bet then anything else at this point. the value is clear

English

@Fierce__beast Mind sharing your prompt? Sounds like a cool use case

English

i use them to build bottoms up DCf models.

i use the same prompt for Claude, gemini, and chatgpt.

if all three have the same EPS estimate, i assume it's correct. and do another closer look and iterate. I have my own spin on how to get EPS. definitely not non-gaap, usually it's significantly lower.

i then try to estimate growth rate and risk myself and come up with a price range for its lifetime expected cash stream

Generals & Workouts@gw_investing

How is everyone using LLMs in their investment process? They seem very helpful for basic research and fact finding. But I find analysis by models (e.g. help w/ modelling special sit outcomes) is generally bad. Somewhat reassuring for those of us who learned to value stocks pre-AI

English

@gordocap18 I think the market is not appreciating the amount of folks planning on moving to Vantage in the near term…think material share loss is a q4’26/q1’27 possibility. Once that’s the narrative = 20x eps

English

@evrgn11112231 @taobanker @SurfingSecular Just started ramping on this ..Found some of the back and forth here helpful / took me to the court filings.

Are you all still involved / think it's interesting? If acres burned continues to CAGR MSD% + HSD% pricing, isn't the core biz worth 50% more per sh than wholeco...?

English

@GDgiulio_ @taobanker @SurfingSecular Sure but if you are scrappy and know where to look you can piece together a lot more - can get pretty good views on hist px vs volume which is the key to unpacking both the source (and sust) of value creation and actual volume cyclicity (not just acres burned shorthand) and grwth

English

$CMP Compass Minerals just SHUT DOWN its fire retardant unit. In the end, its "revolutionary product" was nothing special (it actually had serious flaws that a serious DD would have highlighted). $PRM can finally say goodbye to this once "formidable" and noisy competitor.

English

@Aureliusltd28 Stne is a terminally declining biz with upside thanks to potential rate cuts

Meli is a compounding machine going thru a clearly offensive investment cycle with similar rate cut tailwinds possible. Market has 1-2 quarter duration these days and so investment cycles are punished

English

@evrgn11112231 Agreed - hard to explain in words other than I find 5 very lazy. I think people will say o3 was more creative/thoughtful but that was because it was simply hallucinating more.

English

Canceled my ChatGPT Pro sub today as it has become pretty unusable for me since the GPT-5 roll out.

Let me know when the experience is back to 4o + o3 pro level again.

Evergreen@evrgn11112231

Also forgot Zuck hollowed out a lot of top talent from OAI. Are we starting to see lagged effects on product here? My ChatGPT has become borderline unusable over last few weeks but I chalked that up to them throttling compute as they are diverting to wider use cases (like Sora) in an attempt at finding a sustainable business model. Any thoughts? @lokoyacap

English

@FoldedThroneCap Not involved but I’ll say the Kalshi “combo” / parlay UI is a lot more intuitive than traditional sport books … overtime not sure why they wouldn’t be able to offer the same depth if marketmakers on other side.

English

I don't even own $DKNG or $FLUT but when talking about prediction markets why does literally everyone forget that both of them make the majority of their money off player props / parlays? That isn't something prediction markets can monetize anytime soon

English

@Fierce__beast They don’t have a real reason is the short answer. They thought they’d reaccel 2H’24 and never happened. Team has no visibility and the new CEO is going to want to invest for growth (take down margin target)

English

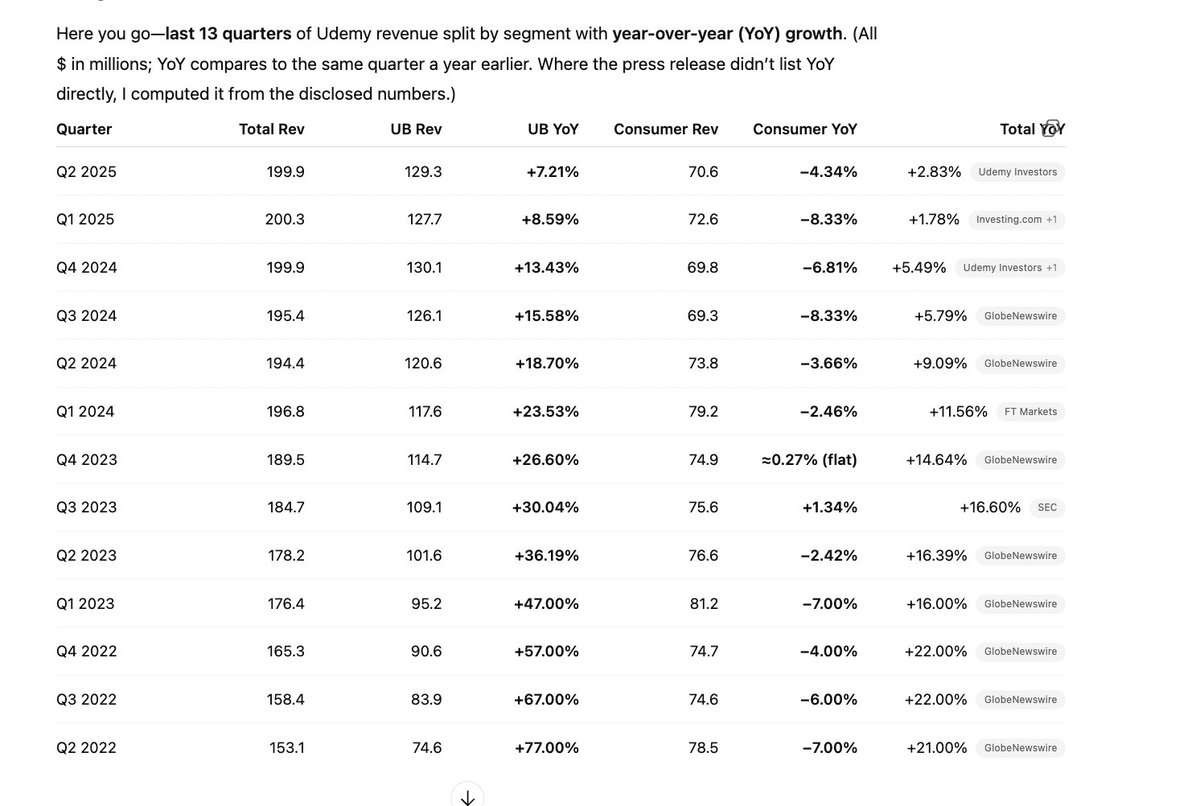

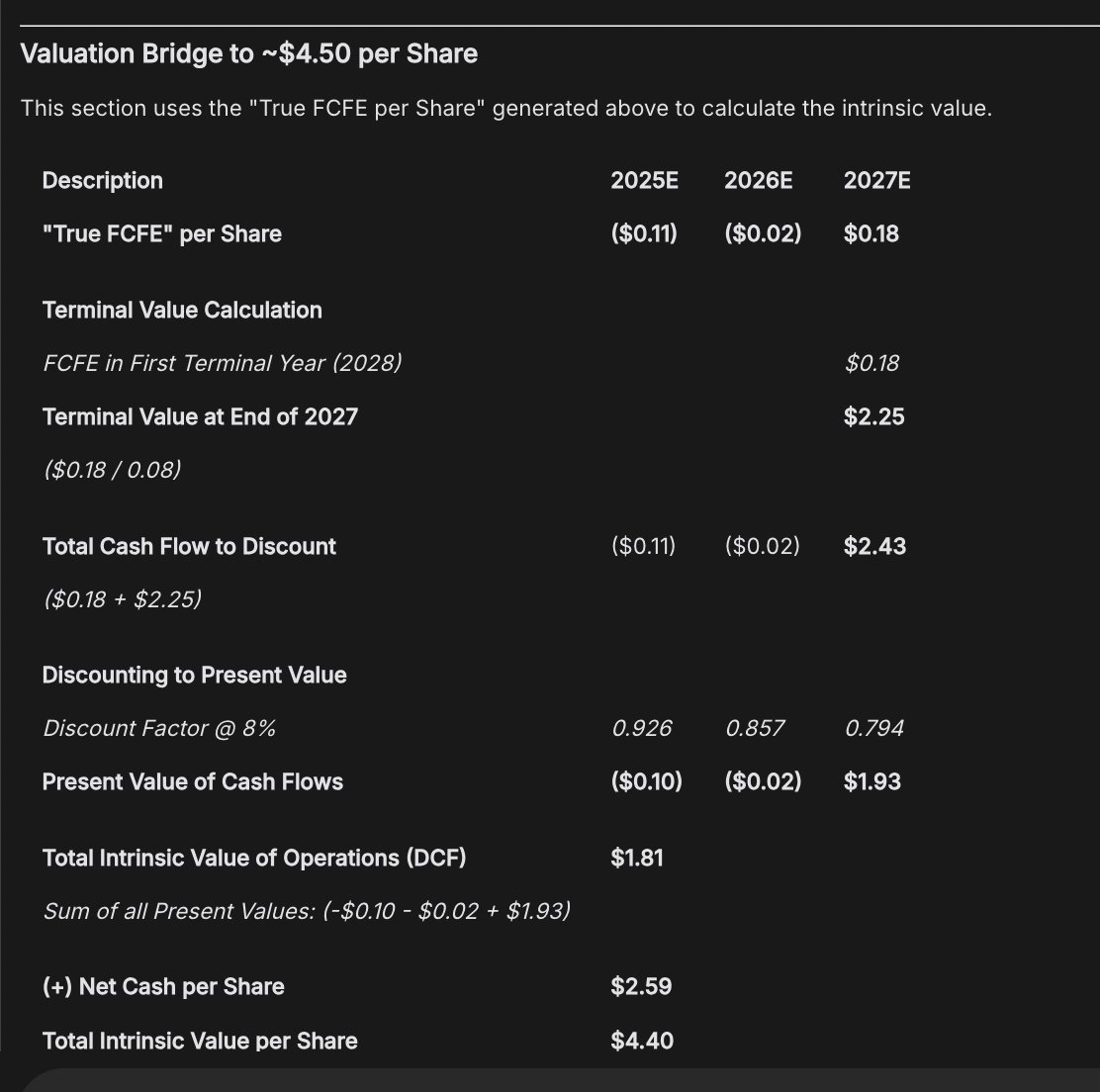

I am short $UDMY, PT 4.5/sh for >30% downside

it has ~2.5/sh in net cash but think the chances of it attaining a breakeven fcfe level is unlikely if they are unable to reaccelerate revenue growth. So the equity stub is worth very little.

They need at least ~13% adj. EBITDA margins by my estimate to break even on FCFE. If the enterprise continues to decelerate total revenue growth will be negative in a few quarters and the chance of reaching scale will become extremely remote. I think they'll maybe earn .25/sh of FCFE by 2027, but they may need to sacrifice growth to obtain this.

I've provided one scenario of stagnant growth but 15.5% Adj. EBITDA margins by 2027 which is sort of in line with management's LT adj. ebitda target of 17-20% and what I think would likely happen to revenues if they got there -- implied here is a large reduction of SG&A for marketing/ad spend, and or reduction of sales people. Here the PT is around 4.5/sh assuming an 8% discount rate and 0% terminal growth.

Consensus estimates have both margin and revenue growth expansion forecasted which does not seem likely given the recent trends of deceleration across both segments of their business which presumably have no first principles explanation -- more of the typical higher churn, lower NDR, difficult macro etc -- but i suspect its due to some sort of declining value proposition of their services or alternatives like AI agent based learning.

My longer term vision is that human generated video content and learning as well as the ~250k lessons of inventory that UDMY champions to have and advantage them may become obsolete in terms of both content and distribution method due to AI.

It's more of a suspicion than some sort of confirmation so we'll see how the next quarter proceeds but if this bear thesis is correct, then we should see further deceleration of growth or some sort of margin deterioration if growth holds up.

On their enterprise business management has provided a prediction of a near-term bottoming then improvement path: NDR to bottom in Q3’25, be flat in Q4’25, and accelerate in Q1’26, citing (1) a larger pipeline (record $100k+ deal count in Q2), (2) higher win rates, (3) outsourcing SMB renewals so internal teams focus upmarket, and (4) a new Chief Customer Experience Officer to improve renewal/expansion motion. I fail to understand why they have this prediction, what first principles reason do they provide to justify their views--I could not find one.

English

@Fierce__beast oh sorry - my reply probably made that confusing. This company is worth 0

English

Lol chatgpt just spits out a great bear thesis on stocks. Here's one for $UDMY:

UDMY: a concentrated bear thesis (as of Oct 15, 2025)

1) Growth looks stalled, not inflecting

Latest quarter (Q2’25) revenue grew just 3% YoY to $199.9M; management’s FY’25 guide of $784–$794M implies roughly flat revenue vs. FY’24 ($786.6M)—hard to support a premium multiple if the top line isn’t expanding. SEC+1

The engine that’s supposed to carry the story—Udemy Business (UB)—isn’t accelerating: ARR up only 6% YoY to $520M, and UB revenue up 7%. Customer count rose just 3% YoY to 17,107. That’s mature-company growth, not a reacceleration. SEC

Guidance also implies a sequential revenue dip in Q3 ($190–$195M)—seasonal, yes, but it reinforces the “no growth” setup until proven otherwise. SEC

2) Deteriorating retention signals weak expansion

UB Net Dollar Retention fell to 95% (large customers: 99%) in Q2’25—below 100% means downsell/churn outweighs upsell. A year ago (Q2’24) NDR was 101% and 108% for large customers. That multi-quarter downtrend is a red flag for enterprise health. SEC+1

3) Consumer marketplace: structurally pressured

Consumer revenue declined 4% YoY in Q2’25; monthly average buyers fell 3% YoY. The small bright spot—consumer subscriptions—was only 15% of consumer revenue in Q2 and may be cannibalizing higher-priced a-la-carte purchases. SEC

Udemy is boosting margins partly by cutting instructor subscription revenue share from 25% (pre-2024) → 20% (2024) → 17.5% (2025) → 15% (2026). That helps gross margin near-term, but risks alienating top creators and course freshness—the moat for any marketplace. (This change is official policy.) teach.udemy.com

(Independent tracking and industry coverage have echoed these reductions and instructor frustration, underscoring supply-side risk.) Class Central

4) Competitive and technological headwinds intensify

Coursera is re-accelerating (Q2’25 revenue +10% YoY, raised FY’25 guide), signaling that budget is available—but may be skewing toward competitors with stronger degree/credential franchises and campus/business channels. Coursera Investor Relations+1

Generative-AI tutors and integrated learning in productivity suites compress the value of static course catalogs. A 2025 Nature study showed AI tutors driving significantly more learning in less time—a structural threat to paid, video-first courses. Investor appetite for traditional edtech has also fallen sharply as free/AI tools proliferate. Nature+1

5) Profitability is largely cost-driven (and may not be durable)

Q2’25 was the first GAAP-profitable quarter ($6.3M net income; Adj. EBITDA margin 14%)—great progress, but it rode opex cuts (S&M, R&D, G&A all down YoY) as much as growth. If management has to re-invest to re-accelerate (sales capacity, product, brand), margins can slip. SEC

6) FX and international exposure add volatility without hedges

Q2’25 growth had ~1–2 percentage-point FX headwinds (worse in Consumer). The company has previously disclosed no currency hedging, leaving reported growth and cash flows more exposed to USD swings. SEC+1

7) Capital allocation doesn’t cure the growth problem

Udemy finished $150M of buybacks in 2024 and still has a strong balance sheet ($393M cash/securities at Q2’25; new $200M revolver). Helpful, but repurchases can’t mask flat revenue or weak NDR—the stock can stay cheap if growth doesn’t come through. Udemy Investors+2The Wall Street Journal+2

Downside catalysts to watch

NDR stays <100% for multiple quarters—evidence that seat contraction/churn persists in enterprise. SEC

UB ARR growth stuck mid-single-digits; inability to monetize new AI “packages” or to upsell beyond compliance/soft-skills. SEC

Consumer erosion continues despite higher take-rates; visible instructor pushback or migration of top courses to rivals. teach.udemy.com+1

Competitors compound gains (Coursera guidance/enterprise wins), capturing share in enterprise L&D budgets. Coursera Investor Relations

FX or macro layoffs pressuring seat counts; minimal hedging keeps reported metrics volatile. SEC+1

What would disprove this bear case

UB NDR >100% for 2+ consecutive quarters and ARR growth back to double-digits. SEC

Consumer subscriptions becoming a substantive mix (say 25%+ of Consumer revenue) without weakening the marketplace. SEC

Demonstrable ROI from AI features that lift win rates/expansions (and not just press-release features). SEC

Sustained FCF margin at mid-teens with re-accelerating revenue (not just cost control). SEC

TL;DR

Udemy’s growth is flat, enterprise retention has slipped below 100%, consumer is shrinking, and competitive/AI forces are eroding pricing power—while recent profitability leans on cost actions and instructor take-rate cuts that may not be sustainable. Until the company re-accelerates revenue and repairs NDR, the stock can remain a value trap despite cash and buybacks. Nature+4SEC+4GlobeNewswire+4

Not investment advice. If you want, I can build a one-pager scoreboard (NDR, UB ARR growth, Consumer mix, FCF) you can track each quarter.

English