Tes Obs

15.5K posts

Tes Obs

@TesObs

Nov24: Every Tesla Bull & TSLA investor should buy a Cybertruck + FSD to experience the pinnacle of Tesla's moat in their bones! Your conviction will 🚀 🌕 🌞

Stand By Me

$TSLA - MUSK HAS DISCUSSED WITH COLLEAGUES THE POSSIBILITY OF FOLDING TESLA-SPACEX TOGETHER - CNBC

Chamath Lays Out the Case for SpaceX at $2 Trillion – Starlink: the most important internet infra project since the internet itself – Rockets: underlying platform that allows everything else to happen – AI: apps top layer, datacenter bottom layer – The Elon Flywheel: operating leverage ➡️ investment ➡️ competitive moat ➡️ capital moat ➡️ technology moat ➡️ execution/learning moat – Potential Tesla merger down the road – Elon’s premium for being “the guy” right now @chamath: “ If I'm asking myself, ‘Chamath, how do I underwrite SpaceX at $2T?’ Here's the basic math that I would do. Last year it did $18-19 billion. It'll probably do $25-30 billion this year. So I'm buying this thing at a fairly costly premium, right? So what am I buying? I'm buying probably the most important internet infrastructure project that's happened since the internet itself. That's going to scale to hundreds of millions of users, and the reason that's going to scale to hundreds of millions of users is it's just very useful, and it's just going to become cheaper and cheaper and cheaper. So that's number one. I'm buying a delivery infrastructure, I think over time, GDP plus 10, GDP plus 15, kind of a grower. So good business, valuable business, but it's the underlying platform that allows everything else to happen. And then I'm buying an AI business, which will be at the top level the apps, but at the bottom layer all the compute capability. So I suspect what happens is next year it's probably $40-45 billion. And then the year after that it probably doubles again, so then I'm buying it at 20x revenue. And you would say, ‘Well, why can you buy a company like this on revenue versus earnings and cash flow?’ And I think the reason is because what the revenue does is it gives him the operating leverage to go and invest in all of these other businesses that ultimately consolidate his differentiation and his competitive moat, because what he creates is a capital moat that then accelerates a technology moat, that then accelerates an execution and a learning moat. And that flywheel, when it starts to spin very quickly, and you would say, ‘Hey, hold on a second. It's probably spinning quickly now.’ I would say we're at the beginning of the beginning. He still has all these disparate assets. I still don't like the fact that Tesla's over here, and as I've told you, that will get merged in. And now you have this incredible corpus of physical capability, movement of all kinds, X, Y, and Z, right? That thing will look very cheap, I think, in a few years. And he has this one thing that nobody else, if you look at the big CEOs, who steps on stage where you're always curious, ‘Okay, what has he got up his sleeve?’ You know, the Steve Jobs, ‘Oh, and one more thing.’ He's the guy. Whether you like him or you hate him, he's the guy, and there's a premium that is well-deserved that comes with that.”

Chamath Lays Out the Case for SpaceX at $2 Trillion – Starlink: the most important internet infra project since the internet itself – Rockets: underlying platform that allows everything else to happen – AI: apps top layer, datacenter bottom layer – The Elon Flywheel: operating leverage ➡️ investment ➡️ competitive moat ➡️ capital moat ➡️ technology moat ➡️ execution/learning moat – Potential Tesla merger down the road – Elon’s premium for being “the guy” right now @chamath: “ If I'm asking myself, ‘Chamath, how do I underwrite SpaceX at $2T?’ Here's the basic math that I would do. Last year it did $18-19 billion. It'll probably do $25-30 billion this year. So I'm buying this thing at a fairly costly premium, right? So what am I buying? I'm buying probably the most important internet infrastructure project that's happened since the internet itself. That's going to scale to hundreds of millions of users, and the reason that's going to scale to hundreds of millions of users is it's just very useful, and it's just going to become cheaper and cheaper and cheaper. So that's number one. I'm buying a delivery infrastructure, I think over time, GDP plus 10, GDP plus 15, kind of a grower. So good business, valuable business, but it's the underlying platform that allows everything else to happen. And then I'm buying an AI business, which will be at the top level the apps, but at the bottom layer all the compute capability. So I suspect what happens is next year it's probably $40-45 billion. And then the year after that it probably doubles again, so then I'm buying it at 20x revenue. And you would say, ‘Well, why can you buy a company like this on revenue versus earnings and cash flow?’ And I think the reason is because what the revenue does is it gives him the operating leverage to go and invest in all of these other businesses that ultimately consolidate his differentiation and his competitive moat, because what he creates is a capital moat that then accelerates a technology moat, that then accelerates an execution and a learning moat. And that flywheel, when it starts to spin very quickly, and you would say, ‘Hey, hold on a second. It's probably spinning quickly now.’ I would say we're at the beginning of the beginning. He still has all these disparate assets. I still don't like the fact that Tesla's over here, and as I've told you, that will get merged in. And now you have this incredible corpus of physical capability, movement of all kinds, X, Y, and Z, right? That thing will look very cheap, I think, in a few years. And he has this one thing that nobody else, if you look at the big CEOs, who steps on stage where you're always curious, ‘Okay, what has he got up his sleeve?’ You know, the Steve Jobs, ‘Oh, and one more thing.’ He's the guy. Whether you like him or you hate him, he's the guy, and there's a premium that is well-deserved that comes with that.”

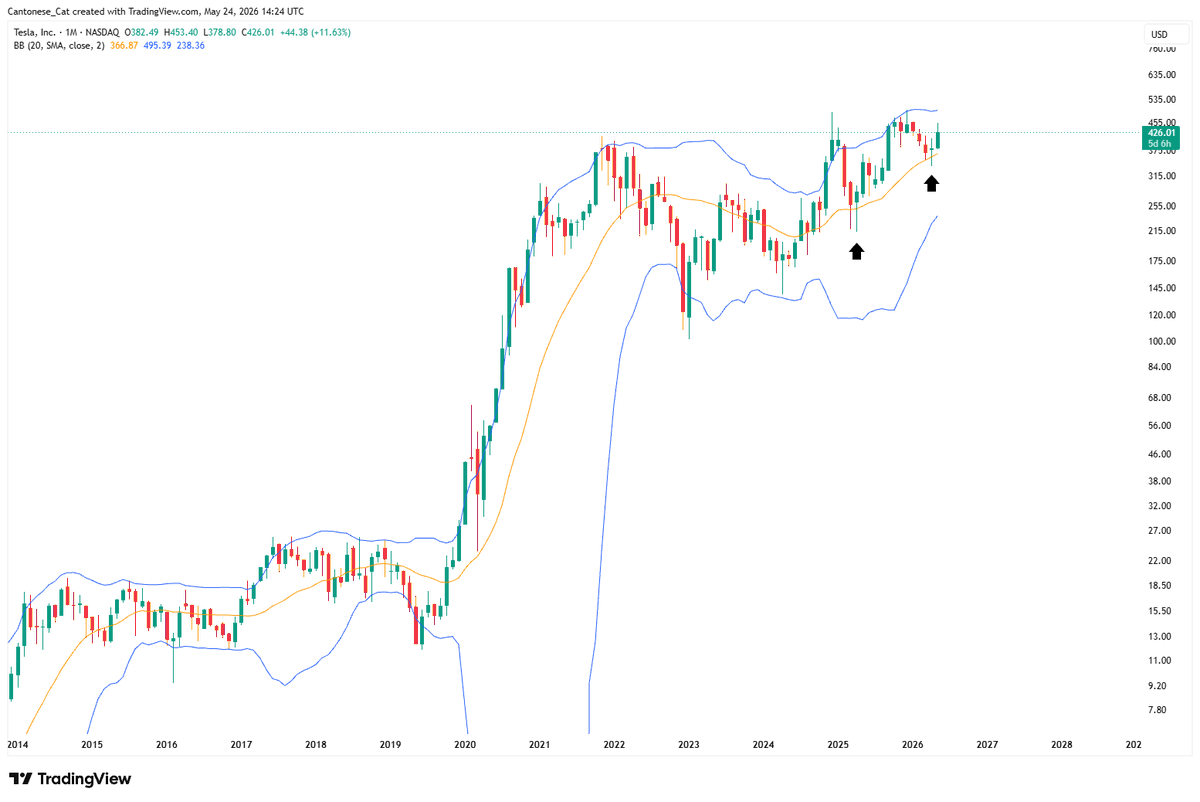

$TSLA monthly chart looks bullish. I don't think it ends here. Nobody knows how high it would go. But I think it could reach $700-$900 in 2025, based on the strong bull trend that started a few months ago.

Interesting

This captures what I've been thinking for a while now. However, I'm still waiting for a few different people to do the actual analysis of the value of Tesla versus SpaceX for a potential merger by: Looking at the TAM for each company, the expected proportion of the market, the likelihood of success, factoring in multiple time frames, the time value of money, and potentially even the opportunities that you could be missing out on in the meantime. On that last one, basically I mean that stocks can stay flat for years while other ones pop up. I'm not a financial analyst, but it shocks me that I haven't seen anyone do this analysis or something similar yet. Maybe it's just too hard. To me, it boils down to a bird in the hand is worth two in the bush. Would I rather have a potential 40x in SpaceX over the next 20 years, or a 10x in Tesla over the next 5 years? For me it's a no-brainer, and Tesla should be much more than 50% of a potential merger.