Sabitlenmiş Tweet

I manage a Facebook group for Nebius Investor, facebook.com/groups/2355224… feel free to join, we have 750 members as of Jan-2026

English

Stephen, Every Tree Counts

396 posts

@ValuePlay52109

Value-Investor, Support Socialistic Capitalism with a light-UBI (10-20% basic living income), a low carbon footprint life, To plant 8 billions trees annually.

JPM software channel checks ( $NOW, OpenAI/Clickhouse ( $NBIS), Anthropic, $DT, etc. read thru):

OpenAI is transitioning away from Datadog and into ClickHouse services, where $NBIS holds a 25% stake

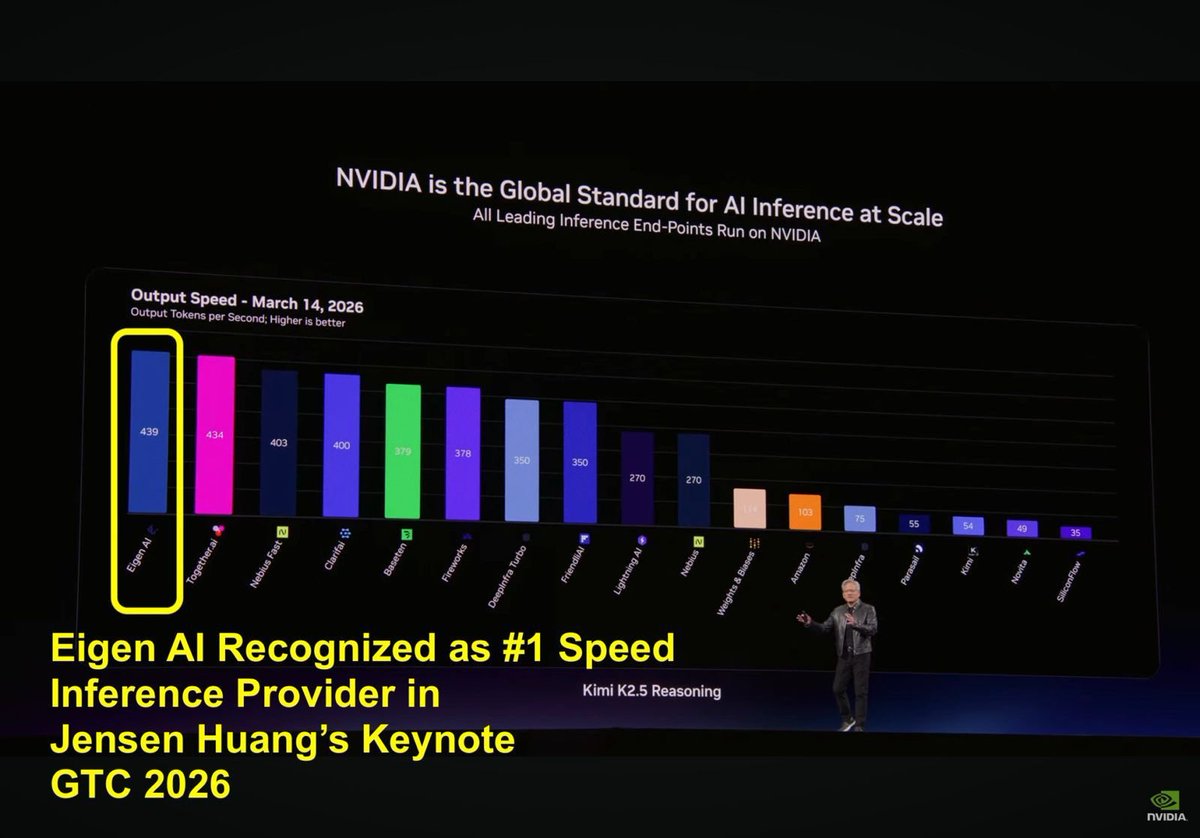

$NBIS TO BUY EIGEN AI FOR $643M Nebius says the deal will add Eigen AI’s inference and model optimization tech to its Token Factory platform, aimed at improving model performance and unit economics at scale. The deal is expected to close in the coming weeks.

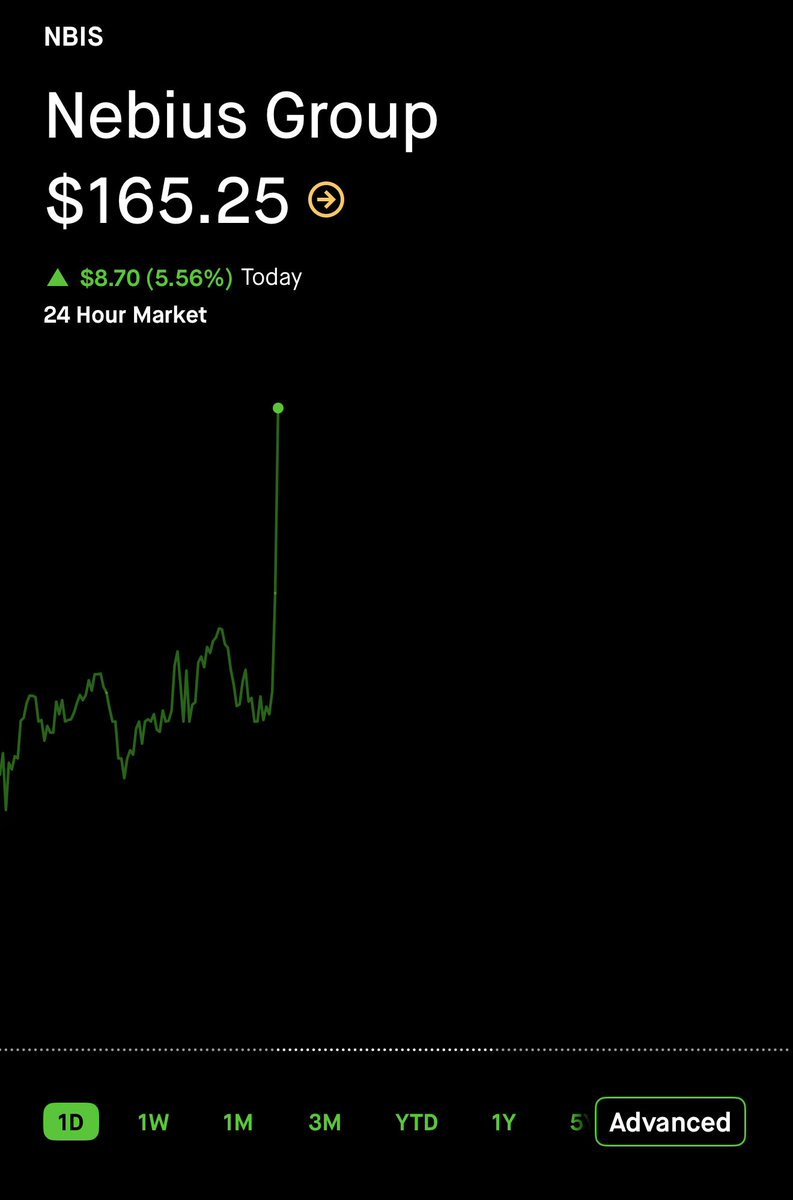

Moved my last 10% cash into $NBIS today at $136 and have now reached degen levels of concentration again. Nice! 77% $NBIS 8% Towa (6315) 8% $HIMS 7% $OUST If you go back and read my portfolio update where I trimmed Nebius from 75% to 20% (at the exact top) I told you that this was my plan. Wait for the stock to cool down. Slowly add it back and keep enjoying the ride up. The word needs more compute and Nebius delivers a world class cloud experience and crushes benchmarks. I believe it is by far the best positioned company to profit long-term from this environment, because they optimize the value of every MW of capacity through an increasingly distinguished and complete compute product that meets customers at the level of complexity they want and need! In a world where many companies have no moat and either grow like crazy or make a little money, I believe Nebius is building a cash printing business, while growing 600-800% yoy and all of that while establishing strong moats and a defensible, recurring revenue business that is loved by many and soon will be loved by even more customers. Customers and partners love working with Nebius and literally can't get enough compute. They also appreciate how Nebius helps them maximize performance and optimize efficiency. Nebius will take care of you.