Brett Caughran@FundamentEdge

A very thought provoking piece and well worth a read.

I agree with some of the points here, disagree with many, with respect to the intellectual rigor & nuance embedded in this argument.

A few thoughts I had, on the finance vertical LLMs specifically.

(and fwiw big fan of Fintool...it was one of the highest rated finance co-pilots in the market on our internal evals...it's a genuinely helpful tool)

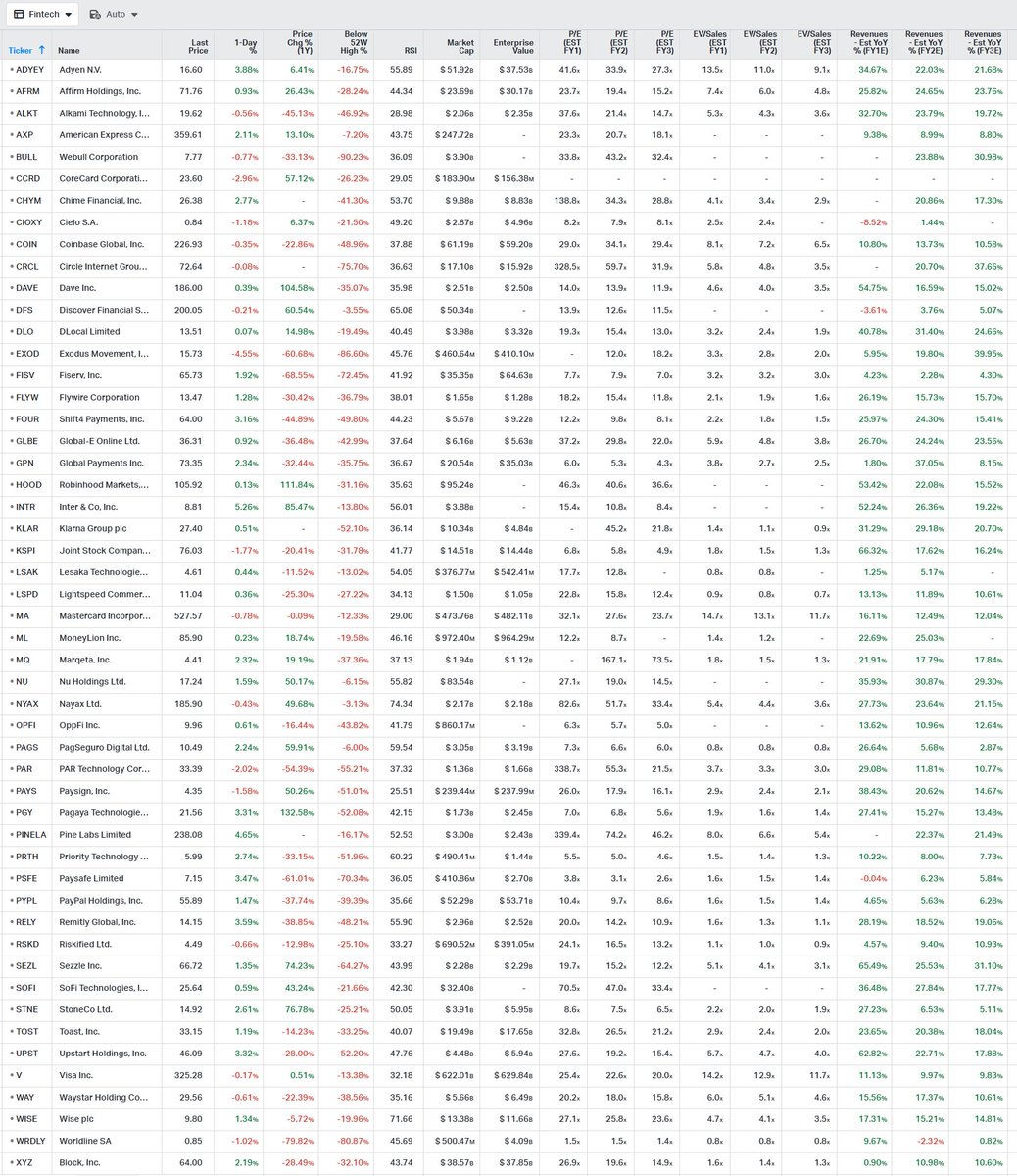

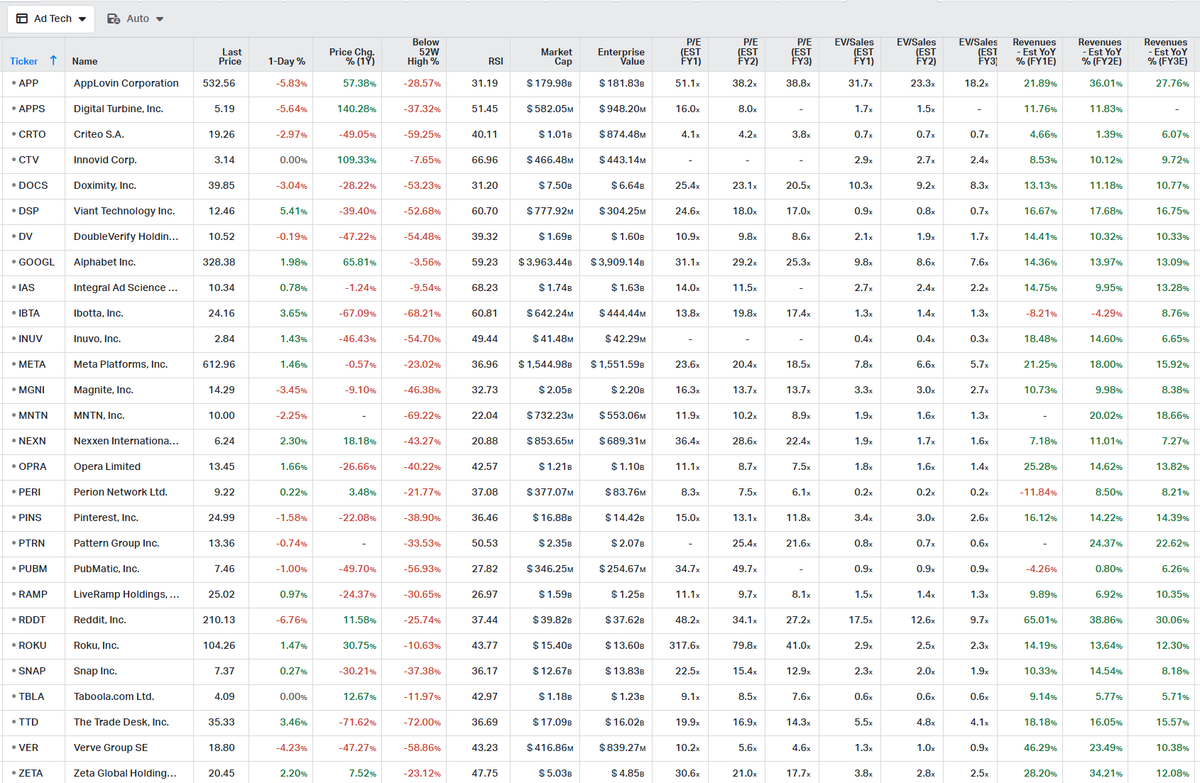

1) The downside of combinatorial competition. We have seen this play out in real time the finance copilot market. LLM's haven't enabled 10 new competitors...they have enabled 100+ new competitors. Much of the initial ARR is founder relationship driven, so this effectively serves to chop the market and lead to "demo fatigue" amongst clients. It feels like this will have to shake out at some point, and capital & staying power will become a moat. But "100 competitors chasing a market" is a lot more difficult than "1 competitor entering an established market" for simple scale & escape velocity reasons.

2) Single pane of glass is powerful (more powerful than most vendors realize). A friend mentioned to me "between these 7 different finance co-pilots, I can patch together quite a useful operating system". But, of course, that is a highly expensive, cumbersome set-up, and he defaulted back to "waiting for AlphaSense to catch up". Many investors are hoping for Bloomberg or FactSet (their incumbent provider) to build a helpful AI overlay. The combinatorial competition and the reality that many co-pilots are stuck in the $500k-$3m ARR neighborhood exert reflexive pressure on the ability to scale data & engineering to serve that full stack of workflows.

To overcome this single pane of glass propensity requires highly meaningful differentiation...Tegus/AlphaSense is really the only vendor who has done this at scale over the last decade in finance, and they had to create a brand new category of research tool (expert network transcripts) to do it.

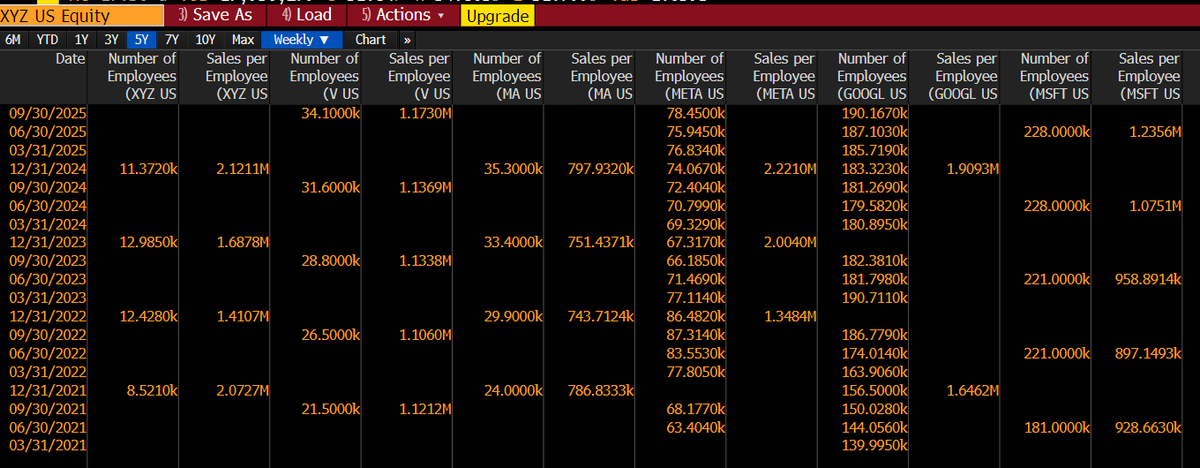

3) The moat (one of many) of the terminals is comprehensive data. It's not publicly disclosed, but Claude (via source: Getlaka) estimated Koyfin's revenue at ~$4m ARR. Koyfin is quite a well built tool. I am a big fan of the tool and teach to it in my ASU class. Koyfin licenses CapIQ data, per Claude. But of the 50 things I need a terminal to do, it can still only do 35. That's a problem. And it's sort of a binary yes or no 35/50 means my personal "single pane of glass" is still FactSet. $18k is a small price to pay of the seamless enablement of 50/50 of the workflows I need done. That seems to be a really hard nut to crack (requires a lot of capital and a "build it and hope they come" mentality).

Unfortunately, I think a lot of finance LLMs will get stuck with the "Koyfin" problem - great tool, but limited data stack and hard to scale.

I obviously take the "over" on business quality at Bloomberg, FactSet & CapIQ and think these will continue to be very hard businesses to disrupt (while keeping an eye on what @fiscal_ai is doing on the data side).

To put it another way, Bloomberg is a business that probably could be disrupted, but it may take $300m of cash burn to do it (which, to be fair, may be down from $3bn pre LLMs) in any meaningful way.

4) There are some unit economics questions. Most (all?) finance co-pilots are still running on a CapIQ or FactSet API. If finance co-pilots do scale enough to eat terminal share, these data vendors can either 1) pull API access (not likely, in my view, as they view LLMs as a key distribution layer for their data) or 2) raise API price (likely, in my view). A typical finance co-pilot charging $3-5k a year sitting on an API of data that goes through a terminal at $15-$20k via FactSet or CapIQ. I still struggle to see how that reconciles & scales. If terminals did (at some point) start to lose seat share to LLM co-pilots, why would the terminals continue to subsidize their own death? The rational response at that point would be to 2x the price of the API...

Also, as 5x more expensive LLMs deliver 50% better performance, end users will demand the latest frontier models, but many of these capital constrained co-pilots will struggle to keep up. My sense it is quite expensive to use Opus 4.6 / ChatGPT 5.2 API (are APIs available yet?). Need to dig a little more on this, but after using so many co-pilots I find myself coming back to Opus 4.6 directly as the model is just GREAT, when prompted & sourced.

5) Technical hurdles are still real, and not solved (yet). Are LLMs + MCP the right technical stack? Or is that too brittle? I have no idea, but LLMs + MCP still seem to make loads of mistakes, more errors of "omission" (needle in haystack problem). This is where nearly all internal builds have failed...IT teams don't have the context to know what good looks like, the tool gets in the hands of the investors, and misses a simple data point that was critical in answering the question well. I don't know exactly why this is, and it's getting better, but it's still not reliable enough to drive widespread behavior change in institutional finance.

6) Claude Excel isn't good. It can do a few small, interesting things here and there. But for any real institutional-grade workflow, it sucks. It breaks, it stalls, it gets confused. Now, at least Claude can interact with Excel! That is progress.

Two way interactivity with Excel (push button builds, key driver identifications, distillation of broad research feeds back into Excel architecture) is the "holy crap" moment in AI for Finance. It changes the game, and is a big opportunity for the vendor who nails it (in my opinion).

But today, AI Excel still isn't close to good enough, and Opus 4.6 is an absolutely, mind-blowingly good model in so many other ways.

This isn't mean to be criticism at all. I've been trying to put myself at the intersection of finance & AI one because it is interesting, and two because it just has so much obvious potential. And I try to remind myself that 18 months ago I couldn't even really figure out anything helpful in my research workflow. That has certainly changed (though I still continue to update models & read transcripts the old fashioned way).