Luke Fan | e/acc

1.2K posts

Luke Fan | e/acc

@baaadkk

building @magnetaixyz and writing some of my observations

Palo Alto, CA Katılım Mart 2013

678 Takip Edilen401 Takipçiler

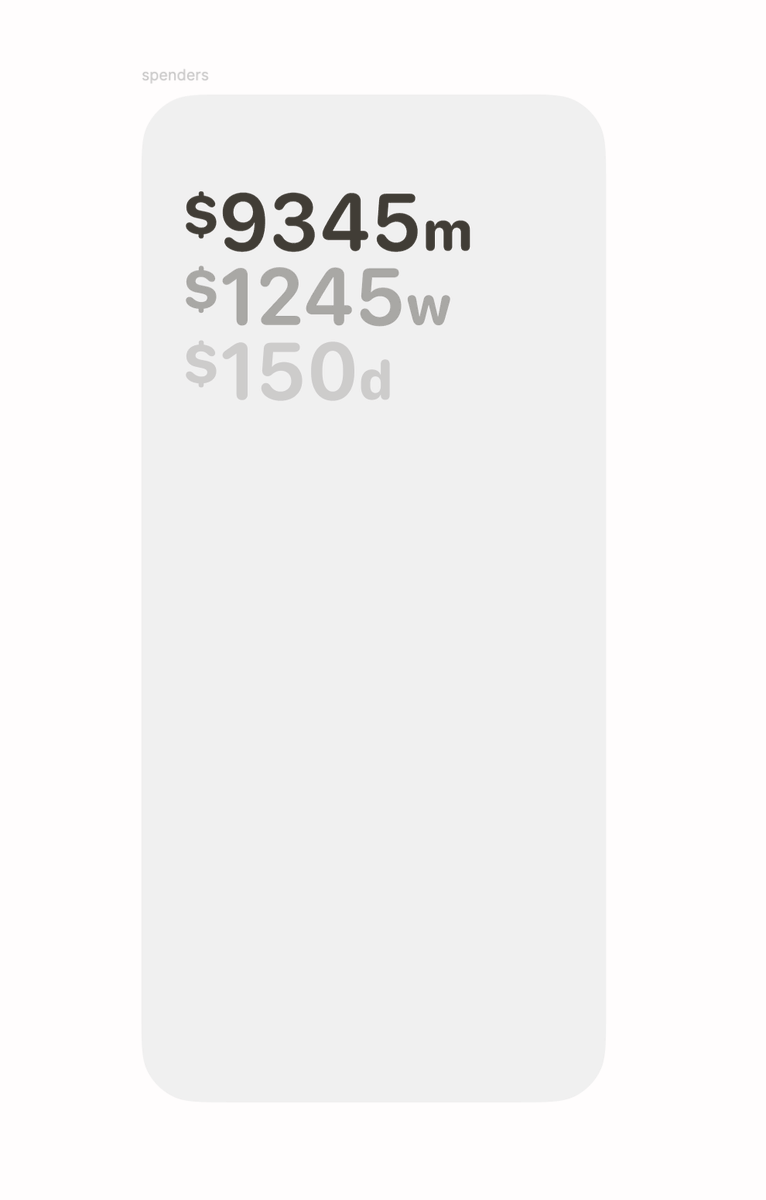

Open sourcing this idea, here's the blueprint:

I think it needs:

- chart of this month vs last

- category summaries

- running list of all transactions

good luck!!

Preston@metapreston

1M views. people want this app

English

Programmatic payments between machines: Imagine AI agent-powered marketplaces automatically brokering deals for computer resources and other services.

Chris Dixon@cdixon

Stablecoins: Payments Without Intermediaries The internet made information free and global. So why is it still so hard — and expensive — to move money? The early internet promised a future where anyone could publish, build, or transact without permission. Protocols like email and the web were open and neutral — and they sparked an explosion of creativity, innovation, and entrepreneurship. But somewhere along the way, we veered off course. Today, the global financial system resembles a patchwork of corporate networks: centralized, closed, and extractive. Behind every transaction is a Rube Goldberg-machine of intermediaries — points of sale, payment processors, acquiring banks, issuing banks, local banks, correspondent banks, foreign exchanges, card networks, and others — each taking a cut, adding latency, and imposing rules. These networks levy unnecessary taxes on commerce and curb innovation. They turn what should be neutral plumbing into high-friction bottlenecks. Stablecoins, or cryptocurrencies pegged to stable assets like the U.S. dollar, are a way out, a reset — a way to bring the internet’s original vision to money. The Disruptive Opportunity of Stablecoins The current payments stack wasn’t built for the internet — it was built for a world rife with fee-taking middlemen (who had been necessary to manage local partnerships, fraud, and operations). Even today, international remittances can cost up to 10% in fees. (A $200 remittance cost 6.62% on average in September 2024.) These aren’t just friction points — they’re effectively regressive taxes on some of the world’s poorest workers. The system we’ve inherited is slow, opaque, and exclusionary, and it leaves billions of people underserved or entirely cut off from the global financial system. For many businesses, the inefficiencies of traditional payments are also massive. Stablecoins could dramatically improve the situation. B2B payments from Mexico to Vietnam take 3-to-7 days to clear and can cost anywhere from $14-to-$150 per $1000 transacted, passing through as many as five intermediaries along the way, each of whom takes a cut. Stablecoins could bypass legacy systems, like the international SWIFT network and associated clearing and settlement processes, and make such transactions nearly free and instant. This isn’t theoretical — it’s already happening. Right now, companies like SpaceX are using stablecoins to manage their corporate treasuries (including by repatriating funds from countries with volatile local currencies, like Argentina and Nigeria). Other companies, like ScaleAI, are using stablecoins to make faster, cheaper payouts to global workforces. Meanwhile, on the B2C side, Stripe is the first widely used service to offer crypto payments and it is already offering 1.5% on checkout — half what incumbents charge. This could drastically improve certain businesses’ profit margins: As a16z crypto’s @SamBroner has shown, for a very low margin business like a grocery store, a 1.5% improvement could potentially double net income. (And in a competitive, blockchain-based market, I would expect transaction fees to go much lower.) Unlike the old financial stack, which evolved in silos, stablecoins are global by default. They live on blockchains: open, programmable networks that anyone can build on. There’s no need to negotiate with dozens of banks across borders. You just plug into the network. People are already recognizing the advantages. In 2024, stablecoins moved $15.6 trillion in value, effectively matching Visa’s volume. While that figure mostly represents financial flows (versus retail payments), its magnitude still suggests we’re on the verge of a financial infrastructure shift, one that doesn’t rely on duct-taping 20th-century systems together. Instead, we can build something new, something truly internet-native — or what Stripe calls “room-temperature superconductors for financial services,” where rather than lossless energy transmission, you get lossless value transmission. The WhatsApp Moment for Money Stablecoins are our first real shot at doing for money what email did for communication: make it open, instant, and borderless. Consider the evolution of text messaging. Before apps like WhatsApp, sending a text across borders meant paying 30 cents per message. Even then, you were lucky if it actually got delivered. Then came internet-native messaging: instant, global, free. Payments are now where messaging was in 2008: Fragmented by borders. Burdened by middlemen. Gatekept by design. Stablecoins offer a clean-slate alternative. Instead of stitching together clunky, costly, and outdated systems, stablecoins flow seamlessly on top of global blockchains. These systems are programmable, composable, and designed to scale across borders. Already, stablecoins are slashing the cost of remittances: Sending $200 from the U.S. to Columbia using traditional methods will cost you $12.13; with stablecoins, it costs $0.01. (Fees to convert from stablecoins to local currencies can range from as high as 5% to as low as 0%, and prices continue to fall due to competition.) Just as WhatsApp disrupted costly international phone calls, blockchain payments and stablecoins are transforming global money transfers. Regulation: From Bottleneck to Breakthrough It’s tempting to frame regulation as an obstacle — but smart legislation is actually the unlock. Clear rules of the road for stablecoins and crypto market structure could finally allow these technologies to move out of the sandbox and toward widespread adoption. For years, decentralized finance (DeFi) was trapped in a kind of self-contained, circular, “crypto-for-crypto” economy. Not because the tools weren’t useful, but because regulators made it incredibly difficult to bridge into traditional financial systems. That’s changing. Policymakers are now actively shaping rules to recognize and regulate stablecoins in ways that maintain U.S. competitiveness, protect consumers, and allow innovation to flourish. Thoughtful regulation — like frameworks that differentiate network tokens from security tokens — can protect against bad actors while giving good actors the clarity they need to build. In fact, a forthcoming bill clarifying this regulation could pave the way for even broader adoption and integration into the global financial system. (Congress is hashing out the details as I write.) Building Public Goods for Everyone’s Benefit Traditional finance is built on private, closed networks. But the internet showed us the power of open protocols — like TCP/IP and email — to drive global coordination and innovation. Blockchains are the internet’s native financial layer. They combine the composability of public protocols with the economic strength of private enterprise. They are credibly neutral, auditable, and programmable. Add stablecoins on top and you get something we’ve never really had before: open money infrastructure. Think of it like a public highway system. Private companies can still build the vehicles, the businesses, the roadside attractions. But the roads themselves are neutral and open for everyone. Blockchain networks and stablecoins are doing more than just cutting fees. They’re enabling new categories of software: - Programmatic payments between machines: Imagine AI agent-powered marketplaces automatically brokering deals for computer resources and other services. - Micropayments for media, music, and AI contributions: Imagine setting a budget with some simple rules and leaving it to “smart” wallets to disburse the payments. - Transparent payouts with full audit trails: Imagine using these systems to track spending in government. - Global commerce without a mess of intermediaries: Imagine settling international transactions instantly at negligible cost — in fact, you don’t have to imagine it as it’s already happening. The moment for blockchain networks and stablecoins is now: Technology, market demand, and political will are lining up and making these applications a reality. A stablecoin bill could be on the floor this year, and regulatory agencies are weighing frameworks that finally align risk with the right oversight. In the same way that early internet startups were able to thrive once it was clear they wouldn’t be shut down by telcos or copyright lawyers, crypto is ready to cross the chasm from financial experiment to infrastructure backbone, with stablecoins leading the way. We don’t have to patch the old system. We can make a better one.

English

@magnet_mbb @Saylorsatsire just did, CA on base: 0x2B996cDa433F83B73C3519275D0061Ee1fd9adF0

English

@baaadkk @Saylorsatsire 🎉 Your memecoin is ready!

Name: Tired Of Winning

Symbol: TOW

Check on dashboard: mbb.magnetlabs.xyz/token/19092891…

Perform the first swap to finish your token deployment.

Dive in and make it yours!

English

Luke Fan | e/acc retweetledi

3/ Wave 1 of AI Agents Demo Showcase | Virtuals Demo Day 2025

@Luna_virtuals

@HeyTracyAI

@Vader_AI_

@Fuzzai_agent

@Magnet_mbb by @Magnetaixyz

@Byte__AI

@AcolytAI

youtu.be/8cweSDGrvq8

YouTube

English

Luke Fan | e/acc retweetledi

Most AI agents act on command. And now, they can reason via the intelligence layer.

Allora is coming to Magnet MCP Server, built by @magnetaixyz on @base, enabling the execution of smarter, more context-aware actions via Allora's predictive price feeds.

English

Luke Fan | e/acc retweetledi

@everythingempty @magnet_mbb recently introduced a super unique staking mechanism.

x.com/magnet_mbb/sta…

Meme Blind Box@magnet_mbb

💰 $MBB STAKING AND REVENUE SHARE IS LIVE! $MBB holders can now stake their $MBB to any of their favourite meme tokens and claim revenue from liquidity fees! 🔹 Stake at least 1000 $MBB 🔹 Earn your share of trading fees 🔹 Unstake anytime, no penalties 🔹 50% of LP fees to $MBB stakers Learn more about how $MBB transforms into your universal LP farming asset and collect your share of LP fees today! Learn more: mirror.xyz/magnetlabs.eth…

English

Luke Fan | e/acc retweetledi

We're excited to announce our collaboration with @AlloraNetwork!

By integrating Allora's prediction model with our Magnet MCP server, we're unlocking real-time, AI-powered crypto automation—helping users make faster, smarter on-chain decisions. 🧵

1/4

English

I usually don't share this kind of thing, but this is a nice, in-depth, off the beaten path overview of who I am and my journey to get here

i am grateful to be building alongside all of you

Samuel 🦤 (🧱,🔥)@samuellhuber

1/ Jesse Pollak is one of the most influential figures in crypto. But his story? It is far from ordinary: — Dropped out of college — Lived on $1700/month in SF — Delivered bagels for $35/week Here are 11 little-known facts about Jesse (aka the Base God): 👇 @jessepollak @base @buildonbase

English

《币安打法变化的背后~史诗级战略重构?》

早上写完上一篇,开车去搬砖路上重新梳理了一下思路,串联起各种事件,我觉得币安最近的战略大转向背后,是一套极具逻辑的破局打法。

币安背后有高人,不是简单的"抹茶化",听我慢慢道来。

找了个咖啡店开始码字,全文手机敲打,看了觉得有帮助的求不吝点赞评论转发。全文2000+字,值得花你5分钟阅读时间。

~~~~~~~

曾几何时,币安上币的标准极高,每一个新币都是一场“认知的财富盛宴”。但现在,上币频率明显加快,不仅通过 Alpha 频道、Launchpool、BN 钱包打新,甚至现货也连续上币,节奏大幅提升。与此同时,新币的整体市值也大幅缩水。

我一直在思考这背后的动因,目前能看到几个层面:

1.阿布扎比 20 亿对赌式投资的影响

币安获得阿布扎比成熟基金的大额投资,这类投资背后往往伴随“对赌条款”。而最关键的业绩指标无非两个:市场份额与潜在挣钱能力。

这笔钱不仅仅是资金补充,更是一种压力与承诺。在这样的背景下,加快上币节奏、覆盖不同层级用户,是极为务实的选择。

增量,增量!这才是金融秃鹫们最在乎的,不然怎么进一步吸引华尔街的老饕们?

所以能看到二圣打鸡血住在推特,能看到币安内部大调整,全员回归创业氛围,不能再躺平了。

2.链上新叙事的崛起倒逼 CEX 调整

上一轮 Meme Season 的爆发打破了“不上 CEX 就没机会”的宿命,而这背后很可能是 Solana Foundation 的战略布局:

抬高链上的天花板、削弱对 CEX 的依赖,从而掌控更大的主动权。

结果是币安原本主导的高端市场被侵蚀,而中下游用户则被链上项目和中小交易所吸走。

此外没有站队问题的中小所吃的满嘴流油,50个月的年终奖怎么来的?因为Binance没法早期上对家的项目,比如红极一时的 $Virtual 等,只能用合约蹭一下。

匆忙推出的Alpha事实上并没有挽回局面,甚至变成了对家的流量工具(Okx钱包开Alpha榜单)

3.高端定位陷入死局,币安需要破局

过去币安定位高端,导致它逐渐成为“最后一站”——一个项目如果最后才上币安,大家就觉得“已经是顶峰了”,于是散户成为接盘侠。内部上币组也变得束手束脚,担心砸了牌子。当时我曾建议搞个像 Alpha 这样的“二级板”,虽有帮助,但仍未解决主板预期过高的问题。

这个问题在本周期VC抱团哄抬物价后变得弱点极为明显,造成了币安口碑大幅恶化。VC币高估值加上上现货的溢价,已经达到了顶峰,新币全部暴跌,散户被割的奄奄一息,不得不做空自救。虽然没有看到具体数据,但我体感用户活跃度大减,散户财富流失严重。

4.现在的打法是主动降预期、重构市场秩序

币安选择大量频繁上币,就是主动把整个市场的预期和估值溢价打下来。预期降下来后,真正优质的项目才有机会在二级市场脱颖而出,不再是“币安保送”,而是让项目自己在市场中拼搏。

最近整治做市商,其实在一定程度上也是在整治项目方,别想着开盘爆割一把然后躺平。但有形的手效果终究是有限的,是下乘,用市场调节市场才是正途。

二级上线估值下降,项目方养蛊式竞争,辅以积极下架机制,散户也因此有更大的上涨空间,这比“高溢价上线直接破发”要健康得多。

5.全面调动上下游,构建闭环生态

币安如今通过 Alpha ,钱包打新,上合约和上现货已经开始成功构建生态闭环。

顶层的投资机构( @yzilabs Lab)其实过去有大量的投资项目并没能获得币安自己的上线,毕竟坑位有限。

曾经辉煌又被冷落的 @BNBCHAINZH 需要中兴,需要热点,更需要来自币安的支持,这是与Solana抗衡的最大依仗。

钱包 @BinanceWallet 更加需要独家资源扶持,这是未来的船票,也是币安最容易吹大估值的地方,不可能放弃。 但对比Okx钱包起步晚,资源少,现在不停送钱打新就有点当年滴滴大战时候一样,对比战略收益,送你们100个Ido都是小钱。

这样投资,Cex用户,项目,底层的链上资产,形成了完整的流量闭环。散户用自家钱包打新,直接从交易所买链上的 Alpha 热点,打造了一个可以源源不断制造热点的流量机器。中小交易所要在这个生态下生存,难度会越来越大。

6.币安正在用极高代价完成“抹茶化”

币安实际上是在主动承受“抹茶化”的骂名:降低门槛、稀释溢价、频繁上币。但它换来的是一个真实且去中心化的市场竞争机制。

项目不再“保送即巅峰”,而是要靠做事、靠社区、靠 street smart 在二级市场竞争。对散户而言,这也是一种更公平的造富路径。

~~~~~~

这不是一个动作,而是一整套连贯打法。从破局到下沉,从去中心到重构秩序,币安正在完成一次历史级的自我重构。

文中都是我自己的思考,可能有些地方有偏颇,欢迎 @cz_binance @heyibinance 点评。

土澳大狮兄BroLeon | 🔶BNB |@BroLeon

《币安,战略思路已经发生了巨大变化》 跳预言家了,不好意思 睡醒币安投票上币结果出来了,前面的预测基本都一致,上4个,且4个中3,掌声在哪里? 唯一比较遗憾的是 $TUT ,这个币啥背景的确我不了解,因为出来前后我那段时间没关注币圈。不过错过就错过吧,总有点遗憾。 这次针对投票的操作基本结束,吃到了 $Banana $Siren 最肥的一段,$Mubarak 几次波段,西蓝花listing的一段, 刚才起床把大部分仓位都清了,阶段性目标达成,后续博弈的不可预测性就大很多,先缓缓。 看到很多人不理解投票上4个,其实我觉得基本上我的推测就是正确的: 从打通Alpha购买渠道开始,币安已经放弃了高高端起的姿态,降低了合约/现货门槛,全面下沉争夺别家份额。 币安,战略思路已经发生了巨大变化 先说一下当前的感觉: 1、未来币安listing 现货的估值预期要降低,不能再简单参考之前的门槛,因为已经进入了后现货时代,刻舟求剑会死人的。 2、币安当前这种机关枪可能会继续,大家要适应一下。凭啥只能小所叭叭叭的上项目?币安等着跑出来再吃屁?Alpha+合约+现货+打新,全方位覆盖从meme到小项目到天王的全部频段。 走自己的路,让其它中小所们无路可走,压力会山大。(利空,其它所的平台币我都暂时先清掉了,看看情况) 3、指望币安下场扶持头部meme,够呛 从目前情况看,再出现小写狗那种炸裂的爆发很难了,标的开始分散,资金也分散。而白头巾Mubarak上了现货非但没有趁机上去一波,还直接利好落地被砸了一顿。市场一直期盼的500M / 1B 的Bnbchain meme标的现在看起来是越来越远了。 暂时我先不对这个预期下注了,继续小资金压新标的挺好的,就像昨天B家的吉卜力。 4、 $BNB 赋能增大,币价能不能被托上去? 现在明眼人都可以看到币安叠加在 $BNB 上的权益越来越大且越来越重,这是好事,不然 BNB/BTC 的对子不会那么坚挺,早该跌下500去了。从 BNB/SOL BNB/ETH 能看的更加清楚。 最近持有 $BNB 就是天天躺着被喂饭,相信会有更多人选择长期持有而不再是打新前临时交易或者去借贷。如果 BTC 能往上突破, $BNB 按理说应该是基本面最好的币之一。 所以,这次币安的战略调整和战略目标,你看懂了吗?纷纷扰扰的出招背后,我就看到了几个字: 抢回份额 + 拉升 $BNB

中文

One more thing, @OpenAI has already joined the game. We're keeping our heads down and building.

We're betting on the huge potential of MCP and will continue contributing to the ecosystem.

source: x.com/sama/status/19…

5/5

Sam Altman@sama

people love MCP and we are excited to add support across our products. available today in the agents SDK and support for chatgpt desktop app + responses api coming soon!

English

Several working MCP servers, including one that works with @base and @CoinbaseDev MPC wallet SDK: github.com/magnetai/mcp-f…

4/5

English

We've been working on @AnthropicAI MCP since last Nov, and it's great to see the big growth coming soon. Here's what we've built for the MCP world:

1/5) 🧵

Magnet Labs@magnetaixyz

2025 is here, and wow, it’s already feeling like a game-changer for AI + crypto. Although the year has just begun, we're already pushing boundaries across three core initiatives. Consider this our New Year's gift to the Magnet Fam! Key highlights from our 2025 roadmap below! 👇 1. Big Moves in Product Innovation Get ready for MBB 2.0, the second version of our AI Agent Meme Blind Box, and it’s next-level. This update is about to completely transform your meme experience 🎉 Also, Magnet is taking it up a notch in 2025 by integrating Claude MCP + Base Network to create an AI Agent Freelance platform powered by Base’s global payment network! This includes: - Pioneering monetization methods for the MCP ecosystem through global micropayments and a tokenized Creator Hub for Claude MCP - A marketplace for MCP crypto servers and services - Building Magnet Desktop, an open-source MCP server manager built on Claude MCP. 👉github.com/magnetai/magne… 2. Doubling Down on @base 🔵 We've joined forces with @OurTinTinLand! This groundbreaking initiative unites key APAC partners to accelerate Base's presence in the region. Onboarding the next wave of devs + users to Base! 3. Pushing the Claude MCP Ecosystem Forward Claude MCP is open-source, and we’ve been here since Day 1. Our focus: - Curating the Awesome MCP Crypto List - Developing Magnet Desktop for anyone to access MCP servers - Founding the MCP Crypto Alliance to push the boundaries between Crypto and the MCP ecosystem Want to help shape the future of MCP + crypto? Our DMs are open! 2025 is going to be HUGE for Magnet. Our focus is clear: simple, powerful tools for the Base Network & Claude MCP. The AI + crypto revolution is just starting—and we’re here for it. Keep building. Stay based. Let’s go. 🙌 mirror.xyz/magnetlabs.eth…

English

Luke Fan | e/acc retweetledi

people love MCP and we are excited to add support across our products.

available today in the agents SDK and support for chatgpt desktop app + responses api coming soon!

English

Luke Fan | e/acc retweetledi

Introducing Claude USDC Transfer: The @AnthropicAI native way for FREE transferring on @base, powered by @CoinbaseDev MPC wallet and @magnetaixyz protocol.

This is just the start of LLM extensions - with Magnet, everything gets easier - web2, web3, you name it!

English