bbqrice

116 posts

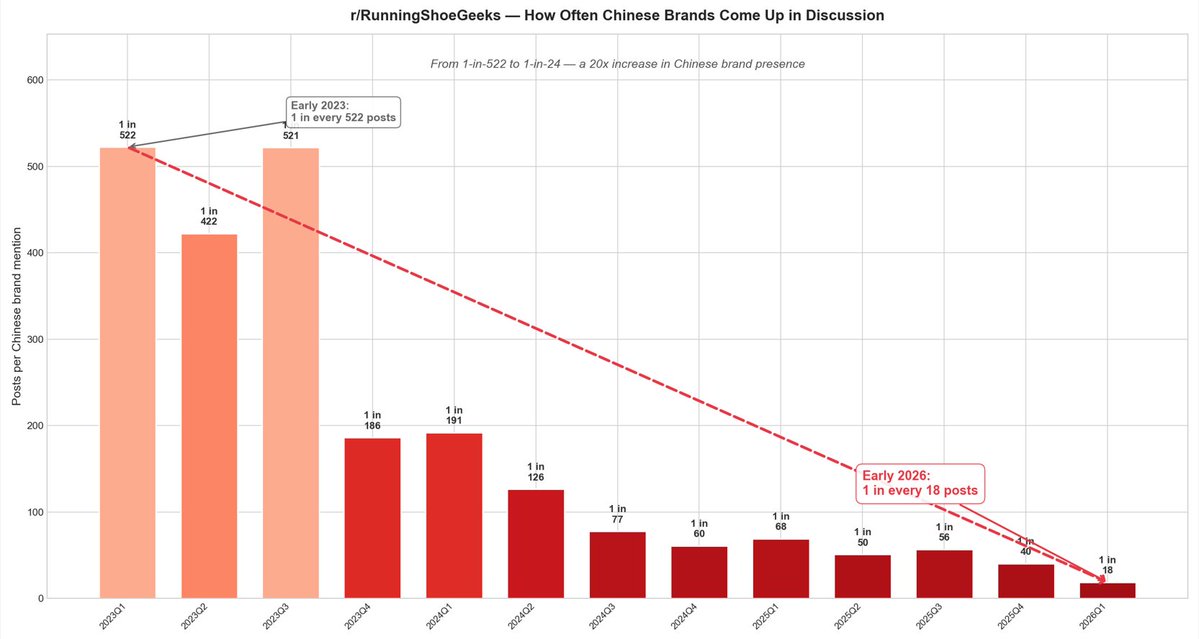

On r/runningshoegeeks, 1-out-of-18 posts mention a major Chinese running shoe brand. Just last quarter it was 1/40. Li Ning is the big one

English

FT should stick to news, and not acting smart.

Nicholas Guyatt@NicholasGuyatt

The FT now reporting that, even without the energy shocks, there's a pretty good chance that the closure of Hormuz will pop the AI bubble and lead to a stock market crash

English

@LukeRDavis @ModeledBehavior It’s less about the data and more about the aesthetics of the time series charts.

English

@bbqrice @ModeledBehavior ElectionBettingOdds volume averages from those *as a minimum*.

English

Who wrote the “from ‘I, Pencil’ to ‘1 Pencil’ “ tweet last year - was it @wwwojtekk ? Or @ATabarrok ?

English

@dalibali2 The first best time to pull the trigger was 3.5 years ago. The second best time is now.

English

English

@bbqrice @ptuomov @RyanMGavin @JasonLiebel Yes. But now I'm wondering how other people are talking about "volatility drag".

English

@choffstein @ptuomov @RyanMGavin @JasonLiebel Whatever you like, as long as you understand that the almost sure long run growth rate (your expression) is not the same as an expected return.

English

@ptuomov @bbqrice @RyanMGavin @JasonLiebel Let me offer a counter-point.

If we assume your wealth follows a geometric brownian motion, as T→♾️ your wealth approaches exp(μ - σ^2/2).

What else are we going to call that -σ^2/2 term?

returnstacked.com/volatility-is-…

English

@__paleologo Everyone can pick stocks, risk management is literally what matters lol

English

Oftentimes, I read from retail traders dismissive comments about risk manage(ment|rs). Risk management is the most useful skill you can learn when trading on your PA or managing a $3b book (and it’s learnable). And a good Chief Risk Officer is the 2nd most important and useful person in a top hedge fund. I know, it’s obvious. But in years like this, a good self-reminder.

English

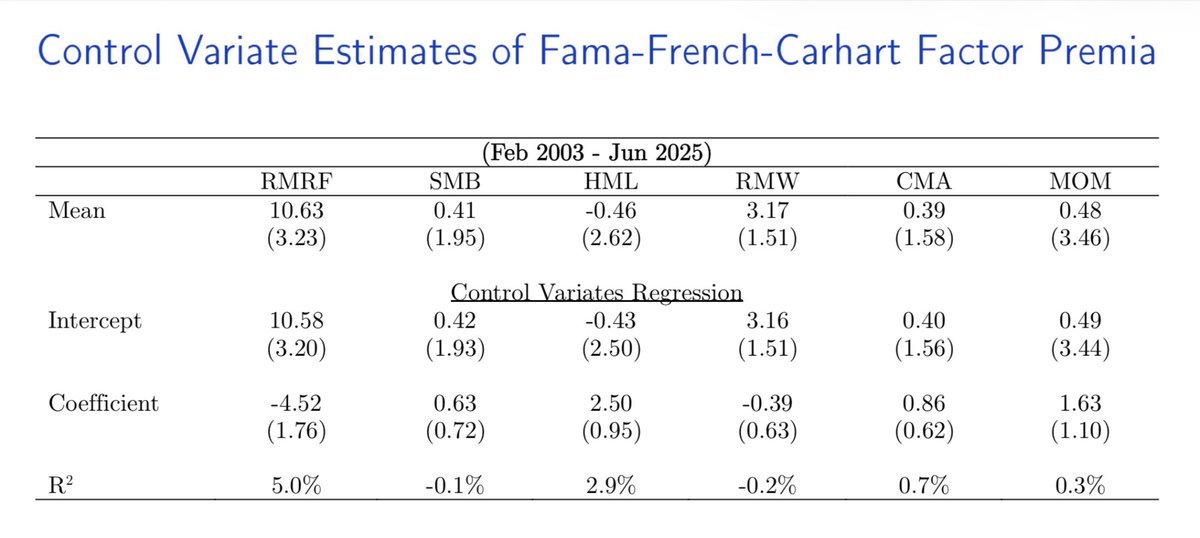

The bottom panel is the control variates technique regression applied to factor premia. The idea is that if you can find a stationary variable (such as 10 year inflation indexed bond yield) and its changes are correlated with the factor premium you’re trying to estimate, then you may get a statistically less noisy estimate of the mean.

The first row is the sample mean factor premia. This can be compared to the intercept row of the CV panel.

English

@iaindunning I prefer "Imagine that you are Leonard from Memento, and you have lost your memory. The last Leonard wrote this down for you"

English

How do you talk to Claude? Say, when using Claude Code, at the end of a session you asked it to write its learnings in a text file. In a new session:

A: "a previous claude wrote this summary, read it"

B: "you previously wrote this summary, read it"

English

Lloyd Blankfein quit being the CEO of Goldman Sachs and instead of taking some cushy board job or going into politics he sits in front a screen all day and trades his PA

absolute sicko behavior

Joe Weisenthal@TheStalwart

NEW ODD LOTS: Why @lloydblankfein hardly ever tweets @tracyalloway and I talk to the former Goldman Sachs CEO about life in retirement and how his risk management background helps him resist the impulse to post podcasts.apple.com/us/podcast/odd…

English

@SowingAlphaSeed There’s nothing about modern portfolio theory that requires fixed assumptions about future returns.

English

Modern portfolio theory works out the math on why rebalancing investments improves risk adjusted returns. But it does so mostly using fixed assumptions on the future returns of each investment. The math can be much more favorable if you have fluid beliefs about expected returns.

Myles@finphysnerd

My 2x ETF arbs really helping out today. Have been able to trim them (which have been fine over the last week) and buy stuff I want to buy.

English

@FICMBondTrader Tbf we’re approaching the end of summer 27 recruiting.

English

I got a LinkedIn update of someone accepting a

“2027 GS summer analyst role”

What? It’s fucking March 2026.

I remember back in the day you could just shake hands and show up a couple months before.

If you don’t have parents/school in the know, you are fucked.

English

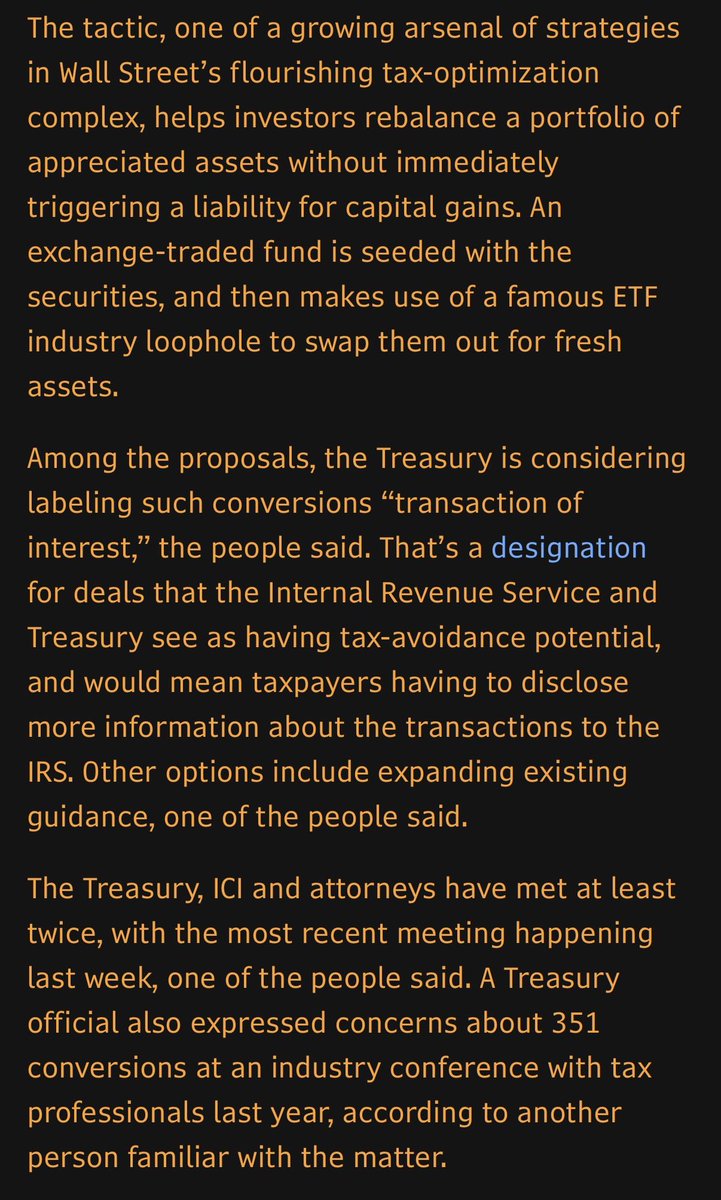

bbqrice retweetledi

SCOOP with @denitsa_tsekova and @VildanaHajric: US Treasury is looking to tighten scrutiny of 351 conversions into ETFs -- which effectively look to cut tax bills by seeding ETFs

Treasury is considering labeling these as a "transaction of interest," which is for deals with tax avoidance potential

English