bhushan patil

129 posts

bhushan patil

@bhushan2000

Helping digitize India with exp from alibaba, paytm, yahoo n more... Stitching ideas, tech, people and money...

India Katılım Mart 2009

67 Takip Edilen191 Takipçiler

For all of India, for all the work we’ve put over years and years. There are no words, there are only emotions! Love this team, love playing for my country! No greater joy than winning for my country! Champions of the world 🇮🇳🇮🇳🇮🇳🏆🏆 Jai Hind!

English

𝗖.𝗛.𝗔.𝗠.𝗣.𝗜.𝗢.𝗡.𝗦 🏆

#TeamIndia 🇮🇳 HAVE DONE IT! 🔝👏

ICC Men's T20 World Cup 2024 Champions 😍

#T20WorldCup | #SAvIND

English

A small weekend tribute dedicated to the #teamindia

#T20 #Worldcup #Cricket

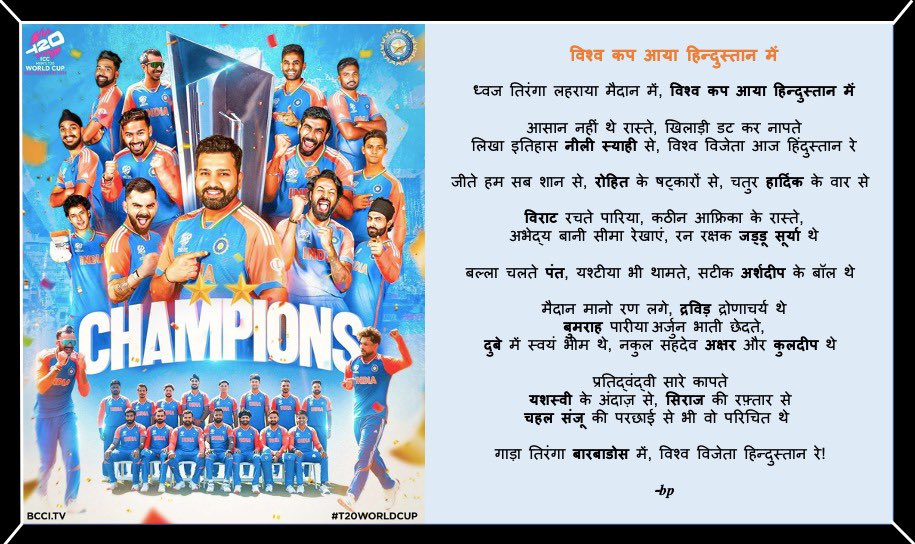

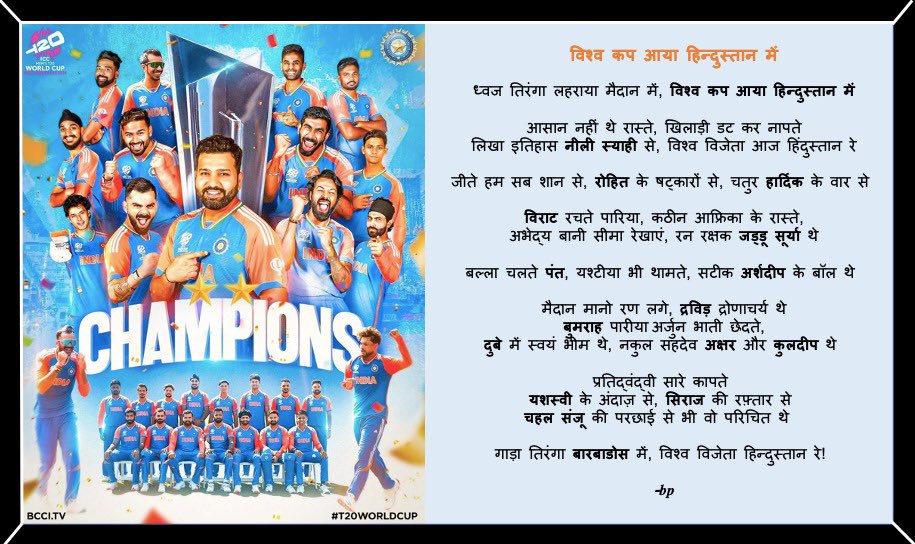

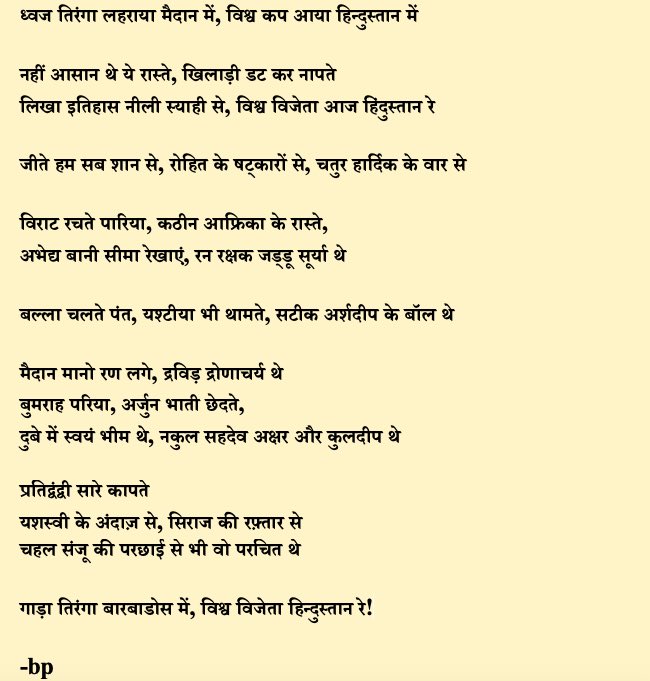

ध्वज तिरंगा लहराया मैदान में, विश्व कप आया हिन्दुस्तान में,

नहीं आसान थे ये रास्ते, खिलाड़ी डट कर नापते

लिखा इतिहास नीली स्याही से, विश्व विजेता आज हिंदुस्तान रे, ….

….

हिन्दी

@PMOIndia @narendramodi twitter.com/energiabuyers/…

@CMofKarnataka @DKShivakumar @INCIndia @INCKarnataka

Mantri Energia Buyers Association@energiabuyers

#Unjustice #homebuyers #RERA #Modi @narendramodi Modi sir waiting for your response !!! @PMOIndia @CMofKarnataka @BSBommai @KA_HomeBuyers @FightforReraKar @amitshah @moneycontrolcom @DatSouptik

QME

हमारी सरकार मिडिल क्लास परिवारों के घर का सपना पूरा करने में भी हर संभव मदद कर रही है: PM @narendramodi

हिन्दी

@BeingPractical While challenges there are fundamentally some USPs of money and opprtunties it offers. If one understand these there are interesting business models around it. Happy to chat more 1x1. And i do feel we in India are yet just scratching surface and yet to cover the entire spectrum.

English

Have a very different view, most VC investors in India don't get Fintech and specially the ones who claim to lead it. It's plain and simple, folks insist on making it complicated.

F&O is very small opportunity, with less than 1.5-2 Mn active traders. One of fintechs, in this domain has retention rate of 10% in less than <90 days. Know other two who have lost 90% of userbase in 24 months

SBI alone does 25,000 Cr EBDITA in single quarter. SBI quarterly revenue is 3X of Capital Markets revenue pool.

Lending is 'the opportunity' of India, which unfortunately handful of fintechs (very small) have been able to crack and still very nascent to call it even an early success.

Financial Services, if someone has to crack it - need patience of decades. VCs, Investors and Founders (me included) can only come up with paper unicorn valuations in 7 years, all that will get ripped on listing day on public markets.

Vaibhav Domkundwar@vaibhavbetter

🇮🇳 Fintech is dead. Long live 🇮🇳 Fintech. Globally, everyone in Fintech is wondering how to figure out profitable venture scale growth to justify their valuations which are falling fast. 🇮🇳 India is no different unless you are in denial and in fact, Fintech in India has bigger problems around profitable monetization -- add the regulatory updates to this & you have an even greater challenge to brave. Besides F&O, where there seems to be a clear profit pool as demonstrated by multiple companies, the rest of fintech is simply a hard and long journey - it all boils down to making money from lending followed by tiny amounts of money from payments, insurance, investments and the likes where you are a middleman shaving off a small slice for yourself. Billions of dollars have been spent over the past decade for us to collectively arrive at this conclusion so it may be best to take the lessons learnt & conclusions concluded and build forward. The good part is that we have a large TAM that is made of multiple sub-markets each of them having 10s of millions of users potentially - some have these already, some will get to this over time. So what we are seeing is that the best teams are figuring out and sticking to one core wedge: a neobank, a credit card, a UPI app, a SaaS app, a gold investment app, a alt investment app, a vertical offering for fleet owners or infuencers etc. They use the core wedge to get to millions of users (some have the capital to go faster, some don't have as much capital so they are hacking channels one by one and getting there slowly but surely) and then expand from the core to sell their users all the other financial services offerings that are relevant and are personalized for their slice of the TAM. ( I am leaving the broking folks aside as they have the beauty of F&O to constantly give them a cushion to build the rest on and the overall push to invest in mutual funds etc gives them a good tide to ride on.) With capital markets unlikely to look anything like they did in the ZIRP era, as an early-stage fintech founder (Seed to Series B), you have to re-underwrite your own vision, conviction, and determination and be clear that it's at least a 5+ year journey from here to build a sustainable business --- many have gone through this over the past 18 months and many others are in the process. Its hard because you have to overhaul everything you thought about your plan in the 2020-2022 timeframe. Those in growth stage (Series B & beyond) have the capital but potentially an even harder problem to solve because they have to go FROM the model of burning 100s of millions to make 1s or 10s of millions TO burning far lesser while making far more. The key is to not forget the lessons learned - easier said than done :) So the problems are hard and harder BUT those with revised conviction after all the mayhem are more determined than ever, based on what we are seeing. So, Long live 🇮🇳 Fintech. 💪

English

@fintechjunkie I’d call it as unfolding- story, value, markets, customers and growth levers over time

English

Each step of the journey is equivalent to reading another chapter in a book that’s still being written.

And a Venture Capitalist reserves the right to evaluate future investment decisions based on how much they like the story so far and what the author says is coming soon.

English

There’s a major structural flaw in how the VC ecosystem works that we don’t talk about enough.

It’s a flaw that creates confusion and bad advice for Founders.

And it’s a flaw that makes no sense when you dissect it. 🧵👇

English

@_ShankarNath OTP - "Online Transaction Pain" :) this is a stress booster in many people's life.

English

Congratulations! @nova benefits , @QubeHealthCare

Today most need insurance, credit, health, & related benefits all at one place. The duo gets you the same.!

buff.ly/3Au1F6R

English

What do you mean by following -

यारो - वीकेंड पे झूमते हैं

और कितना झूमेंगे? अब बस !

This is nothing but -

- Let's meet on Zoom on weekend

- How much time will spend on zoom, enough!

😀

Any such new digital hin-glish stuff?

:) #zoomcall #zoommeeting

English

@elonmusk While recently - it's marked as endangered on earth :)

English

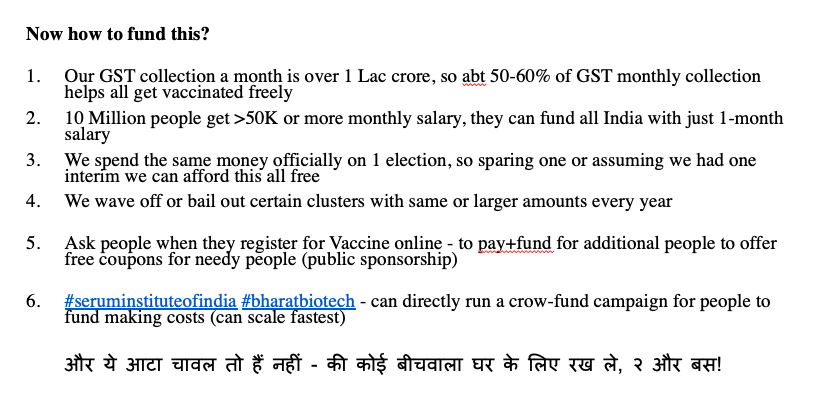

Can we have free vaccination for all in India? - I guess Yes!

Here's the Math -

For mass - approx.500Rs for 2 shots, for billion people it's about 50,000 Crore. (with 1.3B it's abt 65,000 Cr)

#pmoindia #indiafightscovid19 #seruminstitute #BharatBiotech

English

Congrats Team Ally! Awaiting more #Bollywood #Tollywood flix...

CACZero@theallyIndia

Streaming now!! Book your tickets and watch at mm.the-ally.com @rajinikanth @RajiniFC @RajiniFollowers @Rajni_FC @rajinikanfh @rajinikanfh @ksrfablr @Rajini_F_C @RajinikanthFan6 @rajinikanthpage @TamilrajiniM @TeluguRajiniFC @sathyamovies @iam_RAJINI @RajinikanthFan_

English

Interesting equations to be seen for the Chinese apps doing well in US, Europe and then extending to India. What may further be interesting is few Indian businesses buying India parts & setting locally. Wait n watch

English

bhushan patil retweetledi

kudos to the designer for creating such a visual representation.

This is what I'd call #productThinking (PS: I have no idea how accurate this is)

Sanjay Swamy (theswamy)@TheSwamy

#BestTestYet How good is this?

English

Been 100% digital to 99.9% of the world for 40% of the year. #COVID19karnataka #CoronaInIndia #lockdownindia

English

;)

I have a seminar joke, but we are on webinar …

I have a login joke inside, but forgot password

Have a joke on black money, but now am salaried

I have joke on the box am part of, but am Intel …

I have joke of tomorrow, n can tell day after

Vijay Shekhar Sharma@vijayshekhar

I have a joke on Zoom, but I will tell you on Team.

English