Sabitlenmiş Tweet

BitBrew

14.6K posts

BitBrew

@BitBrew1

BitBrew is where decentralization of money meets the automation of intelligence. Join me on my journey through the bits of our universe, one bean at a time. ☕️

The Singularity Katılım Şubat 2024

203 Takip Edilen1.2K Takipçiler

@Kaanesrabiebs @d_1awrence Not sentiment. Capital moves depending on how rates how moving across the curve. The good thing is that we’re pretty much in negative real rate territory where CPI is above Fed funds and that is best for Bitcoin as the cost of capital is now higher.

English

@BitBrew1 @d_1awrence makes sense, market sentiment really drives crypto moves these days

English

I have to be honest....

After all the positive news this week with the Clarity Act mark up being approved, Strive announcing that $SATA is paying daily dividends, $STRC producing enough volume to buy at least 10,000 BTC PLUS $MSTR settling $1.5B of their convertible debt, I expected to see a better reaction to Bitcoin than being DOWN 4% in the last 5 days.

It literally makes no sense. Like, how did we reach $126k when there wasn't half the bullish news there is today?

I understand there were mass OG sellers last year.

I understand Jane Street was manipulating the price for months.

I also understand there's a war in Iran.

What I dont understand is how a company like Intel is up 700% since the US government put a few quid into it and SpaceX is preparing to IPO at a higher valuation than the entire Bitcoin network, yet Bitcoin, as a global monetary asset that's having billions of inflows, is still 40% off it's all time high and 10% down YTD?

Even Nvidia, who has a $5.4T market cap, almost 3.5x Bitcoins market cap, has moved 20%+ higher in 2026 despite all the macro-economic challenges.

I don't know what it is - I said last year that someone was manipulating the price & it turned out to be Jane Street.

It still feels off.

It'll come out eventually. I don't know why, but Bitcoin should be FAR higher than it is right now.

It will revert at some point. I'm convinced of it.

Until then, I'll continue to be perplexed by the price action but grateful I'm able to keep stacking at these lower levels. 🧡

English

@VeChainBTC A 5% dip over a two day span? What good analysis you have sir. Higher still.

English

S&P is doing this…

Bitcoin about to BOOM.

It’s being held down by shorts but it’s a ticking time bomb.

Ben Cowen funeral incoming.

The Kobeissi Letter@KobeissiLetter

BREAKING: The S&P 500 officially hits 7,500 for the first time in history, now up +19% since the March 30th bottom. That's +$10.9 TRILLION in market cap in 7 weeks. This truly is one of the best runs ever seen.

English

BitBrew retweetledi

THE JAPAN TRADE. weekend reading

Everyone's seeing the charts on their feed: JGBs hitting record yields. Yen >158. US 10Y >4.5%.

But do you understand what it actually means, and why it’s important?

I’m going to break it down here, and explain the implications and how it relates to Japan, the US, Bitcoin and #Metaplanet. Because believe it or not, Japan is probably the most important macro story in the world

1/ The data. JGB 10Y at 2.7% — highest since May 1997 (29 years). JGB 30Y at 4.00% — all-time record. JGB 40Y above 4% — first time any JGB maturity has been here in 30+ years. USD/JPY around 158, with the BOJ spending ¥5.48T ($35B) on intervention this month alone. This is not pocket change, and had little to no effect besides a short term bounce.

2/ But this isn't 1997. Look at the JGB 10Y chart (posted below). The yield is back where it last was in May 1997 — 2.70%. The country however, is not. In 1997, Japan's debt-to-GDP was ~100%. Today it's 248%. So it’s the same nominal yield, applied to a debt stack roughly 2.5x larger. Today's reported interest bill (¥13T) is still mild because most outstanding JGBs carry sub-1% coupons issued during the ZIRP/QE era — but every bond that rolls now reprices to today's curve.

3/ Which sets up an impossible trilemma. Three things Japan is trying to do at the same time: (a) keep debt service affordable, (b) prevent the yen from collapsing, (c) let rates normalize to reflect actual inflation. You can only pick two out of three.

— Pick (a)+(b): keep BOJ buying bonds to suppress yields, burn FX reserves to defend the yen. This is the path that got Japan to 46% BOJ ownership of JGBs and ¥5.48T of intervention in a single month. Every quarter the exit gets harder.

— Pick (b)+(c): let BOJ hike to close the US spread, yen stabilizes. But every 100bps higher reprices a ¥1,300T+ debt stack on rollover. Fiscal crisis looming.

— Pick (a)+(c): hike slowly, keep fiscal stimulus, let yen find its level. Yen drifts to 170, 180. Imported inflation crushes consumers. Foreign capital starts selling JGBs. Fiscal crisis through a different door. The trap is circular: every solution produces the problem you tried to avoid. That's why this isn't a riddle you can solve. It’s a can you keep kicking down the road, until the market eventually forces a choice.

4/ Then PM Takaichi said the quiet part out loud. She said "break free of the spell of excessive fiscal austerity." Her plan: ¥21.3T supplementary stimulus, a ¥122.3T FY26 budget (biggest ever, +6.3%), tax cuts and record defense spending. And the bond market is responding.

5/ The fiscal math doesn't work anymore. Interest spending in FY26: ¥13 trillion — about 10.6% of the entire ¥122.3T budget. Total debt service (interest + principal redemption): ¥31.3T, roughly one-quarter of the budget. Japan now spends about ¥1 of every ¥10 of its budget just on interest, before a yen is allocated to defense, healthcare, or anything else.

Sensitivity: every 1% rise in yields adds ~¥3–4T to annual interest cost in the near term as JGBs roll (MOF rule of thumb). Over a decade of full repricing across the ¥1,300T+ debt stack, it adds ~¥13T — effectively doubling today's interest bill.

The budget already had to bump its assumed bond rate from 2.0% (FY25) to 3.0% (FY26). The 30Y is currently quoting 4.00%.

6/ The BOJ wants to hike. It can't move fast. Policy rate is 0.75% (still negative in real terms). Core CPI forecast for FY26 is 2.5–3.0%. April PPI: +4.9% YoY and accelerating. Three board members already dissented for 1.0%. But every hike makes the fiscal hole deeper. They're trapped between inflation and insolvency.

7/ Which is why the yen keeps falling. US 10Y: 4.57%. JGB 10Y: 2.7%. Spread: ~190bps. As long as that gap exists and the Fed isn't cutting, the yen wants to weaken. Tokyo's ¥5.48T intervention may have bought them a few weeks, but it didn’t fix anything.

8/ Now the global piece — the carry trade. For a decade-plus, the world borrowed yen at ~0% to buy higher-yielding assets globally. Estimated notional: $350–500B+. As JGB yields rise and yen funding gets expensive, that trade unwinds. Japanese capital comes home. Foreign assets get sold. The biggest one: US Treasuries.

9/ That's why US 10Y just crossed 4.5%+. It's not only US inflation. It's the marginal Japanese buyer becoming a marginal seller. Japan holds ~$1.1T in US Treasuries — the largest foreign holder. If even 5% repatriates, that's ~$55B of supply hitting an already-fragile market.

10/ The deeper story is debasement. Japan printed ¥700T+ over the last decade. The BOJ balance sheet is now ~130% of GDP. They finally got the inflation they worked so hard for. The cost: yen debasement, a bond market revolt, and a central bank that owns half its own debt. There is no clean exit.

11/ Bitcoin is the hedge against exactly this. Debt monetization that can't be reversed. Currency as the release valve. Bond markets that have stopped trusting central planners. BTC corrected with bonds this week on the risk-off — but the structural reason it exists just became clearer.

12/ So the real question. Not "who owns BTC." Not "who's Japan-listed." Which balance sheet is actually built for this regime — capital structure designed for a debasing yen, a rising US 10Y, and a global capital pool that's starved for real yield? I think you can guess who that is.

13/ Metaplanet is the bridge architecture. Metaplanet ($MPJPY / $MTPLF / $3350.T) is the only treasury company designed to bridge three pools: a Tokyo-listed parent equity, US institutional appetite (the deepest BTC-proxy demand pool in the world), and Japanese yield-starved capital. Into one ecosystem. It’s a structural setup @gerovich and @DylanLeClair have been quietly putting together, while the market is too focused on the short term price action.

14/ The Japan engine is already running. 40,177 BTC on the balance sheet; the largest holder outside the US and third largest globally -> likely to jump to second by end of Q2. Perpetual preferred shares being built from scratch as a first time innovation with extremely high barriers to entry, albeit exact timeline is uncertain.

15/ The US engine is being built right now. I laid out the full chronology in detail in my last post. The short version: this didn't start last week. Apr 2025: Miami subsidiary established. Sep 2025: US Income Corp (BTC income generation, US jurisdiction). Dec 2025: Sponsored Level 1 ADR live ($MPJPY), Deutsche Bank depositary, MUFG custodian. Mar 2026: strategic-disclosure day — Asset Management + Ventures + JPYC investment, all on the same day. Thirteen months of compounding setup.

16/ The fee-waiver is the tell. Metaplanet opened a 60-day fee-free window for converting $MTPLF → $MPJPY ADRs, running April 13 to June 12, 2026. Translation: management wants the ADR float deep, clean, and institutionally ready before something lands on top of it.

17/ The likely product — and why it fits the macro. The most plausible first product is a USD-denominated perpetual preferred, run on the same 144A playbook Strategy used for $STRC / $STRD / $STRF. And the macro story is exactly what makes the two-pool structure powerful: Japan is yield-starved (a 5–6% coupon clears domestically), the US is yield-rich (BTC-treasury perps already clear at 10–14%). Metaplanet can issue into both worlds at their respective rates, building optionality and taking advantage of the two deepest capital pools in the world as they evolve over the coming years.

18/ No other company has this structural setup. A debasing-currency balance sheet, holding the asset that hedges debasement, raising in the world's deepest dollar capital market — while its home market produces the structural tailwind.

19/ What this means for the US and Bitcoin. For the US: Japan is the leading edge, not the exception. US debt-to-GDP is ~125%, the 10Y is 4.59% — the same arithmetic eventually applies. Higher rates → higher debt service → political pressure on the Fed → yield curve control, dollar debasement, or both. The US is roughly 10–15 years behind Japan on the same curve. Japanese repatriation is one of the reasons that curve is being pulled forward right now.

For the dollar: short-term strength as the yen weakens further. But every reserve currency with high debt-to-GDP and aging demographics ends up where Japan is. The dollar's privileged reserve currency status buys time, but we are already seeing this start to unwind.

For Bitcoin: BTC is the only macro asset whose supply is fixed regardless of what any central bank decides. When bond markets stop trusting central planners — and the JGB curve is the first to break that trust at scale — Bitcoin's value proposition stops being abstract.

Short-term, BTC trades with risk-on/risk-off. It sold with bonds this week. But the structural bid keeps building: corporate treasuries, sovereign accumulation, capital fleeing fiscally-trapped currencies. Each Japan-style episode makes Bitcoin's reason for existing more obvious, not less.

English

BitBrew retweetledi

“Tonight, at my direction, brave American forces and the Armed Forces of Nigeria flawlessly executed a meticulously planned and very complex mission to eliminate the most active terrorist in the world from the battlefield. Abu-Bilal al-Minuki, second in command of ISIS…” - President Trump

English

BitBrew retweetledi

BitBrew retweetledi

The feeling when you print 40% of all dollars in existence and your term ends before the bubble pops.

English

BitBrew retweetledi

Whoever designed this needs to be fired immediately:

English

BitBrew retweetledi

BREAKING: SpaceX is planning to debut its record-setting IPO as soon as June 12th and has packed the Nasdaq as its listing venue, per Reuters.

SpaceX has accelerated its IPO timeline and is now aiming to flip its prospectus public as early as next Wednesday.

English

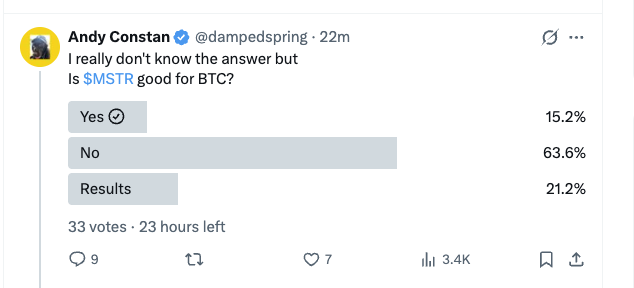

@STRC_live is guessing around 15k BTC and @BTCtreasuries is guessing around 24k.

Considering they used 1.5B to pay off some of the convert, we shouldn’t see the full amount.

Let’s see who is the closest.

English

@hillery_dan Most people don’t know jack shit about anything so polls really don’t matter on stuff like this.

English

BitBrew retweetledi

Strive is a structured finance company and institutional asset manager focused on disciplined capital allocation and long-term value creation.

Proud to celebrate $ASST! #NasdaqListed

English

Say it with me.

DE

VAL

U

ATION

Parker Lewis@parkeralewis

This is a regime change. Seriously doubt the BOJ, Fed, ECB, et al can unring the bell. If you invested in these bonds, took a bath and finally sold out realizing losses, it's one of those fool me once, shame on you. Fool me twice, shame on me kind of things. "Break the glass".

English

$SATA is printing and $ASST is down.

Let’s do a thought experiment.

$SATA keeps printing but the common doesn’t.

Obviously this could lead to higher amplification and even too high to the point where it hurts the credit and $SATA stops trading at par.

Strive has a couple options to delever.

1. Sell equity if it’s at a premium

2. Sell Bitcoin if equity is at 1 mnav and buy back common

3. Sell equity even when equity is at 1mnav if they don’t want to sell Bitcoin

The first 2 seem obvious.

Let’s break down number 3.

Selling Bitcoin actually leverages up the balance sheet and the delevering part would be purchasing common.

The issue is that it may not work to solve the issue at play here which is that amplification is too high.

In this scenario, I would be all for them selling common to acquire more Bitcoin to expand the balance sheet at 1 mnav or even slightly below EVEN IF ITS BTC YIELD NEGATIVE.

Why?

Because of the credit quality.

Saylor said that they have to balance the needs for positive BTC yield and the credit quality.

Expanding the balance sheet at less than 1 mnav is BTC yield negative BUT…

If it allows $SATA to keep printing and reinforcing the flywheel, it’s actually BTC yield POSITIVE on the back end.

Essentially the dilution of the common would be made up by $SATA continuing to trade at par and provide BTC yield.

The flywheel is unstoppable as long as the common has ample liquidity and the common will have ample liquidity as long as the credit quality is good because it reinforces the strength of the underlying business.

English

BitBrew retweetledi

BitBrew retweetledi

@BitStrategy21 Friends? No.

Mutual beneficial entities? Yes.

Just look at the AI space.

They’re all feeding off each other.

English

It is not possible for companies to be ‘friends’ with other companies.

A company is a legal entity, not a natural person.

Legal entities cannot make friends.

Management can be friends with the management of other companies, to the extent it doesn’t interfere with their fiduciary duty to their shareholders.

I know this is a little depressing, but please remember this is business and not the playground.

BitStrategy@BitStrategy21

It’s possible to produce a good product, and still lose market share against the market leaders. Look at MicroStrategy. Fantastic product. Truly innovative software. This didn’t stop them bleeding market share to larger rivals. MicroStrategy partnered with Microsoft in 2023. This doesn’t mean Saylor won’t attempt to eat MSFT’s lunch on the Nasdaq. Friends in the boardroom, but enemies in the capital markets. Smaller BTCTCs can be viewed similarly. Both Metaplanet and Strive have genuinely innovated in the Treasury industry. They have formed close industry ties with the market leader. Innovative, and rational. Youthful, energetic management teams. Competing against giants. Reminds me of MicroStrategy in 2000. Saylor later realised you have to dominate the industry, or you die. That’s why he pivoted to Bitcoin. There was no other way out.

English

BitBrew retweetledi

I spent the past few days in Washington with @hyperliquidpc meeting with policymakers during the historic advancement of the Clarity Act. We discussed Hyperliquid, the benefits that it offers to American consumers, and the regulatory path to bring onchain derivatives markets into the United States.

Some conversations were technical with an impressive baseline understanding of Hyperliquid. Discussions included how onchain trading is a financial innovation that has clear global user demand. Other conversations focused more on a first principles introduction to defi and the promise of onchain markets. It was encouraging to see bipartisan support for thoughtful regulation of crypto. I look forward to continuing discussions in DC and working hard to make American access to Hyperliquid a reality.

English