Carlos M@Carlos_MoraM

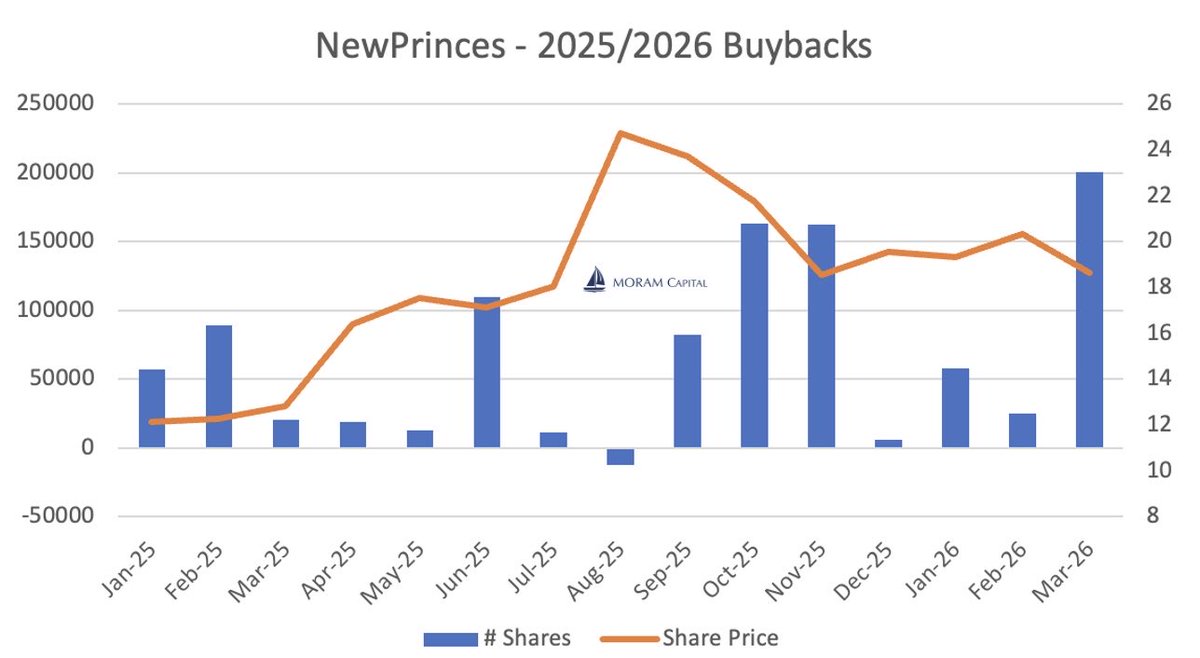

🇮🇹NewPrinces $NWL.MI – Updated Equity Research

One of the companies we have spent the most time on over the past 4 years.

🎯Today, we cover:

• FY25 results analysis, with a detailed breakdown of the main drivers, Q4 negative FCF, balance sheet, …

• Independent assessment of the current situation at Princes UK and Carrefour Italia

• The key elements of a potential Carrefour turnaround, including real estate, synergies, operational levers…

• Our 2026–2028 outlook for NewPrinces (Princes & Carrefour), based on our own assumptions

• Our estimate of Carrefour’s free cash flow based on all currently available information

• Capital structure - both at Princes and at NewPrinces - and the group’s financial position

• Our independent valuation, both for Princes on a standalone basis and for NewPrinces, under the two scenarios we consider most likely

• Our thoughts on NewPrinces and what has changed since Tuesday