@rugbyreplays Mate thanks for getting the games up so early.

Hopefully it's possible to do the same next weekend 🤞

English

P B

138 posts

Arbitrators comings and goings: Challenge to Philippe Sands is upheld - iareporter.com/articles/arbit…

Happy New Year to all my followers! 😆 #NYE2024

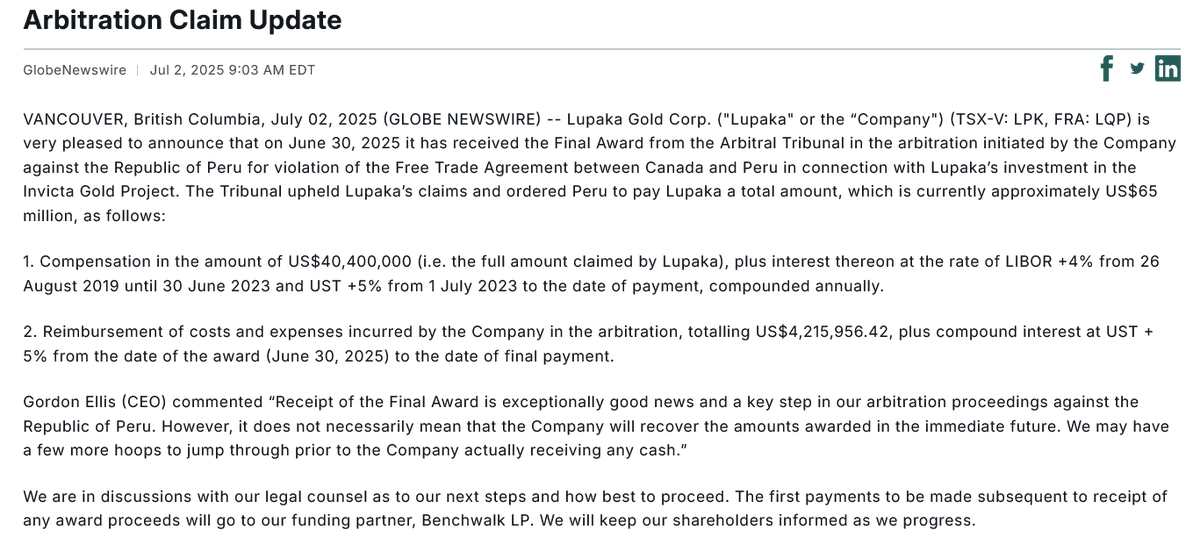

Lupaka Gold Corp. says an ICSID Award dated June 30, 2025, is payable at about US$67M as of Oct 31, 2025. It has engaged an agency to identify assets for potential seizure if payment is not made. $LPK.V Full release 👇 orestocks.com/company/LPK.V/…

@MMichalek91 IMO post CVRs looking at $8m+exp (EV ~32c + gold prospects) Also, settlement risk is lower - strong case - Tanzania poor, Peru moderate - previous similar (less egregious) ICSID case (Bear Creek) had no annulment, tho tactics can change (BW gets 4x) x.com/bonucci_p/stat…

#PAT Panthera Resources remains my top portfolio pick. Why do I like it? - Full exposure to the gold price - Undervalued Mali gold asset - A fully financed and advancing legal claim for a minimum of $1.6bn damages against the Govt of India My base case is 10x in next 12 months, basis just the legal case advancing. Timetable set today: 1 year AHEAD of what I was expecting. londonstockexchange.com/news-article/P…

@MMichalek91 $MON.V 60c PT is ambitious IMO. I was guessing mid/high 30s (quick calc). IMO another where the NPV is pumped - but at least the equity is low and LF (OBL) cut is manageable (~US$12-15m) so there is a return. Downside protection from TZ history (IDA,WINS) suggests bankable win.

Another pumped-up NPV is $OMEX - not even a PFS ffs. Cost redacted too given disputed. My research suggests low. Comp v $100m MC 😬 Ann't soon - decision delayed so likely split decision - Philippe Sands has form and already dissented on a PN

@Michal16122021 @JRMiningIntel $LPK.V wins as expected - best case details & team I've seen - social licence rightly questioned by arbitors (up on YT). Good news for pre & post CVR holders. Latter get $8m+exp in stub value = EV >32c + gold prospect upside - time value v Current SP 20c (even after >150% day)