Sabitlenmiş Tweet

I am honored to be a @BusinessInsider rising star of venture capital in 2023 ⭐

From bank teller to VC, it is honestly still a dream that I get to work in venture for a living!

Thank you to the BI team for sharing my story 🙏🏼

I hope it inspires the next generation of VCs!

I hope it shows that anyone can break into VC, even those with an uncommon background.

Full write up for those who can't access paywall:

--

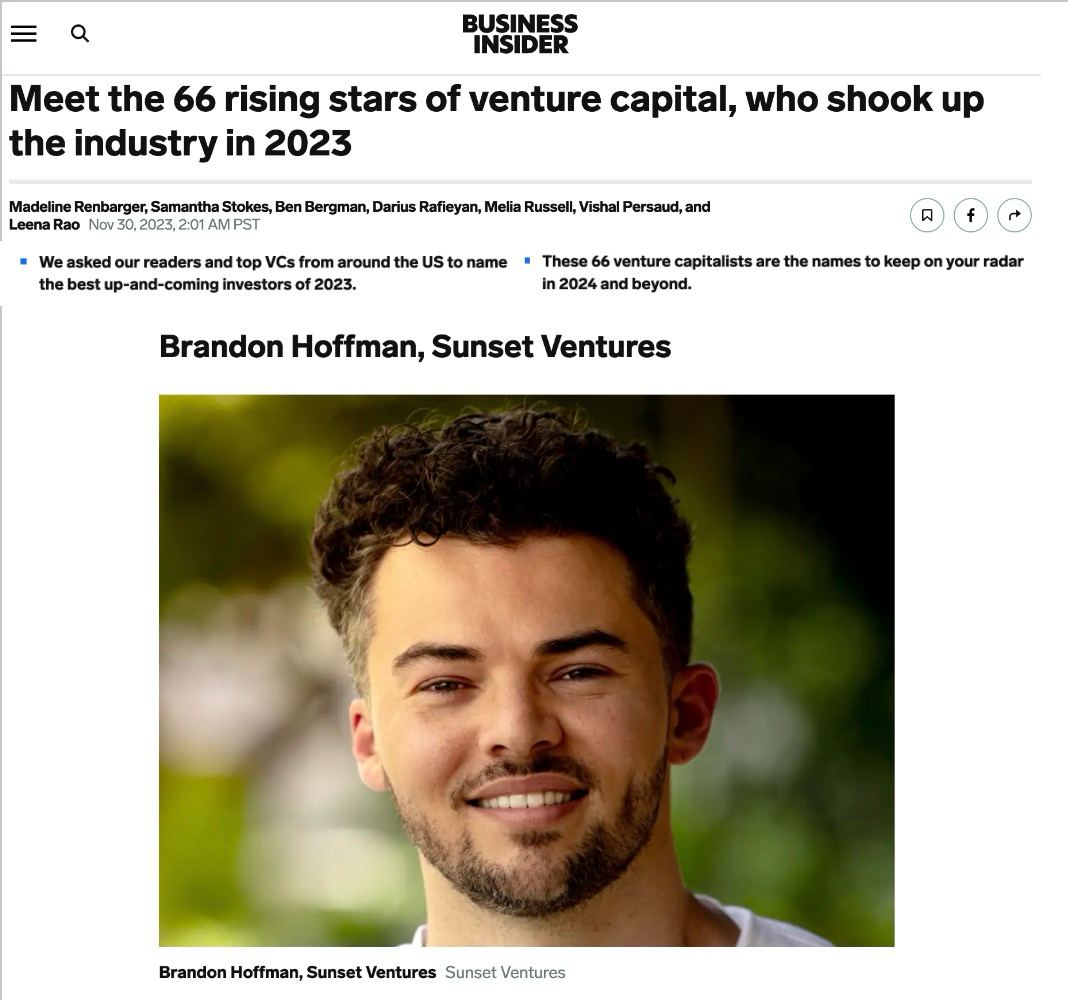

"Hoffman began his career as a bank teller in 2006 at a local bank in downtown Anaheim. He used his wages to pay for college and eventually built a music production studio, and eventually worked in equity research at @MorganStanley.

Hoffman got the startup investing bug and joined Samsung Electronics's innovation and VC firm, @SamsungNext, where he helped lead investments in @readyplayerme , @yugalabs, and @WonderDynamics.

Last year, Hoffman broke out on his own with @SunsetVC , an early-stage fund that got the backing of @BankofAmerica and @alexisohanian's @sevensevensix

Hoffman says the best way to break into investing is by getting "hands-on experience doing the work of a VC."

"Start by joining VC communities and programs that offer intern, fellow, or scout opportunities," said Hoffman.

He said he started angel investing with small amounts on AngelList and then built an angel community. He also volunteered as an intern at @HarlemCapital in 2018 when their first fund was being launched."

English