English

capnpope

2.5K posts

@capnpope

friend to your favorite liquid funds @nyu

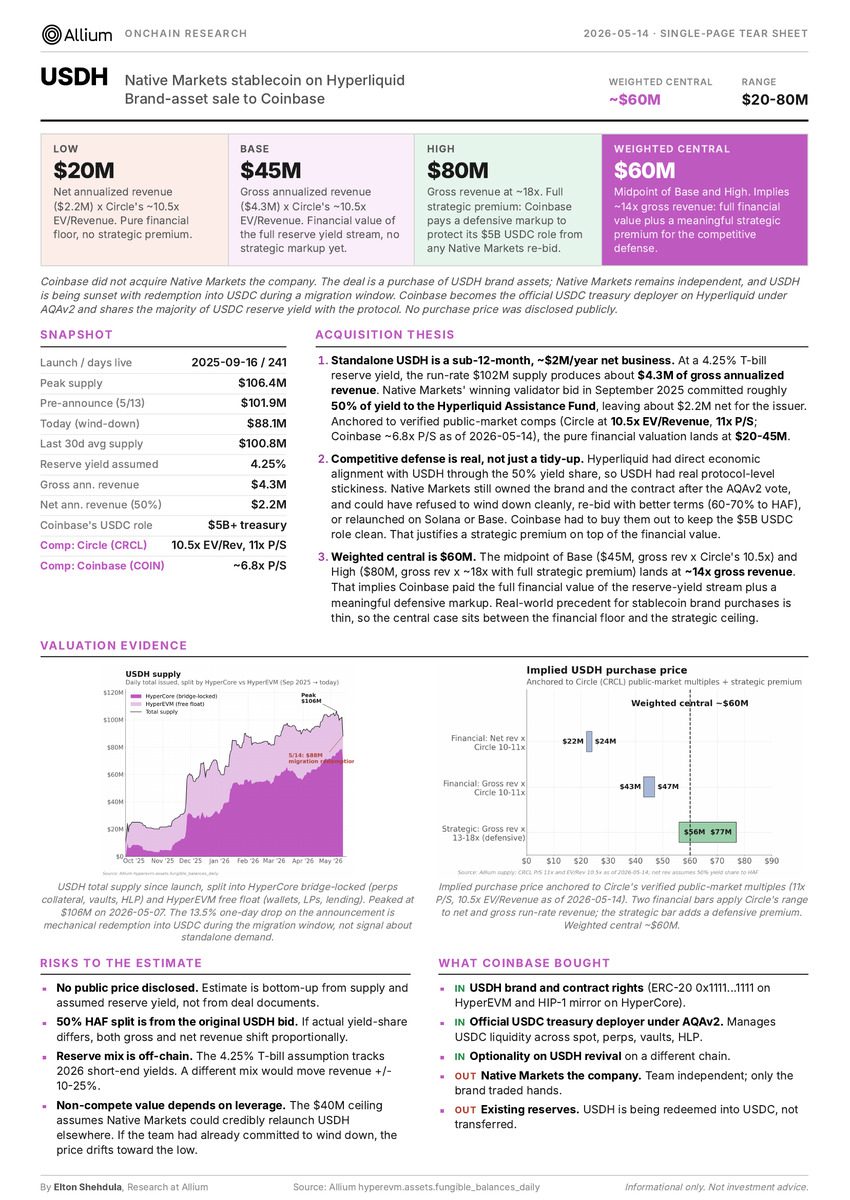

[ ZOOMER ] COINBASE ACQUIRES HYPERLIQUID'S USDH DEPLOYER, NATIVE MARKETS, TO SWITCH ALL USDH INTO USDC: BLOG

Today we’re expanding our support for @HyperliquidX by becoming the platform’s official treasury deployer of USDC. Onchain markets operate 24/7 and require collateral that is always available, instantly transferable, and deeply liquid - USDC delivers exactly that. Alongside this, we’ve also significantly increased our position of staked HYPE.