Echidna

880 posts

Echidna

@cardinalcap12

Buying good businesses and temporarily cheap stocks.

Katılım Nisan 2014

540 Takip Edilen659 Takipçiler

$ACIC $CB $UVE $HRTG

American Coastal buying back their stock is a great sign.

They have done the special dividend each year at the end of the year and that is my favorite use of their cash, but to buy 1% of their float in a single transaction opportunistically tells me they are now in a position to put capital to work, vs a few years ago being on the verge of death.

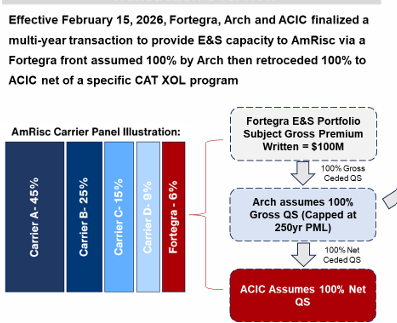

The easy math here is the legacy insurance firm is worth $20-$25, the new MGA is $7-$10 of value, the E&S is hard to value right now so just being cautious we will call it a $0 so, you are getting their 6% co part with AmRisc and ACES plus the MGA and half the insurance firm for nothing.

English

@evantindell @jefke00 wouldn't be surprised to see a series of special dividends to get the capital out.

English

@jefke00 well i dont know if anyone will care about the economic shares, BUT it is true that this massive dividend can be paid with a surprisingly little amount of $ leaving the entity

English

Bollore $BOL.FP announced a div of 1.5 EUR vs a last px of 4.368 EUR

This "amounts to" 4.2b EUR but the vast majority will stay within the Bollore complex.

A lot of it will end up at L'Odet, which is itself majority owned by BOL.FP...

🍿🍿🍿

disclosure: still long

Fox Castle Holdings🇬🇧🇺🇦@FoxCastlehold

Bolloré: boom! 1,5 € exceptionnal dividend

English

@radigancarter Interesting. Thank you. Can't we hold Kharg hostage to open up Hormuz? If we blow it up, Iran loses all oil income and the regime collapses.

English

@cardinalcap12 I'm genuinely not trying to be negative, but from what I know we have no ability to blockade Kharg and no ability to refuel ships in the gulf with the damage Bahrain sustained. Plus any port that refuels the U.S. is being actively targeted.

English

Got the wife evacuated, so have time to drink a tea and think about the Strait of Hormuz. I've sailed through the it a few times years ago and done antipiracy operations in the Strait of Malacca.

Maps can be deceiving. The best way to think about the Strait of Hormuz is a four lane highway, with two lanes per direction for the largest ships like crude carriers, cargo vessels, and warships in the center of the channel where it is deepest and free of obstacles.

Then on the outside of those lanes, you have medium sized ships, going Jebel Ali to other regional ports like Sohar, since a lot of international cargo goes direct to Jebel Ali then is cross loaded across the region.

On the outside of those lanes, along both coasts, are dhow fishing boats and all manner of local, smaller craft. Maritime trade crisscrossing this region goes back hundreds of years. The Portugese wrote how disappointing it was to find a tight network of trade already established in the region when they arrived in the 15th century.

It is hard to describe how crowded these waters are. You sometimes wonder if you could walk to Iran across the decks of ships and not get your feet wet.

The amount of traffic makes distinguishing between normal traffic and a threat incredibly difficult.

Is that dhow fishing, transiting between coasts, laying mines, gathering intelligence, or a tender for surface drones? Hard to discern while sailing ducks in a row escorting a lumbering tanker or cargo ship.

Operation Prosperity Guardian in the Red Sea proved to be a Houthi victory when a land power with no navy to speak of fought the most powerful navy on earth to an agreement.

The Hormuz problem is harder now the Iranians have proved they have the will to fight, no matter how much pain is leveled at them from afar.

The shipping lanes in the Strait of Hormuz go around the Musandam penninsula.

This turn exposes ships to 270 degree of fire control in layered systems from Qeshm, the surrounding high ground, to further inland, with surface drones now added to the mix.

Iran doesn't need to mine the entire strait. Iran just needs to turn that main shipping lanes around Musandam into a kill box and divert approved ships past Qeshm, out of the main shipping lanes like a watery weigh station. It has started doing this.

The U.S. has created a hard problem for itself.

NATO understandably wants nothing to do with this. If the most powerful navy in the world can't solve this, what difference does European navies make.

With the watery weigh station past Qeshm, Iran isn't closing the strait to global commerce. It is simply doing what the U.S. does with the dollar, exerting power over the chokepoint it controls.

Understandably the U.S. doesn't like this, so why can't the U.S. just send warships to escort ships through?

Well, when you escort a ship through a strait, you tend to stay ducks in a row.

So if warships are sent to escort tankers, they are now just another target in the strait.

Even if the warships could maneuver through local traffic to screen ships, lets go back to the 270 degree turn around the penninsula.

The warships would be receiving layered waves of fire likely worse than they faced off with in the Red Sea against the Houthis from essentially three directions while having the longer route to run to protect the tankers around the peninsula.

As the Hormuz Crisis drags on, anything less than breaking Iran's control of the strait will be seen as a loss for the U.S., much like the Battle of the Red Sea was against the Houthis.

English

@SpecSitsCapMgmt @gqfrs @ActionManNews What happens to all of the cash that will go to Bollore, then to Odet and then back to Bollore? Another special dividend?

English

@gqfrs @ActionManNews That is true. The dividend is an important signal. But the discount of Bollore and Odet truely lies on the complexity of the Bollore Galaxy and its control loop. I continue to believe that a merger would be the ideal way to realize a large portion of the discount.

English

Bollore $BOL.FP proposes EUR1.50/share exceptional dividend, a 34% dividend yield to today’s closing. That is EUR4.2 bi, with EUR3 bi flowing through to Compagnie de L’Odet $ODET.FP. That should give ODET fire power to make any move it wishes within the Bollore Galaxy.

English

US tech investors are leaving money on the table - they don't even know it.

Sinan Xin is Managing Partner at Amber Road Investors LP, where he runs a long/short EM tech book spanning China, Latin America, Southeast Asia & beyond. A Penn economics graduate, he ran the Internet, Software & Payments book at Citadel's Surveyor Capital, and has been investing in EM tech since before the Alibaba IPO.

"There are companies in EM tech growing faster than developed market peers, run more efficiently, trading at significantly cheaper multiples - and that's 2026."

We cover:

- Why e-commerce behaves the same globally but fintech is radically different culture-to-culture

- The specific framework for building conviction in stocks you have no cultural home advantage in

- How private VC relationships in Brazil, Singapore & Mexico surface public inflections 6-12 months before the Street

- Why cross-EM correlation is structurally lower than within the S&P — & how that changes your risk math

- The Brazilian fintech trade in 2022: how less VC capital = less competition = path to profitability nobody priced

- Running longs & shorts across Latin America, China, Central Asia, Middle East & Southeast Asia in one book

- Why US-centric funds will always cut EM positions first & why that's your edge, not your risk

Highlights:

00:00 How Sinan Xin Builds Edge in Emerging Markets Tech

02:07 Understanding Culture and Tech in Emerging Markets Investing

04:25 Sinan’s Process: Seeking Change and Primary Research

11:23 Building a Resilient Portfolio in Volatile Emerging Markets

25:05 The Human Element: Relationships and Scar Tissue as Edge

31:07 Why Understanding Behavior Is the Most Durable Edge

40:03 Finding Career Alpha Beyond Rational Economic Outcomes

55:43 The Sum of Individuality: Sinan’s Firm’s Distinct Edge

English

$1T in Medicaid provider spending data released on opendata.hhs.gov. Public should know how its money is spent!

English

Not sure I've ever seen more de-rated and/or outright cheap defensive, compounder-y stocks with decent bal sheets and revisions

English

@varunv_malhotra Doesn't CSU consolidate 100% and then subtract out the minority interest (roughly 40%)?

English

There's a $3B asset hiding on a balance sheet disguised as a $1B liability. Most investors see it and walk away.

(1) $CSU controls Topicus $TOI.V but only owns 31% of the economics. The Joday Group owns 29%. Those cash flows, roughly $65M/year, get subtracted from reported FCFA2S.

(2) Under the IRGA (Investor Rights and Governance Agreement), CSU can buy Joday's stake at a formula price based on Topicus' recurring revenue and book value

That formula price today: ~$1B.

Market value of that stake: ~$3B.

(3) Every quarter Topicus grows, the formula price goes up. CSU records that increase as a charge against FCFA2S.

In 2025 that charge was ~$310M.

It's accounting for a future payment. One that buys $3B of value for $1B.

(4) If exercised today: the $310M annual charge disappears, the $65M in cash flows starts counting for shareholders, and TTM FCFA2S goes from $1.7B to $2.1B.

The liability gets bigger every quarter. The deal gets better every quarter.

Downside is they can't call the option until 2043 for Robin's piece.

TTM FCFA2S says ~5% yield. Adjusted says ~6%.

On a compounder.

$CSU is cheaper than you think.

English

@HaydenCapital E-commerce w/o a dominant logistics footprint feels like a tough business. I think the stock is super attractive if you can gain confidence that SE has a long-term logistics advantage.

English

@HaydenCapital if you see convergence between SE's retail margin and Amazon's retail margins. However, I get the sense that SEA / Brazil are much more competitive and SE doesn't have the same logistics advantage given the presence of large 3P logistics players in Asia.

English

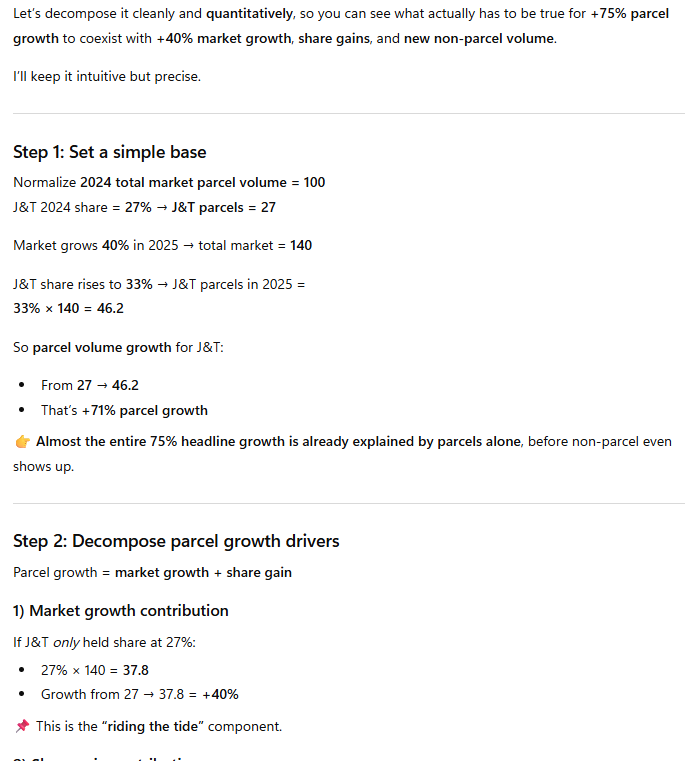

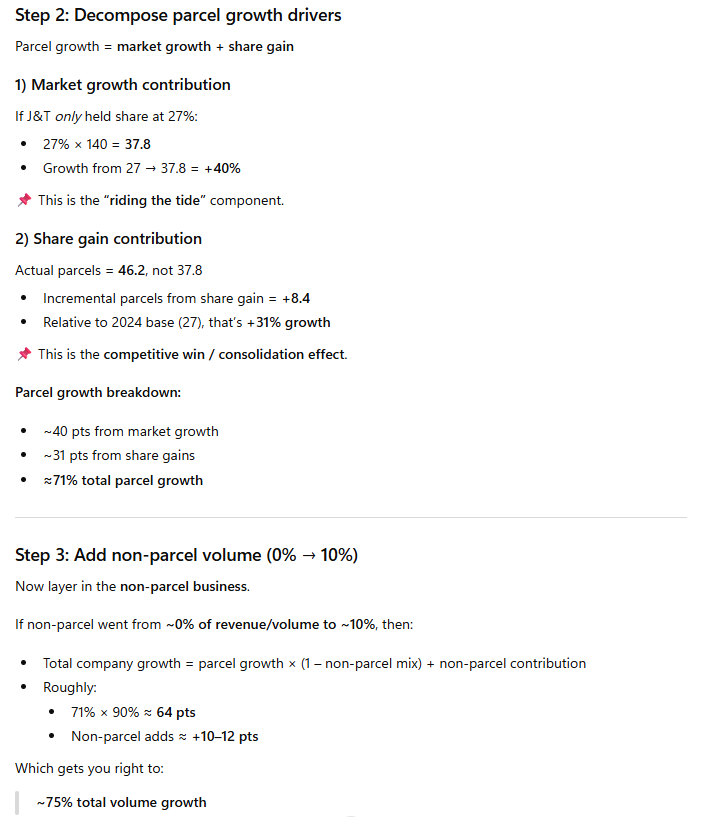

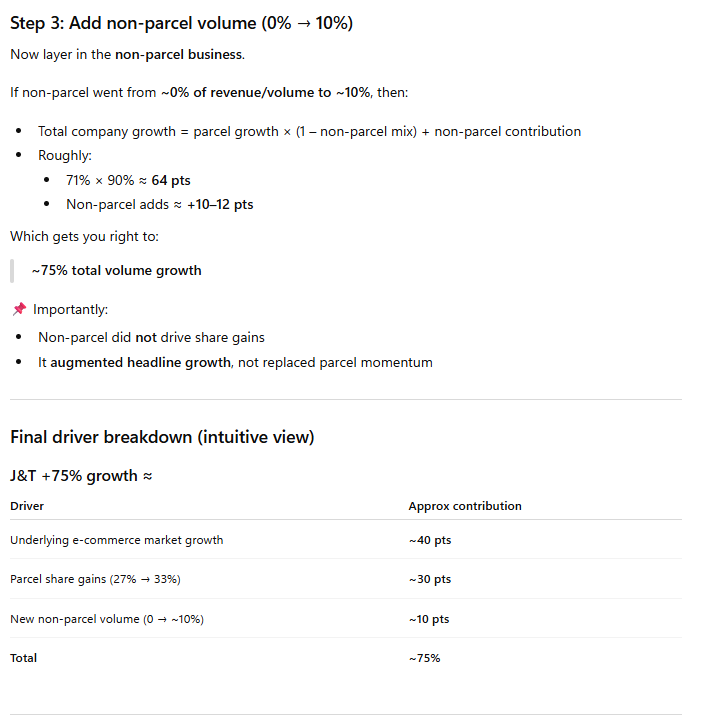

Just hammering this home. For simplicity's sake, let's use round numbers for 2025:

1) J&T Order Volume Grows: 75% y/y

2) Tiktok & Other Customers Grows: 40% y/y

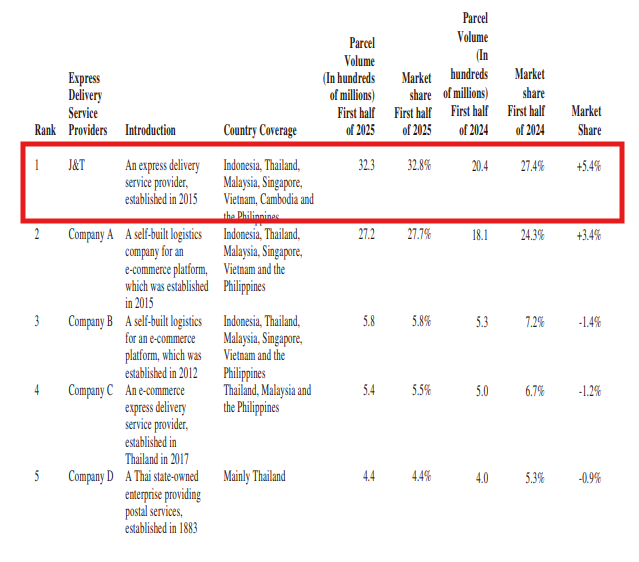

3) J&T Grows Market Share from 27% in 2024 > 33% in 2025 (disclosed in the 1H25 Report)

4) Non-platform % of revenue goes from 0% > 10% in 2025.

All the data-points line up.

Takeaway: It can be true that J&T grew 75% y/y, AND Tiktok is slowing to 40% y/y orders growth (and 30% y/y GMV).

- Market narrative of Tiktok competition increasing is likely wrong.

- Means that Shopee's recent spend is not a defensive move or coming from a weakened position.

- In fact, they're pressing harder, while competition is weak (That's just how they operate. They waited to grow Monee loans, until the digibanks started blowing up. That's why you see an inflection in loan growth 2 years ago. Compare that to when Indo digibank NPLs started blowing up, and you'll see the correlation).

Included pictures of the math (thanks ChatGPT). $SE $1519.HK

Fred Liu@HaydenCapital

More evidence it's just J&T taking share. Rival 3PLs leaving the market. Non-platform volumes are <10% (vs. almost 0 in 2024). So while that's a chunk of the 30% delta vs. TTS order growth, it seems like most of it is share gains.

English

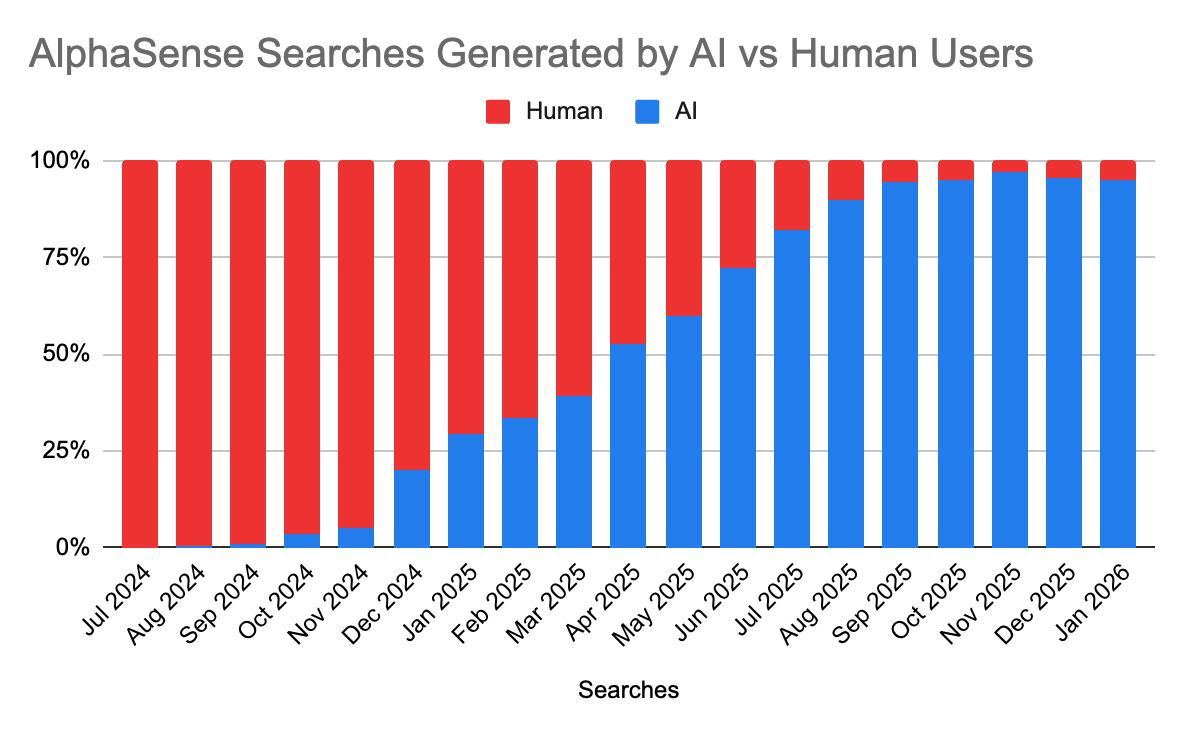

The biggest user of our tool (search) is already AI

Volume up ~20x

English

What software platform has a $300 billion market cap, has been in development for a decade, no large customers, actively traded, and generates less revenue than a mid-tier SaaS company?

English

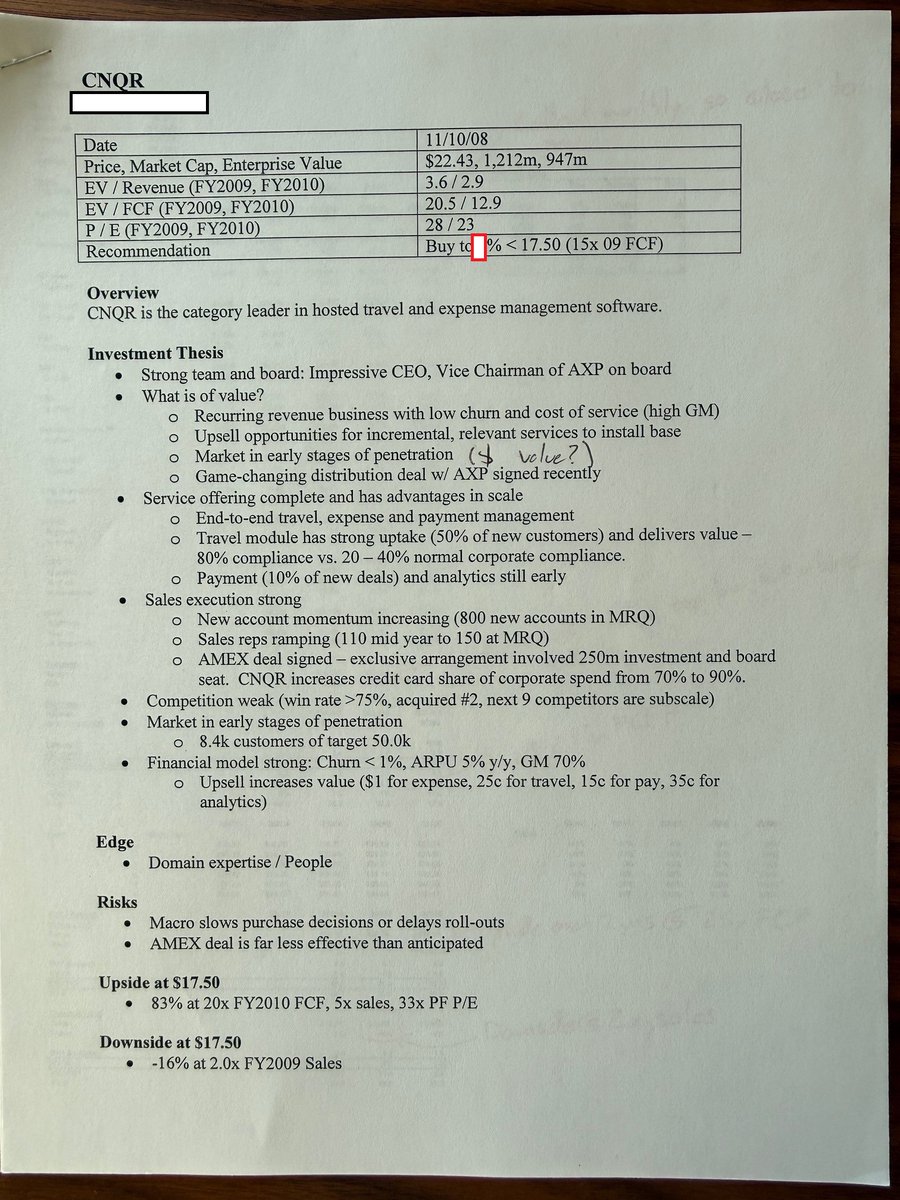

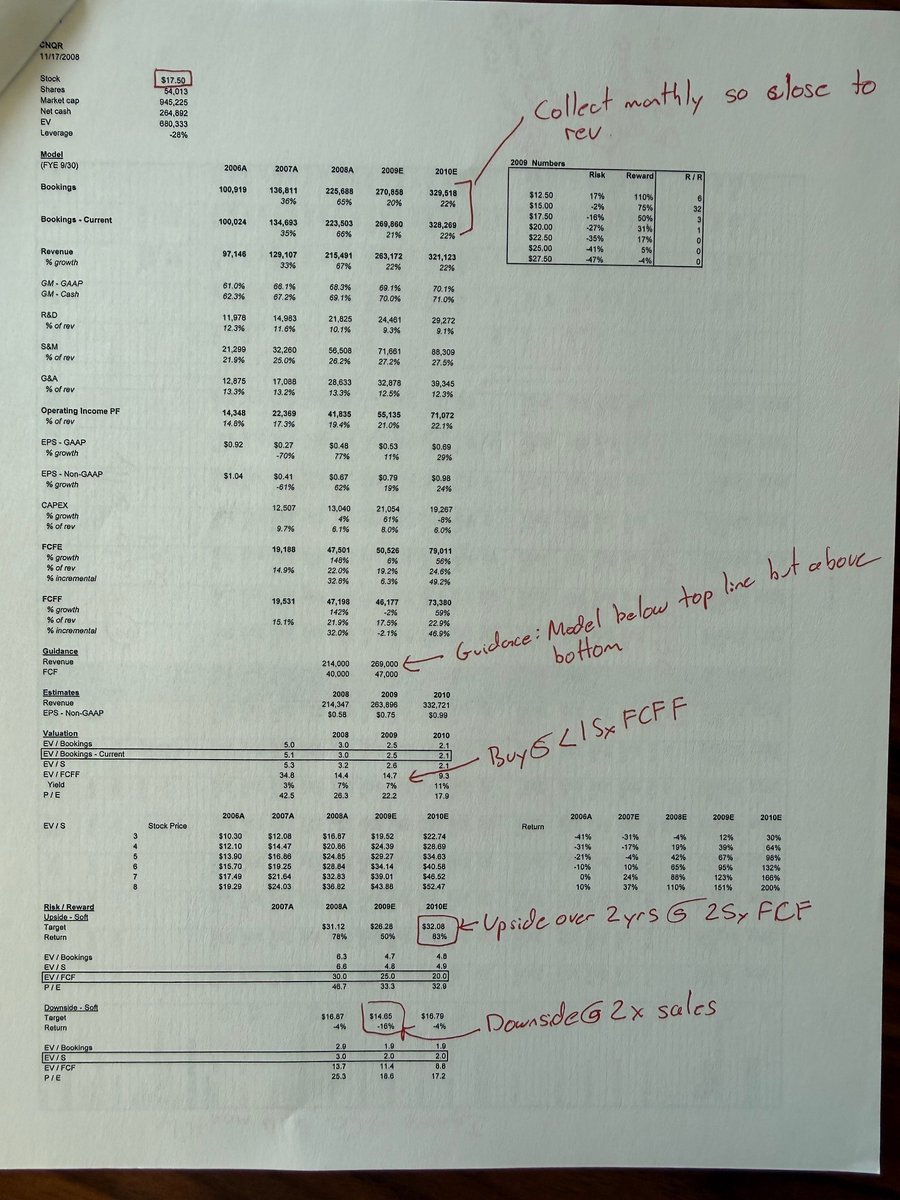

I love the SaaS chaos - kind of my jam. So much fun for a fundamental investor.

Below is my long pitch for $CNQR in the depths of the financial crisis in 2008. SaaS was a very novel concept / industry at the time so names got smoked even harder back then.

$CNQR had a SaaS travel bookings / expense management solution. Was sort of a no-brainer purchase for large enterprises.

At the time, I framed downside conservatively - 2x sales / 15x FCF was -16% lower.

Upside of 83% over a couple years to 5x sales / 20x FCF.

Stock 6x'd over 6 years from this entry point.

Not saying SaaS today is at all the same as back then, but $CRM / $WDAY trade at 12x / 11x this year's FCF right now.

They say stocks return to their rightful owners in bear markets. Come to papa.

English

(9 of 9) Given this type of issue, and for many other reasons, perhaps it should come as no surprise that the large-capitalization IT firms are very interested in building quantum computers.

English

(1 of 9) Quantum computers will operate at the subatomic or particle level, so it is easy to see that they will offer far more information density than the current binary-state logical devices.

English

@Pray4Equity What are steady state e-commerce margins? Seems very competitive with large 3party logistics players. US is much less competitive for Amazon.

English

So $SE is basically like if Fortnite decided to build a mini-Amazon’s worth of distribution footprint and offer retail online shopping, THEN they built Zelle, Venmo, and etc all-in-one, then they cross-sold financing to all their best online shoppers while keeping the most popular mobile game as free advertising space for their other business lines? Am I getting that right, because if I am, that kinda kicks ass.

English

@Discounted38988 They're robotaxi / rideshare losers too, as personal car ownership becomes less necessary.

English

I can’t imagine having 30-40% of my net worth in storage facilities right now.

This ZIRP bubble is going to pop and carnage will ensue.

I’m very bearish on self-storage companies right now. $PSA $EXR $NSA all of them.

There is no way these companies can live up to their valuation.

30% + correction in the next 18 months. More for Bolt Storage investors.

The developers and owners of this 3-cap junk going to go bankrupt too.

English

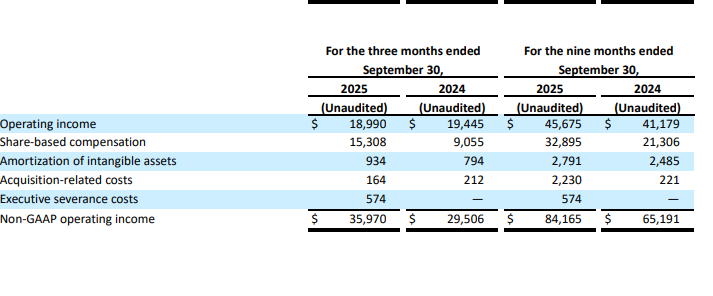

@AggieCapitalist It's 40% of adj. EBIT in the first 9m of 25. I want to like one of these software names, the math just doesn't pencil for me.

English

$CLBT down to 15x '27 EV/FCF vs Mkt at 36x trailing. An entrenched duopoly that will do 20% ARR growth & high 30s EBITDA margins. OBBB added $1T to its customer's budgets. Used in 90% of court trials. Hard to get on FedRAMP approval list, don't think FBI will jump to vibe coded.

English

@FromValue What do you think a fair multiple to pay is for a company that grows LSD organically? Each year, CSU must allocate more and more money to acquisitions, which either entails a higher cash drag due to undeployed capital or lower return M&A.

English