chait

388 posts

@chaitanyam Check out US exports now that it has a stranglehold on global hydrocarbon traffic

English

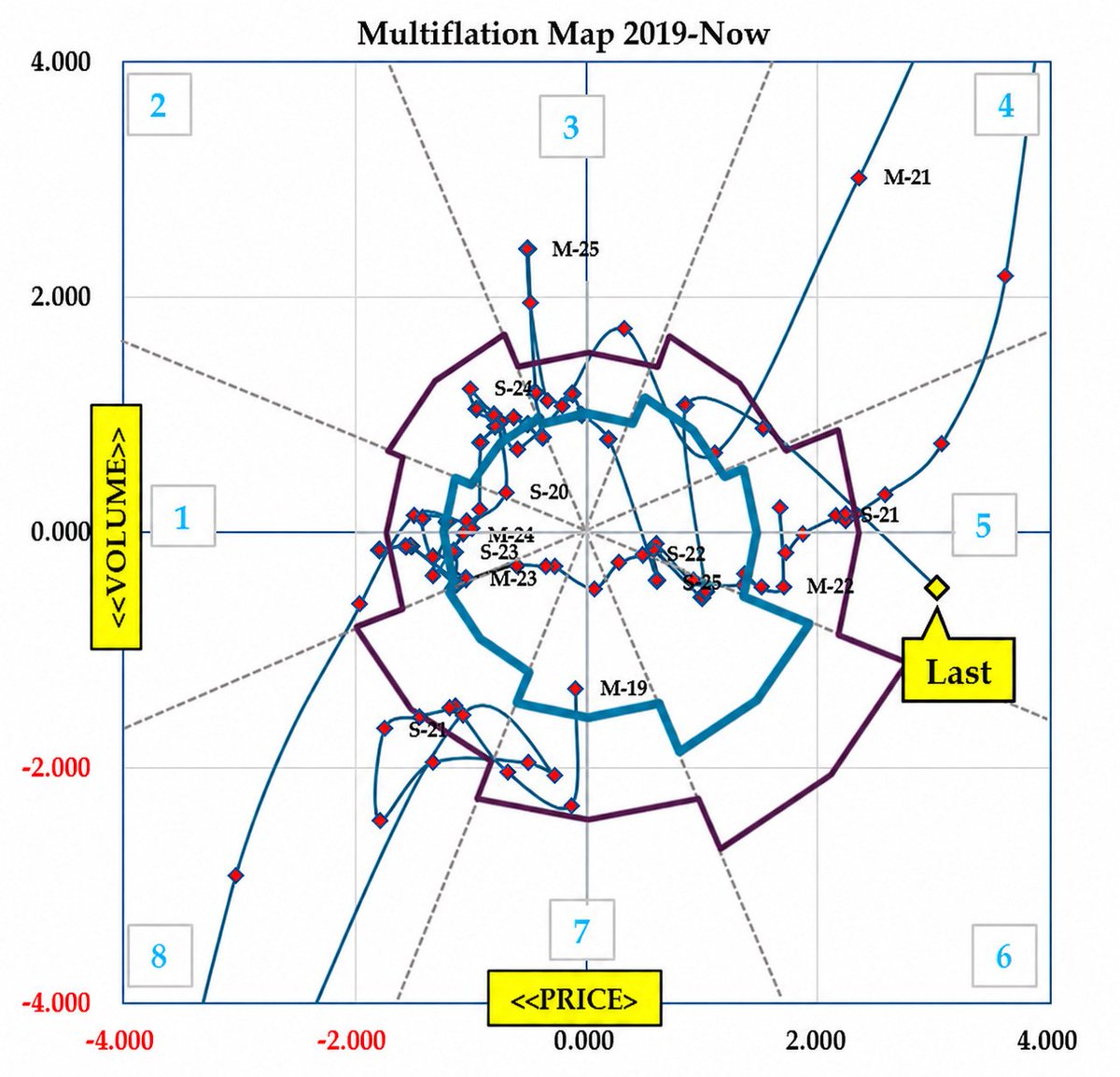

Multiflation Map Update 05.13.26

Stagflation deepens; CPI & PPI hot

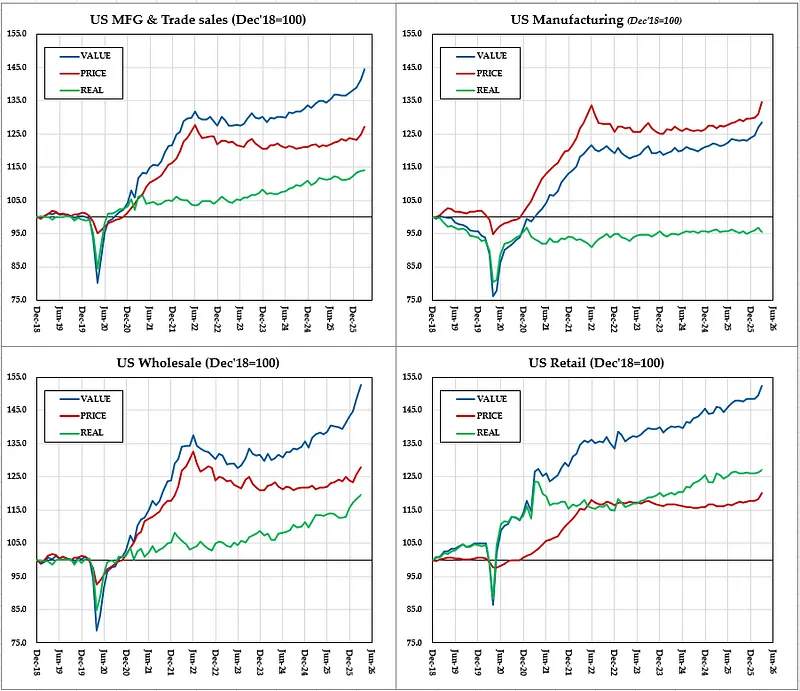

Beneath the surface, the US economy is becoming increasingly dependent on a remarkably narrow engine of growth. Prices are beginning to rise quickly, real economic activity is losing breadth, and what momentum remains is concentrated in just a handful of sectors: fuel and AI-linked technology. Yesterday’s CPI showed the boost from energy prices that made such a contribution to our price measures

As we noted earlier (see quoted note), provisional estimates point to an economy moving firmly into stagflationary territory. Inflation is accelerating sharply, yet volumes—while still growing—are doing so at a diminishing pace and in an increasingly unbalanced way, skewed toward wholesale activity.

The source of the recent surge is hardly mysterious. The categories of petroleum and coal together with gas stations account for much of the acceleration in turnover. Over the past two months, the sales measures we track increased by $77.3 billion, or 3.7%. More than half of that rise—$39.8 billion— stemmed from a 22% jump in fuel-related sales alone.

Strip out the inflation effect, however, and the picture becomes materially weaker. Manufacturing volumes are now slightly lower year on year, a decline only narrowly offset by gains at the retail level. Indeed, just two wholesale segments—fuels once again, alongside the category containing computer-related goods—generated fully three-fifths of the entire increase in real sales volumes.

Fow now, America’s apparent resilience rests increasingly on two pillars of uncertain durability: its tightening grip over global hydrocarbon trade and its debt-fuelled appetite for AI-adjacent technology.

English

chait retweetledi

Stagflation is back; Stocks Are Shrugging…So Far

Multiflation Map Update 04.30.26

Based on our early data, recent US military actions in the Gulf are hitting the economy, bringing us the worst of all worlds: slowing growth and spiking prices.

Our proprietary Multiflation Map readings have been pushed out into the Multiflationary badlands for the first time since the Trump tariff shock a year ago. What makes this episode uglier than last year is the direction: the tariff shock at least gave growth a brief kick. This one offers no such consolation; we haven’t seen this specific combination of subpar growth and above normal price rises since the “transitory” 2021 inflation shock of COVID19 and the QE response.

Right now, the stock market is blissfully ignoring the warning signs. Even as stocks shrug, international bond markets—especially outside the US—are starting to sweat. But a reality check could be coming if we stay in this economic danger zone for much longer or bond markets deteriorate further.

(One caveat: we’re working with only two of our three key growth (revenue) series so far; we filled the gap with an estimate based on their magnitudes. We also used alternative numbers from official sources to gauge the price index outcome. Neither should be a major issue, but worth noting.)

#Multiflation

English

chait retweetledi

One of the best things about getting hacked is that I wasted less time shit posting this weekend and did some actual work to elevate my prior dogshit image game.

Spelling may even be a little better. Have a read.

No sketchy link. You know where to find me.

English

US TIPS 30Y real yields closed at their highest ever level on Friday

English

chait retweetledi

thanks to everyone who shared this. For those asking about the main differences:

- credit spreads had blown out before the 1990 oil shock. The credit cycle had already turned

- the corporate sector was in deficit in 1990, whereas that is not the case today (although position today somewhat flattered by superstars)

- the US was a net energy importer in 1990 and the oil intensity of GDP was higher

- the dollar was falling, in part because the RoW (esp Europe) was expected to absorb the shock better. Germany was about to get its reunification boom

Dario Perkins@darioperkins

🧵Let me take you back to August 1990. Three weeks ago, Iraq invaded Kuwait, oil prices have surged, and the FOMC is meeting to decide how to respond. The economy looks wobbly. Payrolls just recorded a small decline. Greenspan talks about a credit bubble that has started to deflate. There's more than a few credit cockroaches. But nobody thinks the US economy is sliding into recession. The Maestro urges stoicism. Nobody knows what’s going to happen in the Middle East, central banks cant really alter the outcome, so its best to provide stability – by doing nothing.

English

@Geo_papic In the same interview, he says "We'll continue to defend ourselves for as long as it takes in order to end it in a way that it won't be repeated in the future." Sounds like they still want to impose economic pain. Not sure how that's compatible with opening up the strait.

English

@Geo_papic Huge fan of Geopolitical Cousins. You've often talked about IRGC's pain tolerance being low. Is this essentially Iran's capitulation? The article makes it sound like anyone can move oil through the strait under China's or India's flag. And surely the IRGC knows this.

English

Man... I feel like IRGC really needs to start listening to Geopolitical Cousins. This is not how to do it.

jpost.com/middle-east/ir…

English

I’m thinking of adding up all of the signals in the Prometheus Multi-Strategy Program into one index.

What’s a catchy name for a silver bullet like this?

English

chait retweetledi

@cullenroche At some point people will demand redistribution. Probably even go too far in that direction if what you describe happens.

English

Something I am thinking about a lot these days:

Let’s say AI turns out to be the humongous job killer that some think it will be. That would result in a huge decline in aggregate demand and negative wealth effect across large swaths of the economy. GDP stagnates, but doesn’t necessarily go down. Unemployment goes up enough to get a technical recession.

The wealth accrues to fewer and fewer firms and people (the stock market could, paradoxically, go UP in this recession, after initially collapsing). Yields collapse. The Fed stimulates. QE to the max. Automatic stabilizers fill some of the void. The deficit explodes. Calls for a UBI become more prominent. This gets worse and worse until the govt is filling the aggregate demand void entirely (which they’ll be able to afford because inflation will be so low).

TLDR: All of the mega trends of the last 40 years get exacerbated.

What am I missing?

English

chait retweetledi

My annual 2026 outlook is out. Get it now and also subscribe; I promise not to clutter up your inbox with any content whatsoever between tomorrow and 2027 quantian.substack.com/p/2026-market-…

English

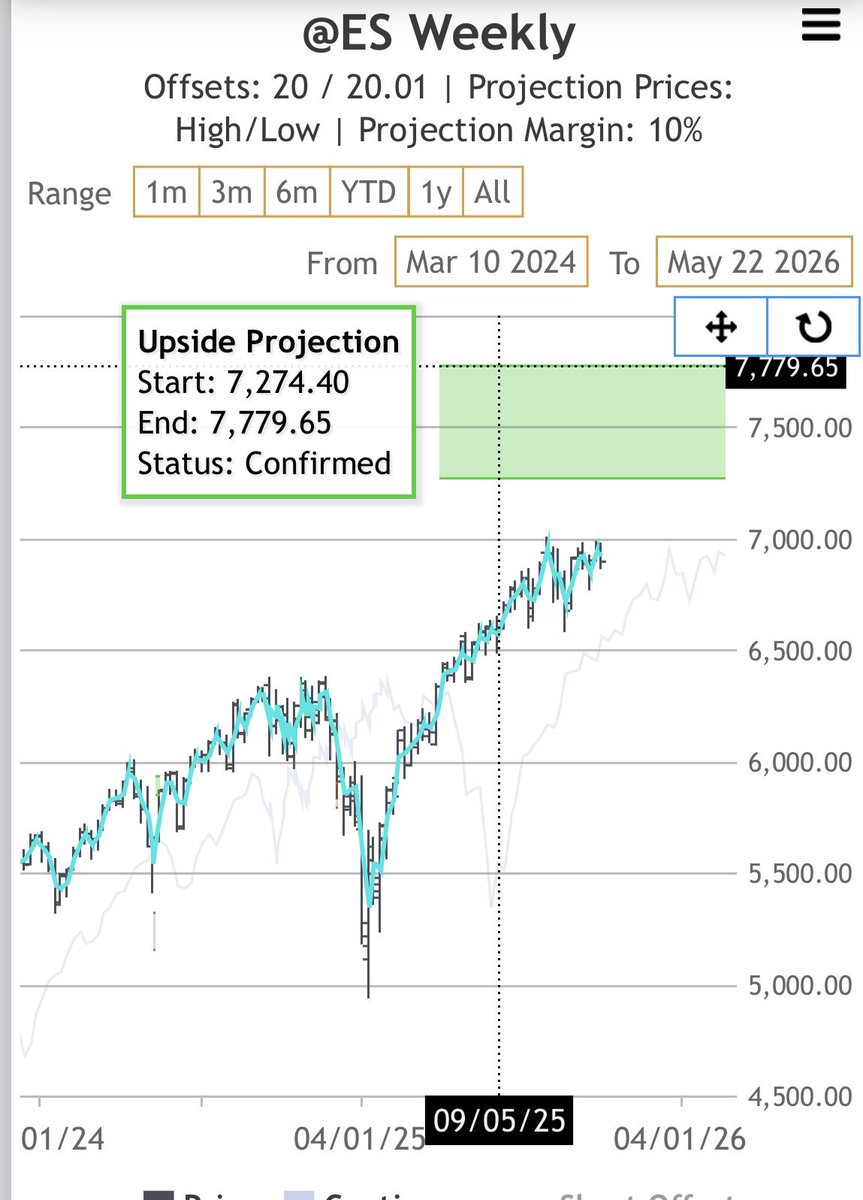

11) The highest target that’s in play in $SPX is ~7777 which got triggered in June 2025 as part of crossing 20W cycle offset. While a bit above my base case, it’s possible but might need till March to be achieved if market doesn’t tank post Feb OpEx. IMO the higher we go in Q1, the lower markets will go on the way down based on Hurst FLD method:

English

2026 forecast: 25% bear market and recovery

-Overall structure I see: head fake in Q1, multi-month liquidation, Q4 rally

-Up till ~Feb 17 (7250-7400 $SPX), then look for topping signs/divergences

-Mar 27 minor low

-Early warning sign that market has topped is acceptance below 6532 which takes us to 6144; below it we go to low 5K

-2 Potential key low dates: July 24 and Oct 27 where I see 3.5Y cycle low

-July is likely a major low followed by a big rally; Oct - lower low that is divergent giving cleaner entry

-5200 target; extreme low range is 4600-4800; upper range is 5400-5600

-Big rally in Q4, year end target 5950

-All 4 previous annual forecasts are included on the chart for reference

-Commentary and other assets forecasts to be added over next few weeks in the thread below

-If you found my work helpful - can support with retweets

Namzes Cycles@Namzes_G

🔮 2025 forecast: Heading towards major market top ⚠️ -📉$SPX: overall structure is up early in the year, 10%+ correction, then melt up into major top, followed by ~17% drop that kicks off a bear market: ⬆️ Up till ~Jan 17 (~6250) then 10%+ correction by end of Q1 (~5600 target) 🎁 Buy points ~Feb 26 and second half of Mar (ideal date is Mar 28). This is primary buy point for the year setting up final leg up for the cycle 🎁 Minor buy point ~June 27 ⚠️ Major top ~July 17, then Aug 22 ether lower high or double top/divergent high with 6500 min target I outlined a few times past 3 years & ~7000 upside target 🎯 🔽 Down into ~Oct 27 (seasonal low & nested cycle lows), then bounce which fails 📉 $SPX ends the year red setting up disastrous 2026. YE Target 🎯 5650 -🅱️ $BTC: Deep retest into March low, followed by 1 more run at the highs early summer; after which crypto starts multi year bear market. IMO high probability that next 4 year cycle (2026+) will be left translated and Saylor & $MSTR will be liquidated and $USDT #tether fraud will also likely be exposed, while almost all alts lose 99-100%. Right now it’s unclear if BTC will act more as a NASDAQ proxy or monetary hedge in the years ahead. Many alts have potentially peaked for the cycle but some like $ETH have more upside. -💲 $DXY: Dollar likely to remain in uptrend into 2025-26. There is a potential pullback early in the year helping risk assets to push higher, then a rally into spring (risk assets sell off). Then big correction in $USD into July-Aug low which should coincide with the market top -💶 $EUR: 18M low is due and likely falls ~March '25. The subsequent 18M cycle is likely left translated with a drop into 2026 4Y cycle low where targeting below par vs USD -💹 $JPY : I’m still looking for #yen to start a secular multi year uptrend which will results in trillions in capital to be pulled back from US back to Japan 🇯🇵 during years ahead -📈 $TNX: bonds remain in a secular bear market so any rally in bonds will be cyclical (growth scare/recession) followed by a big rates rally. There is a potential counter rally in bonds in Q1 2025 which will fail. $TNX technical target is 5.5% -💰 #Gold: given that 2022 was 8 year cycle low, we have bullish IT/LT bias. There is a potential low in spring with ~$2400 support, then push higher towards high $2800-$3000+ into 2026. CBs won’t stop buying as war cycle and geopol tensions intensify while governments debase currencies. -🪙 #Silver: post consolidation, next target is $38 next 6Qs -⚡️🛢️☢️ #Energy: all energy should be in uptrend next 6-8Qs; NatGas likely being the leader (new ATH in ‘26), oil 80s in spring and 100, then 150 in 2026, uranium back to 100+ in 2025, coal as well. My oil leading indicators and cycles suggest a big move next 2 years but exact timing of expansion is hard to pinpoint, potentially ~end of 2025 into 2026. -🏦 Macro: GDP growth ideal cycle top is mid-2025 while unemployment should continue rising into 2026 suggesting recession could come in early 2026 or even end of 2025. -💦 Liquidity 5Y cycle peaks ~mid-2025 and should roll over which will a major issue for historically overpriced equities and crypto. The big question is with RRP drained, if/when Fed will provide liquidity to support asset prices without real economic reason to. -Commentary below 👇

English

@dwarkesh_sp @pawtrammell Two questions:

1. Does the state retain monopoly over legitimate violence in this future?

2. If yes, are governments still democratically elected?

English

New blog post w @pawtrammell: Capital in the 22nd Century

Where we argue that while Piketty was wrong about the past, he’s probably right about the future.

Piketty argued that without strong redistribution of wealth, inequality will indefinitely increase. Historically, however, income inequality from capital accumulation has actually been self-correcting. Labor and capital are complements, so if you build up lots of capital, you’ll lower its returns and raise wages (since labor now becomes the bottleneck).

But once AI/robotics fully substitute for labor, this correction mechanism breaks.

For centuries, the share of GDP that goes to paying wages has been 2/3, and the share of GDP that’s been income from owning stuff has been 1/3.

With full automation, capital’s share of GDP goes to 100% (since datacenters and solar panels and the robot factories that build all the above plus more robot factories are all “capital”).

And inequality among capital holders will also skyrocket - in favor of larger and more sophisticated investors. A lot of AI wealth is being generated in private markets. You can’t get direct exposure to xAI from your 401k, but the Sultan of Oman can. A cheap house (the main form of wealth for many Americans) is a form of capital almost uniquely ill-suited to taking advantage of a leap in automation: it plays no part in the production, operation, or transportation of computers, robots, data, or energy.

Also, international catch-up growth may end. Poor countries historically grew faster by combining their cheap labor with imported capital/know-how. Without labor as a bottleneck, their main value-add disappears.

Inequality seems especially hard to justify in this world. So if we don’t want inequality to just keep increasing forever - with the descendants of the most patient and sophisticated of today’s AI investors controlling all the galaxies - what can we do? The obvious place to start is with Piketty’s headline recommendation: highly and progressively tax wealth. This might discourage saving, but it would no longer penalize those who have earned a lot by their hard work and creativity. The wealth - even the investment decisions - will be made by the robots, and they will work just as hard and smart however much we tax their owners.

But taxing capital is pointless if people can just shift their future investment to lower tax countries. And since capital stocks could grow really fast (robots building robots and all that), pretty soon tax havens go from marginal outposts to the majority of global GDP. But how do you get global coordination on taxing capital, when the benefits to defecting are so high and so accessible?

Full automation will probably lead to ever-increasing inequality. We don’t see an obvious solution to this problem. And we think it’s weird how little thought has gone into what to do about it.

Many more thoughts from re-reading Piketty with our AGI hats on at the post in the link below.

English

I’ll post 2026 forecast today. It’s not meant to be a precise prediction that I’ll stick to: no one has a crystal ball. But it’s rather a probabilistic set up using various cycles, historical studies, models & TA; a scenario analysis for which I’ll use other tool to execute.

Namzes Cycles@Namzes_G

IMO Bottom is due (I won’t be able to tell until after the fact). We experienced a full blown crash with 3 huge gap downs. Ideally we bottom tonight or tomorrow in US session and then can start building structure above. Markets bottom on bad news and rally when news becomes less bad, they just need something to cling to. Ironically I was expecting 4800 SPX last August and didn’t expect us to go this deep in this expected window of weakness. But large picture view is that this test of Jan 2022 ATH is completely normal. Survive next week to live to see the other side of the crash.

English

chait retweetledi

🧵Things that wont happen in 2026.

some "hilariously" bold off-consensus forecasts

English

chait retweetledi

There has never been a time in my whole professional life that I started with some structural model and did not end up with a much simpler model in production.

And I still have not learned this bitter lesson.

English

chait retweetledi

Various members of the FOMC including the chair have made some unfortunate statements on their reaction function and what tariffs mean and why they are on pause. They are human and this stuff is super confusing.

The popular narrative is by many of the weaker FOMC members (and distressingly occasionally reinforced by the chair) is tariffs are definitely at least a one time upward adjustment to the price level. Even that may be false. If exporters, currency changes or importer supply chain eat the tariffs prices don't change. If because the importers eat the tariffs the reduction in their margin may lead to job loss which may hit demand and actually result in reduction in consumer prices.

However if money and credit is incredibly loose and consumers are willing and able to leverage up prices could fully pass through to consumers. If that is true it also is true that once the tariff price change occurs further inflation is likely as well because policy is too loose. This is the scenario that the weaker FOMC members are afraid of. It is highly highly unlikely.

Why unlikely? Because tariffs are an aggregate tax on an economy. While it's possible that the tax will be entirely paid by the export chain that is also highly unlikely. An increases of taxes paid by U.S. entities takes aggregate wealth from the private sector which is then burned by the government. This is a simple

Identity. Deficits up NGDP up Deficits down NGDP down.

Tariffs reduce NGDP full stop

So what's with the Fed? Some

of the dopey members are worried about ongoing post tariff inflation and really really shouldn't.

Otoh tariffs are NOT certain in legality or level. So pausing makes sense.

BUT the longer and more persistent tariffs are the more certain NGDP will fall. It's NOT inflation that will drive a cut it's persistent tariffs despite what the FOMC says. In fact tariffs going away which would restore NGDP to pre tariff trends is when the Fed will hike or persist in pausing.

Yes they are paused due to uncertainty. BUT only the dopey ones are paused due to inflation heating up in a high tariff world.

English

chait retweetledi

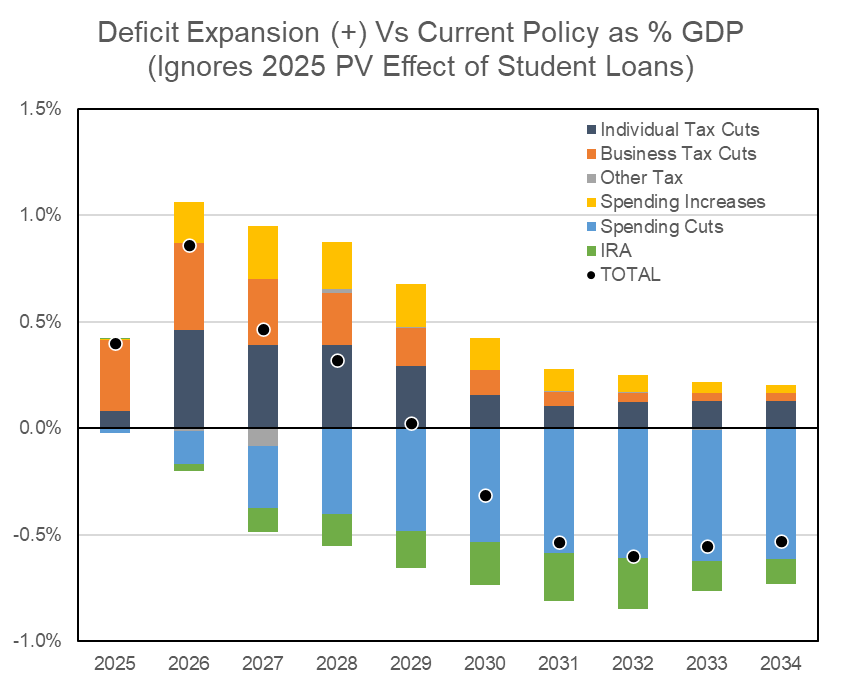

Here is, in my view, most economically appropriate way to think about OBBB. In FY25 it will expand deficit by 0.4% GDP relative to current policy and 0.86% in FY26. That is sequential expansion of 0.4% and 0.46% of GDP then fiscal tightening as cuts ramp

x.com/USCBO/status/1…

U.S. CBO@USCBO

Estimated Budgetary Effects of an Amendment in the Nature of a Substitute to H.R. 1, the One Big Beautiful Bill Act, Relative to the Budget Enforcement Baseline for Consideration in the Senate. cbo.gov/publication/61…

English