@borrowed_ideas It’s not a Hyperscaler. It’s a digital/social media company. It can’t compete with Amzn, Goog, Msft or even Orcl in the provision of cloud and or AI infrastructure and services.

English

Cristiano Souza

344 posts

@csouzaZEP

Compounding in life

$AMZN 1Q'26: Rosy Near-term but "Cloudy" Long-term

"My largest positions aren’t the ones I think I’m going to make the most money from. My largest positions are the ones where I don’t think I’m going to lose money." -- Joel Greenblatt

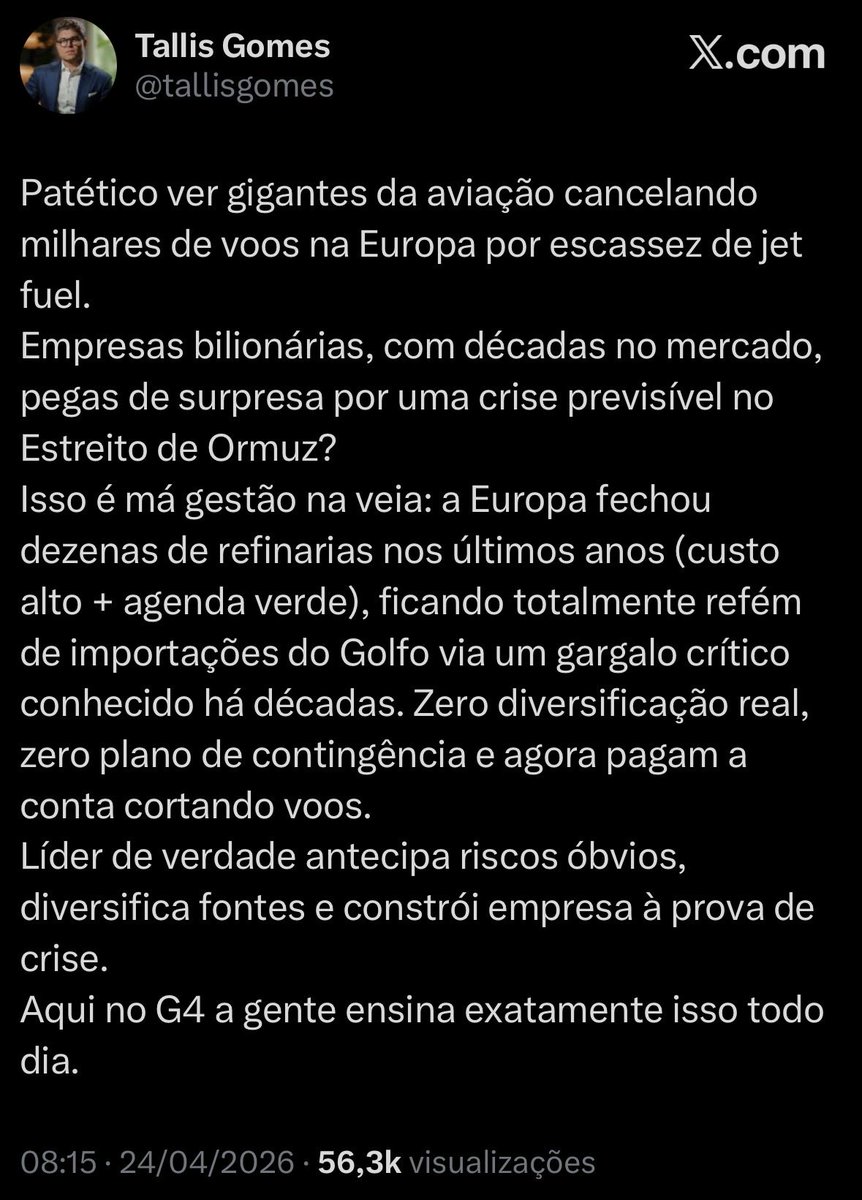

Nosso Tallis achando que tocar uma companhia aérea tem a mesma complexidade que vender curso pra incauto.

BREAKING: Japan will begin releasing part of its oil reserves from May 1, according to the Ministry of Economy, Trade and Industry (METI). 🔴 More on aljazeera.com

I have seen several times on my timeline people bemoaning $DHR targeting a "HSD Year 5 ROIC" on their recent acquisition of $MASI. The way DHR mgmt. phrased this was (unnecessarily) confusing. What DHR mgmt is saying is basically that they are paying a HSD year 5 unlevered FCF yield on the entry EV. If you add synergies to the acquired EBITDA in their merger model, you get to ~8% UFCF / entry EV of $9.9B, so that checks out. I'll illustrate below how economic returns could be high teens or better, much better than "HSD". But to simplify, DHR is paying roughly an equivalent EBITDA multiple for MASI, which they expect to compound earnings at a mid-high teens rate while throwing of a growing amount of FCF. So the economic value creation includes the contribution to DHRs EV from that growing EBITDA/FCF, plus the excess FCF, less what they paid. For simplicity im going to ignore leverage since we dont know at what rate $DHR will pay merger debt down or keep it outstanding.

$DHR projecting a HSD ROIC on the Masimo deal by the fifth year of ownership...Is this what Rainer means by "the financial model has to work"? I don't get it.

I have seen several times on my timeline people bemoaning $DHR targeting a "HSD Year 5 ROIC" on their recent acquisition of $MASI. The way DHR mgmt. phrased this was (unnecessarily) confusing. What DHR mgmt is saying is basically that they are paying a HSD year 5 unlevered FCF yield on the entry EV. If you add synergies to the acquired EBITDA in their merger model, you get to ~8% UFCF / entry EV of $9.9B, so that checks out. I'll illustrate below how economic returns could be high teens or better, much better than "HSD". But to simplify, DHR is paying roughly an equivalent EBITDA multiple for MASI, which they expect to compound earnings at a mid-high teens rate while throwing of a growing amount of FCF. So the economic value creation includes the contribution to DHRs EV from that growing EBITDA/FCF, plus the excess FCF, less what they paid. For simplicity im going to ignore leverage since we dont know at what rate $DHR will pay merger debt down or keep it outstanding.

$DHR should have been down more today for that deal. Management has lost the plot.

Análise: Campanha de Flávio pode ser impactada após determinação de Moraes cnnbrasil.com.br/eleicoes/anali…

*KEY NORTH SEA OIL PRICING WINDOW SEES 12 CARGO BIDS, NO OFFERS