dannny

228 posts

@whoisjoenathan @Hedgeye @zriboua massive net interest spread to pay off the loans that shouldve alr been marked down

English

$hnge on hiatus

cant get comfortable on yield growth and migraine demand

new SWORD M&A and OMDA also weak competitors

dannny@dannny56

$hnge update also overstated TAM (wrt yield & billings) + compression (churning off MSK entirely), diseconomies of scale, ramping comp + pricing headwind, commoditized offering

English

@ContrarianCurse yes esp with DOCW, workflows, and some of the expert call integrations

BQL formulas with the backend is a nice touch too with ASKB

English

@taobanker u have seen acquisitions partially for the sake of getting more $cat machines and ur bearing? ☹️

English

$cat is the new $wmt this shit is fucking dumb, michael burry is right on this one

Wagie Capital@WagieCapital

Everyone ragging on Burry for shorting $CAT but surely it is obvious this is not sustainable This chart will ultimately look similar to the 2021 bubble stocks that eventually retraced

English

$TDS: we remain long and are sharing a follow-up note at kerr.co/tds-2. Since our January report, earnings have been solid and thesis reaffirming. But it’s worth discussing what comes next 1/6

English

$qdel finally printing🙏

archive.is/xj5pS

bit lost on how to get a 10x EBITDA buyer on a declining PoC biz, but regardless, should rerate the labs biz better on fcf conversion, mix / margin improvements, less conflicts of interest (e.g. cannibalization)...

English

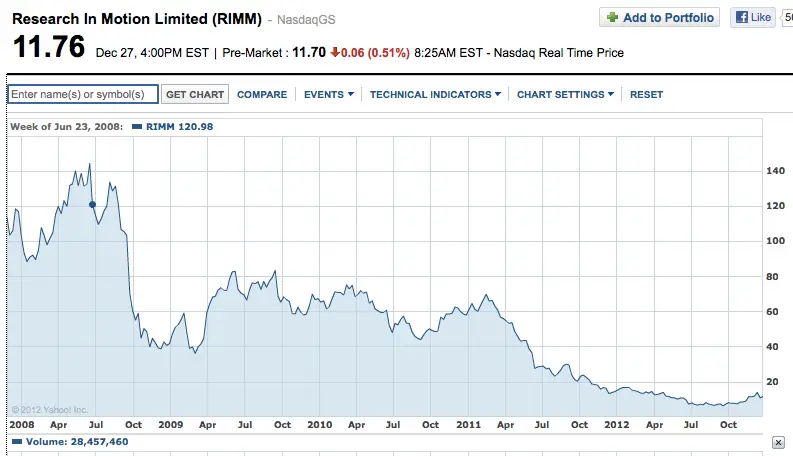

$RIM peaked at $147 per share in 2008. FY2011 results: revenue +33%, EPS +47%, crackberry shipments +43%. Revenue more than tripled, shipments quadrupled from 2008-11. Several managers dip buying all the way down saying fears overblown.

Everyone has a calculator.

JaguarAnalytics@JaguarAnalytics

$ADBE Fun fact: Adobe is now trading at 3.2x trailing 12-month sales and 8.9x earnings. In the past 3 years, its sales are up +38% and it has never posted a sequential QoQ decline in sales. Operating margins at 36% same as 3 years ago.

English

@ExcessDefaults fr the main reason mag 7 is down is bc of mem prices anyways

English

Gonna be another dark 5 years for value bros (always dark pour moi)

English

Following the reports from $1SXP, $WST, $BDX & $STVN, we now have the full context to judge each company’s results. $GXI is still having issues with their auditors or something along those lines. Honestly, I haven't bothered to look into it and I don't think it’s very relevant.

English

@kaladindz yes but sales != volumes. $wst has diff unit economics on pfs vs vials and rtu vs non-rtu.

English

@kaladindz $wst is elastomers; their PFS use $1sxp and $gxi glass. not rlly comparable

English

$MIAX has real operating leverage in its options-revenue segment through its Access & Market Data fees.

Biggest revenue segment is Transaction & Clearing fees (of which options) is 72% of total revenue BUT that 72% of revenue has a big cost attached to it- the net capture is $74m because the cost attached to that revenue is $223.m of liquidity payments (paid out as rebates to attract order flow).

The opportunity lies in Access & Market Data fees which are $46m - but this is basically 100% margin (36% of NET revenue) and grew at 45% YoY. This is where the real bull case is.

The exchange is already built, adding more transaction volume benefits from economies of scale.

As $MIAX continues to take options market share- in volume, the Access/Market Data fees increase and contribute directly to the bottom line.

If you look at the financial statements its nascent. There is a LOT of margin growth to happen vs other exchanges (this is a big part of the bull case).

The stock price is suffering due to technicalities (no not stupid line drawing) real stock technicalities- there is a massive stock overhang -the 180-day lock-up expired Feb 10, 2026, freeing ~80M pre-IPO shares to sell. That post-lock-up supply is the main driver of the slide from $57, and insiders are now selling (e.g., an EVP sold ~$0.67M).

Again, this is a technicality, not a fundamental issue with the underlying business. And I would say its more of an opportunity to buy a high quality, growing business, at a cheap price- not financial advice, just my opinion. I do own shares.

English