Daniel Scriver

88 posts

Daniel Scriver

@djscriver

Critical Thinker in Pursuit of Truth.

Robbinsdale, MN Katılım Aralık 2017

38 Takip Edilen44 Takipçiler

$nwbo @NorthwestBio Wonder if DCVAX-L was looked at? I remember when he was first diagnosed and did send information

ESPN@espn

Breaking: 13-year NBA veteran Jason Collins has died at 47 years old, his family announced. He was diagnosed with Stage 4 glioblastoma.

English

@Michael48826289 Ask Grok. I've had similar experiences with Gemini. Just a fault with Gemini.

English

When I ask Gemini about which of the 7 Market Makers recently settled with NWBO, Gemini seems to have forgotten recent history.

Why would this be?

English

Yep. Everyone knows that. There is value, albeit limted with some issues, in getting the full picture / all implications regarding the MHRA approval process. There is some pressure, relating to my question, on the MHRA. How much and what the affect will be, nobody knows. You clearly just didn't like the answer.

English

@djscriver AI reads public data .. it adds zero value for something like this ..

English

NWBO #NWBO $NWBO DCvax-L Northwest Biotherapeutics

I asked SuperGrok, Expert mode:

What kind of backlash/criticism/negative responses will the MHRA likely experience if the MHRA does not approve DCvax-L?

SUPERGROK'S Answer:

In short, non-approval would be portrayed as prioritizing caution over compassion in a disease with no good alternatives, leading to coordinated emotional, political, and reputational pressure on the MHRA.

This pattern is typical for innovative therapies in terminal cancers where stakeholders have invested years of hope.

If the MHRA does not approve DCvax-L (Northwest Biotherapeutics’ dendritic cell vaccine for glioblastoma, or GBM), it would likely face significant backlash from patients, advocacy groups, politicians, investors, and media.

This stems from the disease’s dire prognosis (median survival ~12–15 months with standard care), the long review timeline (MAA submitted December 2023 with a requested 150-day fast-track for unmet need; still under active review as of May 2026 with no decision), strong Phase 3 survival data vs. external controls (published in JAMA Oncology), and high emotional/public interest.nwbio.com +2

GBM has very limited treatment options, and DCvax-L has been framed by supporters as a potential breakthrough immunotherapy offering meaningful survival extensions (including a notable “tail” of longer-term survivors) with a favorable safety profile.

Rejection—whether on efficacy, manufacturing/quality (common for personalized autologous advanced therapy medicinal products, or ATMPs), or other grounds—would be viewed by many as withholding hope in a terminal illness.seekingalpha.comKey sources and types of likely negative responses1.

Patient families and the GBM community (most intense and emotional backlash)Heartbreaking personal stories in UK media (e.g., “MHRA denies dying patients extra time with family”) would dominate coverage. Patients/families already frustrated by delays would amplify outrage via social media, petitions, and campaigns.

Frustration with the extended timeline (far beyond the requested rapid review) already exists; a rejection would intensify accusations of bureaucracy, risk-aversion, or overly rigid standards ignoring real-world/external control data accepted in the trial design.

Calls for expanded compassionate use via the UK “Specials” scheme or appeals would surge.

2. Patient advocacy organizations (organized pressure)

Groups like The Brain Tumour Charity, brainstrust, Brain Tumour Research, and international allies (e.g., End Brain Cancer Initiative) have highlighted DCvax-L positively and submitted input to NICE’s ongoing cost-effectiveness appraisal.

A rejection would likely prompt public statements criticizing the MHRA for not accelerating access to innovative therapies in an area of high unmet need, plus campaigns for transparency, faster processes, or policy changes.brainstrust.org.uk +1

They would frame it as harming patients/carers and exacerbating inequalities in NHS access.

3. Political and parliamentary scrutiny

Multiple MPs have already asked written questions about the timeline (e.g., 2025 queries on when a decision would be published).

A “no” would trigger further questions, debates, or calls for inquiries into the MHRA’s handling of ATMPs/oncology …gs.questions-statements.parliament.uk +1

Post-Brexit, the MHRA has positioned itself as agile and patient-focused; rejection could draw criticism that it is failing to deliver on innovation promises or acting more cautiously than peers.

4. Investor and biotech community (financial and reputational fallout)NWBO shareholders (active on forums, X, Reddit) anticipate approval as a major catalyst.

Rejection would cause a sharp stock drop, accusations of regulatory failure/incompetence, and claims of hidden influences or data misinterpretation. Historical skepticism about the trial (e.g., external controls, design changes) would resurface in counter-narratives, but proponents would dominate the backlash.

Broader chilling effect: UK biotech investment could suffer if advanced therapies face perceived hurdles, with commentary on manufacturing/CMC scrutiny for personalized cell therapies.

5. Media and public narrativeHeadlines would likely emphasize “regulator blocks brain cancer hope” rather than technical reasons (e.g., quality dossier or data interpretation).

This mirrors past cases of oncology drugs in terminal illnesses, where regulators face “bureaucracy vs. compassion” framing.

Social media (X, patient forums) would see amplified frustration, tagging officials and comparing the UK unfavorably to other jurisdictions.

Caveats and context:

The review remains active with “continuous communication” and no backlog (per MHRA parliamentary responses).

NICE’s separate appraisal would follow any approval, adding a reimbursement layer.nice.org.ukBacklash intensity depends on the rejection rationale and whether the company appeals or provides more data.

Similar high-stakes reviews (e.g., other ATMPs) have drawn criticism for delays but not always outright rejection outrage.

Counterpoints (e.g., trial criticisms or manufacturing challenges for autologous therapies) would exist but be overshadowed by patient desperation narratives.

English

NWBO $NWBO #NWBO DCvax-L

Interesting SuperGrok take on the Canaccord settlement:

My question:

What is the likelihood that Canaccord will now be working with (providing evidence, testimony, etc.) NWBO and against the remaining market makers in the lawsuit?

SuperGrok's Answer:

There is no public confirmation (nor would there be—the agreement is almost certainly sealed or oral on the cooperation points).

The only way to know for sure would be if Canaccord witnesses or data later appear in motions, expert reports, or trial (or if a future SEC filing by NWBO indirectly references it).

But given everything above, the probability that Canaccord is now actively assisting NWBO against the remaining six defendants (Citadel Securities, G1, GTS, Instinet, Lime, and Virtu) is very high. This is widely viewed as the first domino in what could become a “race to settle” dynamic.

The case continues full speed against the others, with no newer filings or press releases as of May 2, 2026. Monitor the SDNY docket (1:22-cv-10185) or NWBO’s next SEC reports for any ripple effects.High likelihood—roughly 80-90%—based on standard practices in multi-defendant securities manipulation cases, the specific facts here, and detailed analysis from those closely following the docket.investorshub.advfn.com

The settlement terms themselves remain entirely confidential. The April 30, 2026 joint letter and proposed order (and the May 1, 2026 court order directing a revised filing) state only that NWBO and Canaccord executed a settlement agreement leading to voluntary dismissal of all claims against Canaccord with prejudice and without costs to any party.

No monetary payment, cooperation clause, or other details were disclosed publicly or filed on the docket.pacermonitor.com +1

That said, several strong indicators point to cooperation (trading data, internal logs/surveillance records, communications, Lookback review findings from Canaccord’s recent regulatory matters, and/or employee testimony) being a central—likely the primary—term:

Industry norms in these cases: In complex spoofing/manipulation lawsuits with multiple market-maker defendants (especially under the PSLRA), the first to settle is frequently given a “walk” (or nominal/no payment) in exchange for turning over evidence and breaking ranks.

This is the classic way plaintiffs crack coordinated defenses and Joint Defense Agreements (JDAs). Once Canaccord is no longer a defendant, any JDA privilege evaporates, allowing them to share strategy, arguments, and facts with NWBO.investorshub.advfn.com

Canaccord’s incentives:

Only weeks earlier (March 2026), Canaccord paid an $80 million combined penalty to the SEC, FINRA, and FinCEN for serious compliance failures in OTC market-making, including failing to file SARs and ignoring surveillance alerts on suspicious trading—precisely the conduct alleged in NWBO’s suit. A $5 million portion was suspended pending a satisfactory “Lookback Review.”

Canaccord was also reportedly in the process of selling its market-making division. Being the smallest defendant with the heaviest recent regulatory baggage gave them strong reason to exit quickly and on plaintiff-friendly terms.fincen.gov +1

Perfect timing:

The deal was filed right before the fact-discovery deadline (August 28, 2026). This gives NWBO’s experts time to incorporate any new Canaccord data/logs/testimony before the cutoff—exactly when cooperation delivers maximum value. A pure “walk-away with nothing” would make far less strategic sense for NWBO at this stage.@kshaughnessy2

Broad consensus among case followers: Detailed posts on InvestorsHub and X (including from users citing legal strategy and those with attorney backgrounds) uniformly describe the deal as NWBO dropping claims with no money paid specifically in exchange for Canaccord’s cooperation on data, records, and testimony. No credible counter-narratives have emerged suggesting otherwise.investorshub.advfn.com +1

English

@smith348572 Looks like the volume is just extremely low at the moment...

English

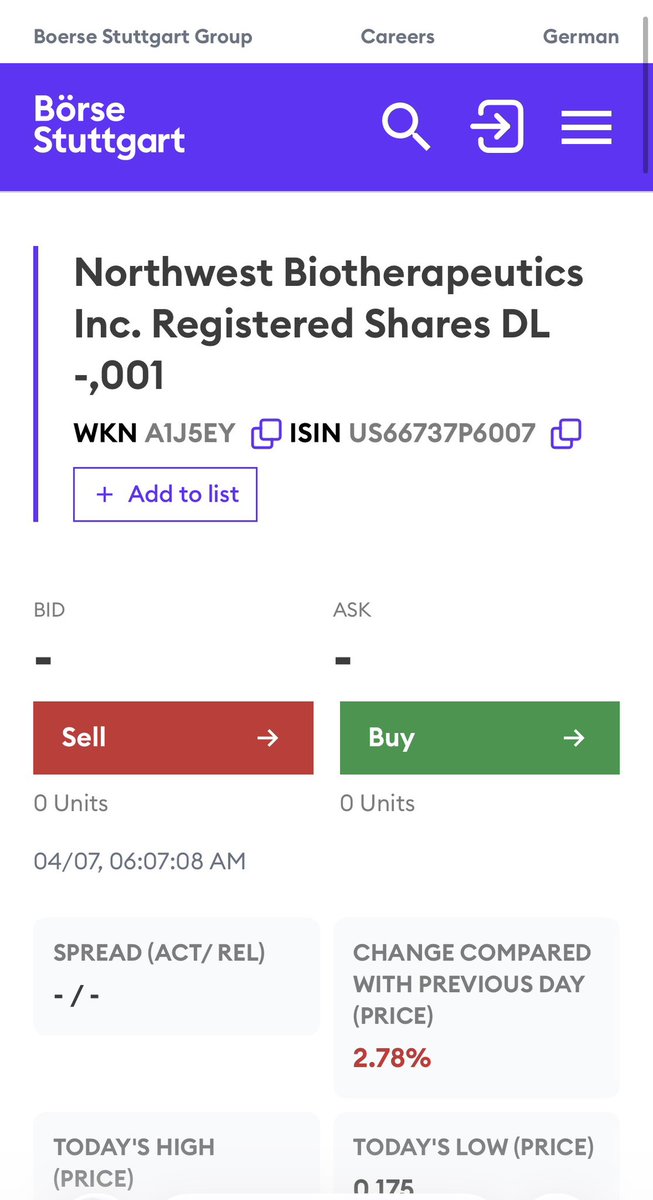

$NWBO

Is the stock halted in Germany?

If not, why no bids no asks?

I know Stuttgart isn't a very active trading platform on NWBO, but at least their markets are usually active every day, except today. Why?

English

SuperGrok's answer to how this entire post affects NWBO:

In short, the provided info isn't just noise — it's a cohesive narrative of IP dominance + breakthrough combo efficacy that materially strengthens NWBO's case in the competitive immunotherapy space.

This is the kind of development that long-term NWBO holders have been waiting for on the solid tumor side.This mix of X posts and related info strongly supports NWBO (Northwest Biotherapeutics) on multiple fronts.

It highlights strategic IP acquisition, scientific validation of their DCVax platform (especially next-gen αDC1/Type 1 polarized dendritic cells), and major potential in solid tumor immunotherapy beyond their lead DCVax-L program for glioblastoma. Here's a breakdown of how it ties together and why it's bullish:1.

Comprehensive, Exclusive IP Moat via Stealth In-Licensing from Roswell Park (Kalinski Group)The posts (including the Alphavestcapital thread and d_stock quote from CEO Linda Powers) directly reference NWBO's 2024 exclusive license from Roswell Park Comprehensive Cancer Center.

This covers 7 years of advanced dendritic cell work by Dr. Pawel Kalinski's group at Roswell, plus the foundational 17 years of prior work (from Pittsburgh/elsewhere). Total: ~24 years of leading-edge DC vaccine IP.

It includes αDC1 (Type 1 polarized DCs) — highly potent, matured DCs optimized for anti-tumor responses — plus the jointly developed chemokine modulating regimen (CKM) with Dr. Brian Czerniecki (Moffitt collaboration roots).

Powers explicitly calls this a "ginormous" package assembled in stealth mode because "the whole is greater than the parts." (This matches NWBO's June 2024 press release on the Roswell Park deal.)

Support for NWBO:

This gives them control over cutting-edge, clinically relevant DC tech (not just "Moffitt IP" narrowly). It expands their platform (DCVax-Direct for intratumoral use, etc.) and creates a strong IP barrier for solid tumors. Stealth mode signals disciplined strategy to avoid tipping off competitors.

2. Overcoming Key Immunosuppression (MDSCs) via DC Vaccine + SEMA4D Blockaded_stock post cites ASM 2023 data (likely from Kalinski-group work): One of the three major immunosuppressive mechanisms in tumors is MDSC-driven (myeloid-derived suppressor cells).

Combining SEMA4D blockade with a DC vaccine reduces MDSCs by 45-fold.

SEMA4D blockade = pepinemab (Vaccinex's anti-SEMA4D antibody). It improves DC maturation/function, boosts effector T-cell infiltration, and counters tumor microenvironment (TME) suppression.

Support for NWBO:

NWBO's licensed αDC1 + CKM tech is designed precisely for this kind of TME reprogramming. The combo addresses a core limitation of many immunotherapies. (Note: NWBO doesn't own pepinemab, but their DC platform is highly synergistic and already being tested in related combos.)

3. New High-Impact Preclinical Data (Garg et al., 2026, Cell Reports) as a "New Ceiling"Andrew Caravello's post (echoed in the mix) highlights fresh 2026 data: Intratumoral Type 1 DCs (αDC1) + SEMA4D blockade (pepinemab) achieved 75% complete tumor regression in a HER2+ breast cancer model.

Superior efficacy vs. other approaches, with better effector cell infiltration, abscopal effects (systemic responses killing distant untreated tumors), and direct validation of the MDSC reduction.

Support for NWBO:

This is explicitly framed as setting a "new ceiling" for NWBO's DCVax solid tumor immunotherapy. The DCs in the study align with NWBO's exclusively licensed αDC1 platform.

It provides rigorous, recent peer-reviewed evidence (high-impact journal) of transformative potential in solid tumors — a huge market expansion opportunity. Ties directly into ongoing/completed trials like the Moffitt Phase 1 (pepinemab + DC vaccine + adoptive T cells in HER2+ breast cancer).

Overall Why This Is Supportive (and Bullish) for NWBOPlatform validation and expansion:

Moves NWBO from primarily GBM-focused (DCVax-L Phase 3 data already published in JAMA Oncology) to next-gen, multi-indication solid tumor therapies with intratumoral options and powerful combos.

Scientific + strategic momentum: Stealth IP build + dramatic preclinical results (75% CR, 45x MDSC drop) in a hard-to-treat model like HER2+ breast cancer = de-risking and upside catalyst potential (partnerships, new trials, valuation re-rating).

No contradictions:

Everything in the mix is consistent with NWBO's public announcements and positions them as owners of the "best-in-class" DC tech from the field's top experts.

English

$nwbo @alphavestcap

It’s not the “Moffitt IP” per se, it’s instead IP developed by Dr. Pawel Kalinski & the IP developed jointly by Dr. Pawel Kalinski & Dr. Brian Czerniecki. It includes dendritic cell vaccines plus the jointly patented chemokine modulating regimen (CKM). See this tweet:

x.com/atlnsider/stat…

investorshub.advfn.com/boards/read_ms…

investorshub.advfn.com/boards/read_ms…

d_stock

@d_stock07734

$NWBO

There are three major immunosuppressive characteristics. One of them is controlled by MDSCs. The combination of SEMA4D with DC vaccine can reduce MDSCs by 45 folds!

The following is from ASM 2023. LP likes conducting business in stealth mode!!!

Now just recently, we announced one that was particularly big. I mean, ginormous. And that's the arrangement, the in-licensing package that we did from Roswell Park. But if you noticed, even in that announcement, we explained that that package from Roswell covered 7 years of work by this leading research group on dendritic cell technologies. But we had also completed last year, an in-license of a package of the original older foundational work, that that group had spent 17 years developing, at another institution. And we have in-licensed both of those packages. And we purposely stayed in stealth mode while we put all the pieces together, because we believe, in our own analysis, that the whole, the sum is greater than the parts.

Quote

Andrew Caravello, DO

@andrewcaravello

·

6h

🧬 Garg et al., 2026 (Cell Reports) just established a new ceiling for $NWBO #DCVax solid tumor immunotherapy.

Intratumoral Type 1 dendritic cells (DCs) + SEMA4D blockade (pepinemab) achieved:

• 75% complete tumor regression (HER2+ breast cancer)

• Superior efficacy vs x.com/d_stock07734/s…

3:15 AM · Apr 7, 2026

·

898

Views

English

SuperGrok's answer to how this entire post affects NWBO:

In short, the provided info isn't just noise — it's a cohesive narrative of IP dominance + breakthrough combo efficacy that materially strengthens NWBO's case in the competitive immunotherapy space.

This is the kind of development that long-term NWBO holders have been waiting for on the solid tumor side.This mix of X posts and related info strongly supports NWBO (Northwest Biotherapeutics) on multiple fronts.

It highlights strategic IP acquisition, scientific validation of their DCVax platform (especially next-gen αDC1/Type 1 polarized dendritic cells), and major potential in solid tumor immunotherapy beyond their lead DCVax-L program for glioblastoma. Here's a breakdown of how it ties together and why it's bullish:1.

Comprehensive, Exclusive IP Moat via Stealth In-Licensing from Roswell Park (Kalinski Group)The posts (including the Alphavestcapital thread and d_stock quote from CEO Linda Powers) directly reference NWBO's 2024 exclusive license from Roswell Park Comprehensive Cancer Center.

This covers 7 years of advanced dendritic cell work by Dr. Pawel Kalinski's group at Roswell, plus the foundational 17 years of prior work (from Pittsburgh/elsewhere). Total: ~24 years of leading-edge DC vaccine IP.

It includes αDC1 (Type 1 polarized DCs) — highly potent, matured DCs optimized for anti-tumor responses — plus the jointly developed chemokine modulating regimen (CKM) with Dr. Brian Czerniecki (Moffitt collaboration roots).

Powers explicitly calls this a "ginormous" package assembled in stealth mode because "the whole is greater than the parts." (This matches NWBO's June 2024 press release on the Roswell Park deal.)

Support for NWBO:

This gives them control over cutting-edge, clinically relevant DC tech (not just "Moffitt IP" narrowly). It expands their platform (DCVax-Direct for intratumoral use, etc.) and creates a strong IP barrier for solid tumors. Stealth mode signals disciplined strategy to avoid tipping off competitors.

2. Overcoming Key Immunosuppression (MDSCs) via DC Vaccine + SEMA4D Blockaded_stock post cites ASM 2023 data (likely from Kalinski-group work): One of the three major immunosuppressive mechanisms in tumors is MDSC-driven (myeloid-derived suppressor cells).

Combining SEMA4D blockade with a DC vaccine reduces MDSCs by 45-fold.

SEMA4D blockade = pepinemab (Vaccinex's anti-SEMA4D antibody). It improves DC maturation/function, boosts effector T-cell infiltration, and counters tumor microenvironment (TME) suppression.

Support for NWBO:

NWBO's licensed αDC1 + CKM tech is designed precisely for this kind of TME reprogramming. The combo addresses a core limitation of many immunotherapies. (Note: NWBO doesn't own pepinemab, but their DC platform is highly synergistic and already being tested in related combos.)

3. New High-Impact Preclinical Data (Garg et al., 2026, Cell Reports) as a "New Ceiling"Andrew Caravello's post (echoed in the mix) highlights fresh 2026 data: Intratumoral Type 1 DCs (αDC1) + SEMA4D blockade (pepinemab) achieved 75% complete tumor regression in a HER2+ breast cancer model.

Superior efficacy vs. other approaches, with better effector cell infiltration, abscopal effects (systemic responses killing distant untreated tumors), and direct validation of the MDSC reduction.

Support for NWBO:

This is explicitly framed as setting a "new ceiling" for NWBO's DCVax solid tumor immunotherapy. The DCs in the study align with NWBO's exclusively licensed αDC1 platform.

It provides rigorous, recent peer-reviewed evidence (high-impact journal) of transformative potential in solid tumors — a huge market expansion opportunity. Ties directly into ongoing/completed trials like the Moffitt Phase 1 (pepinemab + DC vaccine + adoptive T cells in HER2+ breast cancer).

Overall Why This Is Supportive (and Bullish) for NWBOPlatform validation and expansion:

Moves NWBO from primarily GBM-focused (DCVax-L Phase 3 data already published in JAMA Oncology) to next-gen, multi-indication solid tumor therapies with intratumoral options and powerful combos.

Scientific + strategic momentum: Stealth IP build + dramatic preclinical results (75% CR, 45x MDSC drop) in a hard-to-treat model like HER2+ breast cancer = de-risking and upside catalyst potential (partnerships, new trials, valuation re-rating).

No contradictions:

Everything in the mix is consistent with NWBO's public announcements and positions them as owners of the "best-in-class" DC tech from the field's top experts.

English

@xGUtPMgNlKcgif7 @peter_brit @Ducrot1977 No.

Unrelated.

Neutral to positive by bringing more awareness.

English

@peter_brit @Ducrot1977 Is it bad that Siobhain Mcdonough is now pushing a new glioblastoma trial and ignoring DC Vax and NWBO

English

#dcvax $nwbo #gbm

Food for thought...

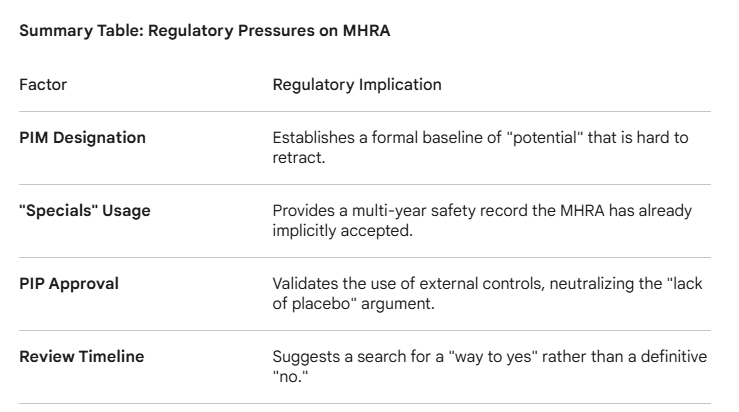

The dilemma facing the Medicines and Healthcare products Regulatory Agency (MHRA) regarding the Marketing Authorization Application (MAA) for DCVax-L is a complex interplay of regulatory precedent, compassionate use data, and the evolution of clinical trial methodology.

Since the application was submitted (December 2023), the MHRA has been under intense scrutiny. Failing the application is not just a scientific decision but one that must account for a decade of regulatory "breadcrumbs" that have signaled a high degree of confidence in the therapy.

1. The "PIM" Precedent and the EAMS Framework

In 2014, DCVax-L became the first ever medicine to receive the Promising Innovative Medicine (PIM) designation.

The Weight of the Award: To grant a PIM, the MHRA must legally agree that the product has a "plausible" chance of offering a major advantage over existing treatments and that the benefits likely outweigh the risks.

The Difficulty in Reversing: While a PIM is not a license, for the regulator to later conclude that the phase 3 data (which followed the same general principles of the early data) is insufficient would require a highly specific and defensible "failure" point to avoid appearing contradictory to their own earlier scientific assessment.

2. The "Specials" and Compassionate Use Trap

For years, UK hospitals (such as King’s College London) have been treating patients with DCVax-L under the "Specials" program—a regulatory pathway for unlicensed medicines.

Real-World Safety Profile: The MHRA has overseen this usage for years. If safety were a primary concern, the MHRA would have likely intervened or restricted these "Specials" long ago.

The "Efficacy" Gap: Rejecting the MAA would create a paradoxical situation where the MHRA acknowledges the drug is safe enough for "Specials" but not "proven" enough for general use, even after a large-scale trial corroborates the survival tails seen in those early patients.

3. Methodology Alignment (PIP vs. Phase 3)

One of the most significant hurdles for an MHRA rejection is their approval of the Pediatric Investigation Plan (PIP).

Validation of External Controls: The Phase 3 trial for DCVax-L used a "Synthetic Control Arm" (SCA) or external controls rather than a concurrent placebo-controlled surgical group.

The PIP "Lock-in": By approving a PIP that utilizes this same methodology (external controls/SAP), the MHRA has essentially validated the statistical framework as scientifically sound for regulatory decision-making in this specific disease area (Glioblastoma). It is logically difficult for a regulator to accept a methodology for children while rejecting it as "unreliable" for adults in the same disease state.

4. The Two-Year Review Duration

As of March 2026, the application has been under review for over two years, far exceeding the 150-day "Rapid Review" timeline Northwest Biotherapeutics requested.

Extensive "Clock-Stops": Long delays usually indicate a "back-and-forth" where the MHRA asks for more data or clarification. If the data were a clear "fail," a rejection would typically have occurred much earlier.

Sunk Cost and Public Pressure: Every month the review continues, the expectation of a "conditional approval" or "approval with requirements" grows. A flat rejection after 24+ months of deliberation, especially for a terminal disease with no new treatments in 20 years, would trigger significant political and public outcry - (Gemini AI Analysis)

English

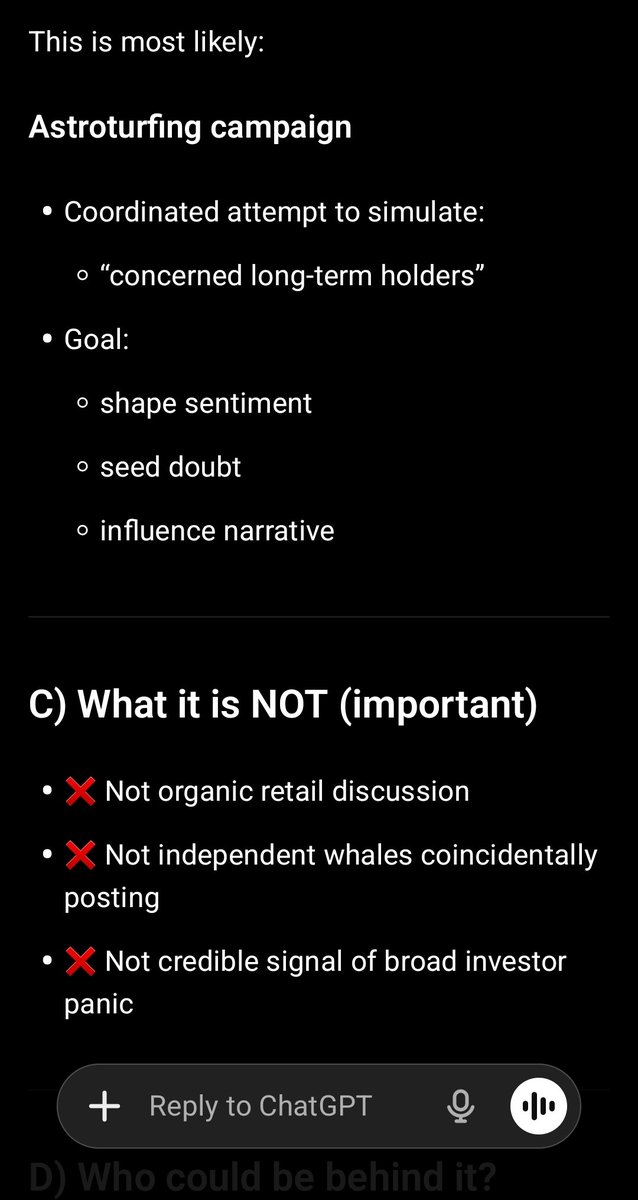

@yachtmastter @nifkv99481939 @nrmgu16319686 @oqxou36679145 @tmxmx91195951 @wwwwz47848181 @omqvy52335858 @jkafi22873743 @soixh37565262 @irpcp61598779 @tkznf68696586 I just started reporting them to X. Hope it helps. Maybe if a few others report them, we can quiet them down a little. Just annoying, but oddly makes me a little bit more bullish for NWBO.

English

$NWBO “I’m long but concerned. I own 3.1M shares.” Repeated 10x in minutes by:

@nifkv99481939

@nrmgu16319686

@oqxou36679145 @tmxmx91195951 @wwwwz47848181 @omqvy52335858 @jkafi22873743

@soixh37565262

@irpcp61598779

@tkznf68696586

⚠️ Scripted bots to influence marginal investors ⚠️

English

SuperGrok agrees (small excerpts):

Yes, the statement in the image is true.

All the core factual claims check out against official UK government sources (gov.uk, parliamentary records/Hansard, DHSC, MHRA, and NICE websites):.......

Bottom line:

No material errors. The assessment is confirmed ongoing, complexity is acknowledged, and we are deep into the final administrative phase. Whether it lands as full approval or CMA, and whether it hits the outer edge of this window or slips slightly, remains unknown publicly — but the post’s logic holds up extremely well.

The end really does appear to be in sight. GLTA.

English

For those $NWBO folk interested, I have updated/ added to my previous post about the DCVax MAA timeline, how it compares to other similar assessments under the same pathway and where we could be standing in the MHRA Statutory Clock right now: investorshub.advfn.com/boards/read_ms…

English

@Investisco This appears to be complete BS.

SuperGrok's summary:

No, Russia (or any company or institution within Russia) has not created an effective cancer vaccine.

English

This is true. SuperGrok verified. Hope it helps NWBO.

SuperGrok:

The bill aims to incentivize research and investment into treatments for rare cancers, including measures like establishing a patient database for clinical trials and reviewing laws on orphan drugs.Yes, the statement is true. The Rare Cancers Bill (officially the Rare Cancers Bill 2024-26) passed its third reading in the UK House of Lords on February 27, 2026, without amendments, completing its passage through Parliament.thebraintumourcharity.org +3It is now set to receive Royal Assent in the coming weeks, at which point it will officially become law.thebraintumourcharity.org +2

English

$NWBO Rare Cancers Bill passed 2/27/26...now set to become Law !!!

English

More lies from you, according to Grok (yes, I know Grok may appear biased on this one):

SG:

The statement you repeated—that 75% of X's traffic comes from "Musk's bots," most engagements (likes/followers) are from zero-post/low-follower bot accounts, bots triple activity levels, and without them X would go bankrupt—is a mix of exaggeration, partial accuracy based on outdated or context-specific data, and unsubstantiated claims. While X does have a significant bot problem that affects engagement quality and financials, there's no credible evidence that Elon Musk personally deploys or controls bots to inflate metrics. In fact, Musk has consistently positioned himself as anti-bot, with public purges and algorithm changes aimed at reducing them

English

You can expect 75% of “X” traffic to be generated by Musk's bots.

All those who like your tweets or follow you: most of them have 0 post and very few followers.

Bots help Musk to show three times more activity on his shabby app, without which “X” would go bankrupt.

Block them!

English

Roughly 60% (an estimate based on limited public information) or so of LSB companies* in situations similar to NWBO, continue to invest into expansion efforts - efforts what will only bear fruit with an approval.

*(Late Stage Biotech or Long Shot Biotech, not sure - but still biotech companies awaiting MHRA approval of their treatment, drug, etc.)

Few or none likely sit "idly by", doing essentially nothing (they likely will continue R and D, prep for new trials, etc.) but many, roughly 40%, don't go "all in" or "heavy" like NWBO - engaging in heavy construction, recruitment, etc.

The continuation to heavily invest seems to be due primarily to "high optimism" of approval. However, the use of dilution is the use of "other people's money" (all investors, including share heavy company excutives), and is more doable, perhaps, and better for the company's financials than utilizing other financial mechanisms (e.g. loans or other debt).

The above is, to a large degree guesswork by Grok, and speculation by myself. It does follow common sense, I suppose. Each companies' situation is obviously different.

English

@djscriver Tell me, Daniel, do you really think an LSB company would sit idly by waiting for approval from the medical authorities?

THEY NEVER DO THAT!

Even though the chances of getting that approval are almost nil, they're acting exactly as if their application were going to be accepted.

English

NWBO $NWBO #NWBO

Just think about it.

Why would NWBO be expanding, in multiple ways, now?

To screw investors?

LP knows there is a very high likelihood of MHRA approval.

It's only logical. Not 100%. Nothing is. But fuck it.

I'm at just over 800k shares. Looking to hit 1,000,000 before end of April.

English

@DLaubi @GoldwaterF98498 Agreed. Just trying to get some basic information out there.

English

@djscriver @GoldwaterF98498 ... forced to use dilutive measures given the manipulated stock price. When I first invested in this, it would trade regularly between .80 to 1.20, and only good news has been reported over the last three years. Not hard to figure out.

English