Marks

376 posts

We’re back tonight!

LIVE Episode 59. Waiting for the World to Catch Up

We’re on in 2.5 hours. We’ve been cooking, excited to share.

True North@MSTRTrueNorth

⚡Brand New Episode Tonight📷 10pm EST / 7pm PST True North Episode 59 - Waiting For The World To Catch Up Agenda: - Trading Volume - Bank Balance Sheets - Bad Bonds - Building on Prefs - Efficiency of Transactions

English

🔥STRATEGY WILL BE THE WORLD'S MOST VALUABLE COMPANY - BY FAR🔥

Strategy bulls need to understand how insane this 10-year balance sheet model actually is.

I modeled a simple cadence. We just saw two weeks of some awesome capital raising with MSTR/STRC, didn't we?

So going foward, let's assume this:

Every 4 weeks, Strategy raises capital at the same MSTR / STRC ratio as the last two Bitcoin buy announcements.

But only for 2 weeks out of the month.

The other 2 weeks are dead, zero capital raised, full cool-off, full return-to-par window.

No infinite ATM fantasy. No permanent intravenous dilution drip for the spreadsheet autists to cry about.

Half the month, the machine is literally OFF.

Then I assume:

Bitcoin grows 25% per year,

STRC preferred issuance grows 5% month over month,

and all proceeds go into Bitcoin.

Starting point in the model - March 2026:

Bitcoin NAV = $54.7B

Enterprise value = $65.1B

Preferred outstanding = $10.0B

Debt outstanding = $8.2B

At the start, pref is 15.4% of EV and debt is 12.6% of EV.

That is where the bears freeze the frame and start hyperventilating into a paper bag.

Now watch what happens when time passes and the engine keeps doing what it’s doing.

By March 2027:

Bitcoin NAV = $119.2B

EV = $141.9B

Pref = $34.8B

Debt = $8.2B

So after one year, Bitcoin NAV has more than doubled.

Preferred gets bigger, yes.

But debt as a share of EV gets chopped from 12.6% down to 5.8%.

That is the first humiliation ritual.

The liabilities did not disappear. They got outgrown.

By March 2028:

Bitcoin NAV = $240.2B

EV = $285.9B

Pref = $79.4B

Debt = $8.2B

Now debt is just 2.9% of EV.

So the company goes from “look at all that debt!!!” to “that debt is becoming decorative.”

It starts to look less like a capital structure problem and more like a historical artifact preserved in amber for future MBA students to misinterpret.

By March 2029:

Bitcoin NAV = $464.1B

EV = $552.3B

Pref = $159.4B

Debt = $7.2B

Now debt is just 1.3% of EV.

The debt stack is basically entering hospice care at this point.

By March 2030:

Bitcoin NAV = $874.4B

EV = $1.04T

Pref = $303.2B

Debt = $1.4B

Debt drops to 0.13% of EV.

Read that again.

0.13%.

The convert stack has effectively been vaporized by scale.

Not because someone performed magic, but because a growing Bitcoin asset base plus disciplined capital intake makes the fixed liabilities look microscopic.

By March 2031:

Bitcoin NAV = $1.62T

EV = $1.93T

Pref = $561.4B

Debt = $0.8B

Debt is now 0.04% of EV.

At this point, talking about the converts as the central bear case is like warning the public that a trillion-dollar fortress may be threatened by a garden hose.

By March 2032:

Bitcoin NAV = $2.98T

EV = $3.54T

Pref = $1.03T

Debt = $0.8B

Debt falls to 0.02% of EV.

Then by March 2033, debt is basically gone in the model, while:

Bitcoin NAV = $5.42T

EV = $6.45T

Pref = $1.86T

And here is the really important part:

The preferred stack does get enormous in dollar terms.

But as a percentage of EV, it does not spiral into insanity.

It rises from 15.4% at the start to roughly:

24.5% in 2027

27.8% in 2028

28.9% in 2029

29.1% in 2030

29.1% in 2031

28.9% in 2032

28.8% in 2033

28.6% in 2034

28.5% in 2035

28.4% in 2036

That means the preferred layer becomes large, but it stabilizes.

The model is not saying pref eats the company alive.

The model is saying pref becomes a scalable capital intake layer while the Bitcoin asset base outruns it hard enough to keep the structure stable.

By March 2034:

Bitcoin NAV = $9.84T

EV = $11.71T

Pref = $3.35T

By March 2035:

Bitcoin NAV = $17.8T

EV = $21.18T

Pref = $6.04T

By March 2036:

Bitcoin NAV = $32.12T

EV = $38.22T

Pref = $10.86T

Now obviously the model becomes physically absurd because BTC held would mathematically run past available supply around 2034.

That matters.

It means the model stops being a literal forecast and starts becoming a demonstration of system pressure.

And that is even more bullish. What do you think happens to the Bitcoin price?

Because the thing that breaks first is not debt.

It is not preferred.

It is Bitcoin scarcity.

The structure survives the stress test better than the asset supply does.

That is psychotic. That is bullish.

That is the part the market still does not understand.

Under this framework, Strategy is slowly replacing maturity risk with perpetual capital, refinancing anxiety with preferred demand, and fragile liabilities with an expanding Bitcoin fortress.

Again, this is with a built-in 2-week monthly cool-off.

Half the month, nothing happens.

No raising. No nonstop aggression.

Just a reset period.

And even with that restraint, the numbers get grotesque:

Bitcoin NAV: $54.7B to $32.1T

Debt % of EV: 12.6% to basically 0%

Pref % of EV: 15.4% to a stable high-20s range

So the real story is not “wow, look how much pref they issued.”

The real story is they are building a balance sheet where debt dies, preferred scales, Bitcoin compounds,

and scarcity becomes the bottleneck.

That is not a normal company.

That is a corporate absorption machine wearing a public equity costume while half the analyst class stands outside with a clipboard trying to calculate book value like it’s still the Bush administration.

English

@HurdleRatePod 🚀🚀🚀The points made lately by @PunterJeff on total addressable market are blowing my mind.🤯🤯🤯

English

Welcome Back to The Hurdle Rate.

Episode 51: A Digital Credit Treasury

The crew is back this week and focuses primarily on an update around Strive ASST & SATA, breaking down the latest developments. They also touch on Strategy’s latest buy and what it could signal. Here's the latest with

@TimKotzman, @ColeMacro, @PunterJeff and @Werkman .

0:00 - Welcome Back to The Hurdle Rate

0:36 - Strive ASST & SATA Update

49:14 - Strategy’s Latest Buy

English

@BTCoptioneer IMO: Strive is a very articulate, & intelligent team. They are transparent, adaptable, & innovative, higher on the risk curve compared with MSTR, yet they are also positioned for more explosive growth. Like a Metaplanet, but without the fog of a foreign market. $MSTR $ASST 🚀🚀🚀

English

Strive is amplified Strategy

$ASST up 39% in 1 month

$MSTR up 19%

I am not a fan of ASST at 1x mNAV but if the mNAV drops below 0.9x, I will absolutely add to my position

English

@PunterJeff @notthreadguy @saylor Excellent content. The iPhone comparison in the last few minutes of the interview is a great way to put the addressable market in perspective

English

Virtual stream with @notthreadguy today considering "the full implications of @saylor being right"

I break down $STRC & $SATA from a basic level.

- How'd we get here

- How does this work

- How to think about these instruments

- How much capital can buy these?

Tune in:

0:50 – Intro

1:48 – Reinsurance to Bitcoin treasury

4:56 – BTC Treasury history, post-2021 unwind

7:42 – Perpetual preferred equity launch (STRK/STRC)

10:44 – High yields (11.5–12.75%) vs. bank preferreds

13:37 – Underwriting Bitcoin, long-term 25–45% CAGR

15:21 – Backtesting the yield model; excess risk/return

19:37 – Liquidity advantage $STRC trades 100x+ more than JPM

22:43 – Targeting trillions in fixed-income capital

25:58 – Low dividend-risk probability vs. credit market

28:30 – Preferred = low-vol BTC; common = high-vol/amplified BTC

30:08 – High volume enabling ATM liquidity

36:32 – Strive lower leverage (1%) vs. Strategy (12%)

39:03 – Capital raising & maintaining credit profile

41:37 – Massive TAM (200–300T fixed income)

43:41 – Host recap: cool product, new capital access thesis

threadguy@notthreadguy

few are considering the full implications of michael saylor being right

English

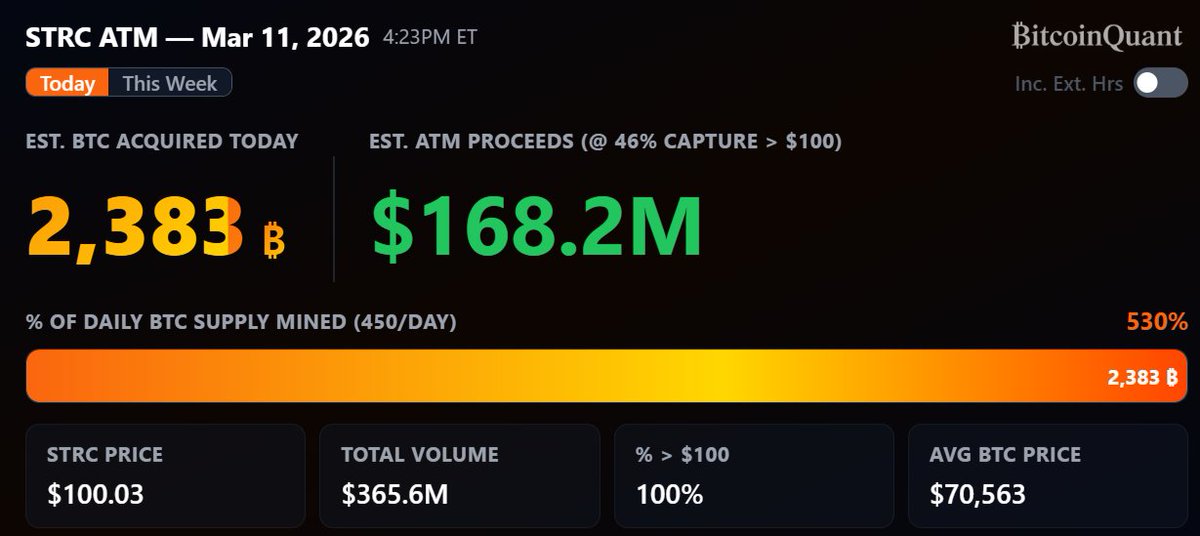

DID STRATEGY JUST RAISE $572 MILLION IN ONE DAY?

And they're probably still selling STRC after hours LOL

But that's another $168.2 million from STRC.

Last week's MSTR capital raised was 2.4x STRC.

Stands to reason that means ~$403.7 MILLION was raised from MSTR today ASSUMING they are keeping amplification the same.

$403.7m + $168.2m = ~$572 MILLION.

These numbers are crazy, especially if they were actually able to sell that much MSTR.

That'd be 18.9% of all the MSTR trading volume today.

If they didn't sell that much MSTR, well that just means your Bitcoin amplification with MSTR is just going higher.

THIS IS THE GREAT BITCOIN SINGULARITY.

English

I honestly foresee STRC and SATA having to throttle the amount of capital coming in with the waterfall of demand on the horizon. It's so interesting, as I never assumed a possible Achilles heel to be too much too fast. I would love to see true north break down the possible scenarios for too much too fast. Could MSTR pay Buffet 11.5% on $380 billion? I think yes, but it's fascinating!

English

Had a spine tingling conversation today about Private Credit.

Estimates of 35% of insurance company balance sheets are comprised of Private Credit in North America

This private credit on insurance balance sheets is effectively financing large swaths of LONG TAIL Insurance and Reinsurance risk. (Think life insurance, liability & medical claims)

This means that the SOLVENCY of traditional long-tail insurance and reinsurance is becoming INCREASINGLY correlated to the Private Credit market.

If Private Credit permanently falters, solvency of the insurance market may falter.

It felt like the "Why are they confessing" scene in the Big Short.

If there's turbulence, Digital Credit will be ready to scoop & score.

Definitely still early to Bitcoin, btw.

English

⚡Brand New Episode Tonight📷 10pm EST / 7pm PST

True North Episode 58 - Is The Tide Turning?

Agenda:

- MSTR Billion Dollar Purchase

- How Big Can This Get?

- Is This The Bottom?

True North@MSTRTrueNorth

⚡Brand New Episode Tonight📷 10pm EST / 7pm PST True North Episode 57 - Signals From True North Live Agenda: True North Event Summary Saylor’s Keynote Traditional Pref’s vs. Digital Credit

English

⚡Brand New Episode Tonight📷 10pm EST / 7pm PST

True North Episode 57 - Signals From True North Live

Agenda:

True North Event Summary

Saylor’s Keynote

Traditional Pref’s vs. Digital Credit

True North@MSTRTrueNorth

⚡Brand New Episode Tonight📷 10pm EST / 7pm PST True North Episode 56 - The Quiet Accumulation Agenda: 1. Strategy Purchase This Week & Relativity 2. Strategy World Announcement Speculation 3. What’s the Next Driver for Bitcoin 4. AI Productivity Explosion

English

Currently deep in the red like I am? Imagine telling your grandkids that you started buying Strategy when it was called Microstrategy well before they offered digital credit, and you worked hard with 2 jobs & a side hustle to buy as much as possible every month thereafter.

English

@0xleegenz The key is to work a job that gives back to the community, that makes you feel like it’s worth your time. A very short commute ( preferably on foot) is also very healthy. The amount of money earned is less important. Just make more than you spend, & invest the difference.

English

@StrategyMaxi @Strategy I’m in the same boat. Actually I’m 10% deeper in the red. I buy more monthly.

English

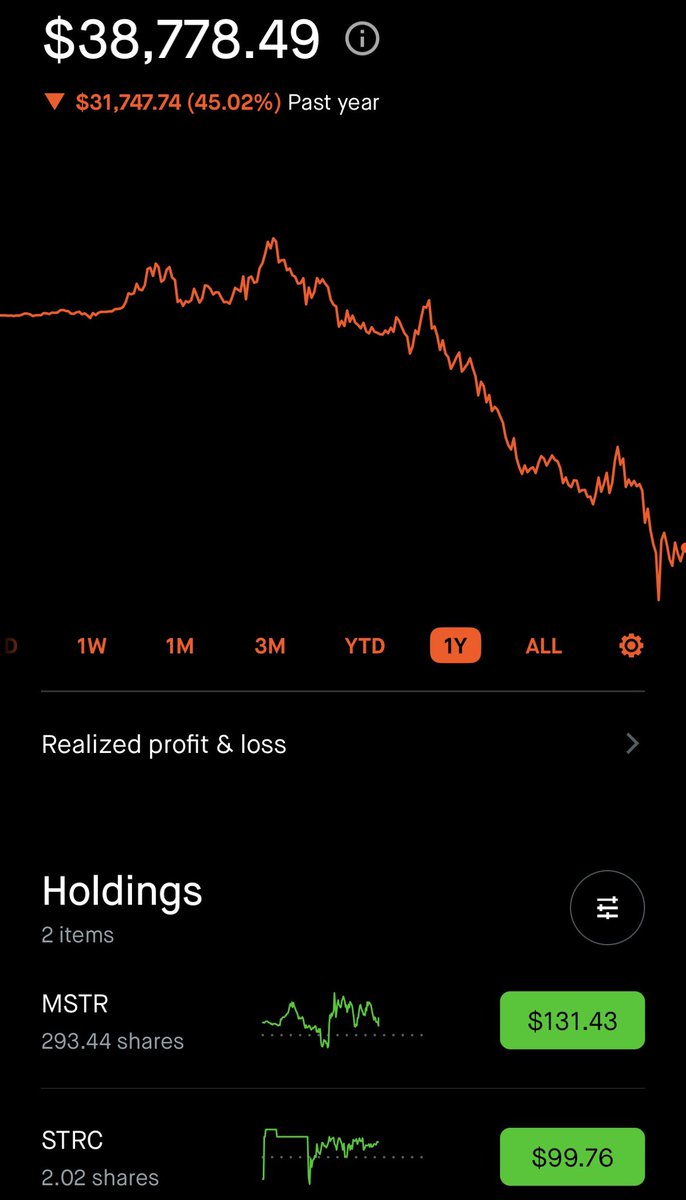

I have Skin in the Game!

Don’t listen to people with ZERO skin in the game bullshitting on X.

When I say I’m 100% $MSTR, I MEAN IT. I accept ALL the upside and ALL the downside.

Take a look at my portfolio 👇

Follow people who actually have skin in the game… like me! 💪

English

Marks retweetledi

🚨 BREAKING: CBS reportedly refused to air Stephen Colbert’s interview with Democratic Senate candidate James Talarico after pressure tied to Trump’s FCC.

Let that sink in.

A network news giant backing down because a president doesn’t like the politics.

Trump isn’t afraid of “fake news.” He’s afraid of losing Texas.

Here is the full 14 minutes for you to see what they tried to censor.

English

@halstonvalencia Do you see them in competition with each other, or complimentary?

English

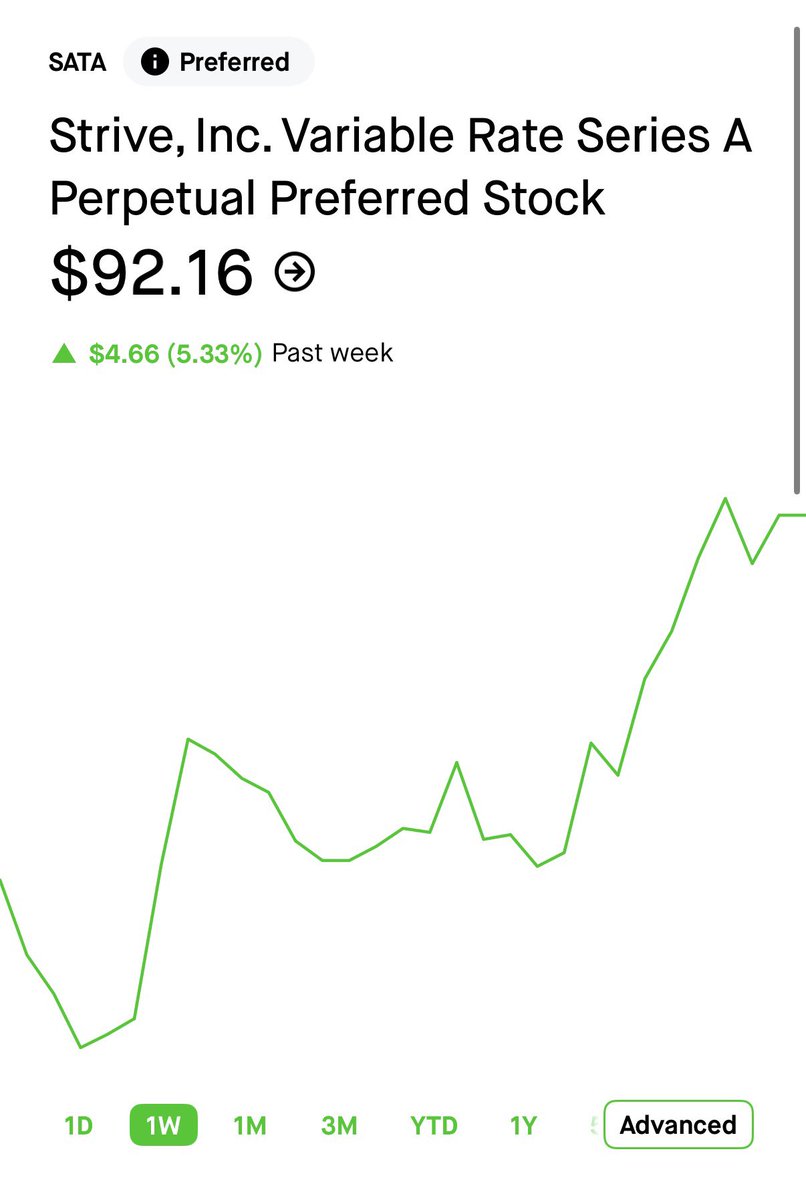

$SATA and $STRC are two of the most interesting products in not just bitcoin, but in finance in general.

SATA is particularly underrated right now:

- 12.5% variable dividend paid monthly

- Dividends treated as return of capital for tax purposes

- Designed to trade around $95–$105 par, currently below that range

- $127.2M cash on hand which means 17+ years of dividend coverage at CURRENT btc prices

The biggest risk in BTC treasury financing has always been debt maturity walls, but @strive and @Strategy are building capital structures that eliminate that entirely.

This is the future.

English

How to 10x-25x Your Wealth in Under 3 Years with ASST:

The more I look into the setup for ASST's growth, the more bullish I get. I love the entry here.

Beginning caveat: if you don't believe in Bitcoin, you aren't going to like amplified Bitcoin. Shocker, I know. Stop reading here instead of commenting "YEAH, but this ASSUMES Bitcoin goes up over time."

Just like any projections/model, there are assumptions made. If you don't like them, that's fine. My goal here is to illustrate what I believe to be a massive opportunity with what I perceive to be realistic and non-heroic assumptions.

If you don't like the assumptions, don't buy the stock. Most people don't have conviction in Bitcoin like I do, especially in the depths of the bear market that we've been in since the November 2024 election. (this is extremely obvious when pricing BTC in gold)

This is not financial advice. This is financial entertainment.

Now onto my reasoning:

ASST behaves like a Bitcoin exposure machine where the stock's potential upside (and downside) comes from four stacked engines:

1. Bitcoin's price move

2. Bitcoin per share increasing over time (often called "BTC Yield")

3. Issuing perpetual preferred equity and buying Bitcoin with proceeds (so Bitcoin amplification accrues to common stock ASST shareholders)

4. The market assigning a premium (or lack thereof) to the Bitcoin held (mNAV)

When these four forces compound together, the result can look like a rocket equation. If one of them fails, the outcome can flatten or reverse quickly.

I like making my aggressive entries when Bitcoin is in oversold territory, and looking at the relative strength index, the power law, the fear and greed index, and what it is priced at in other assets, it seems like we are there.

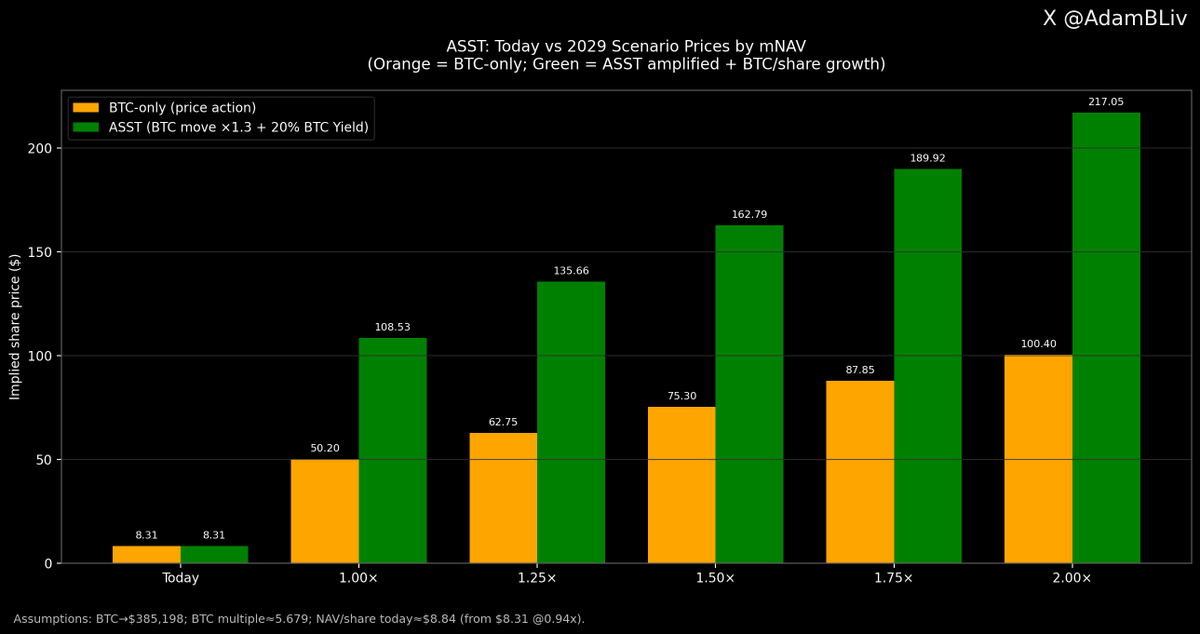

Right now we have a crucial anchor: an mNAV of 0.94x.

The current stock price at that multiple is $8.31, which implies the current NAV per share is $8.84.

That is what we are starting with, everything is just applying growth factors and then applying a future mNAV multiple (variable depending on market sentiment).

One target scenario is reversion to the regression fit line of the Bitcoin Power Law. Why people use it? Because Bitcoin has been volatile short term but strongly directional long term and the power-law regression tries to describe the "center line" of that long-term trend.

The "regression fit" means if you fit the curve to historical data, what does the curve imply at a future date?

This is a scenario anchor, not a promise. Obviously. Like I said, if you don't think Bitcoin is going up over long time periods, you don't belong in this trade.

If you look at the image below, you'll see the regression fit line three years from now is $385,198 Bitcoin. Could be higher. Could be lower. We are using that as a baseline that implies a price that isn't in a regime of ultra-bull market or ultra-bear market.

To calculate our BTC multiple move for ASST stock price: BTC multiple (M) = 385,198 ÷ 67,834 ≈ 5.679×.

ASST is currently amplified Bitcoin by close to 50%.

This model assumes they maintain 30% amplification on the way up to $385k which would imply they would need to issue another $2 billion of new SATA, which is less than 1/4th of Strategy's current pref notional value.

But that isn't realistic because they will be growing BTC yield. A modest growth of 20% BTC Yield per year (could definitely be higher due to small BTC stack size on a relative basis) would mean they need $3.86 billion of new SATA to maintain that amplification rate.

Still less than half of Strategy's outstanding, and they'd have 3 full years to do it. I think it's doable and we are in the infancy of the digital credit marketplace.

More BTC Yield means more pref issuance to keep an amplification target... it'll be interesting to see how the management team balances this based on demand for SATA.

Let's crunch the math for some stock price projections.

Remember the BTC move multiple of 5.679x.

Amplified BTC factor w/ 30% amplification is 7.08x.

A BTC Yield assumption of 20% per year for ~3 years is 1.73x, so each share today represents about 73% more Bitcoin in three years.

Current NAV/share ≈ 8.8404

Amplified BTC factor ≈ 7.082

BTC/share factor ≈ 1.733

Multiply the two factors:

7.082 × 1.733 ≈ 12.276×

So:

Future NAV/share ≈ 8.8404 × 12.276 ≈ $108.53

That $108.53 is the model’s “intrinsic Bitcoin NAV per share” in that scenario, before the market’s valuation multiple.

Now apply mNAV scenarios, because that is where the 10–20x gets spicy

So if future NAV/share is $108.53:

1.00× mNAV: $108.53

1.25× mNAV: $135.66

1.50× mNAV: $162.79

1.75× mNAV: $189.92

2.00× mNAV: $217.05

Now compare to today’s $8.31:

$108.53 ÷ 8.31 ≈ 13.1×

$135.66 ÷ 8.31 ≈ 16.3×

$162.79 ÷ 8.31 ≈ 19.6×

$189.92 ÷ 8.31 ≈ 22.9×

$217.05 ÷ 8.31 ≈ 26.1×

So yes, under these assumptions, a 10–20x is not coming from magic, it is coming from multipliers stacking:

BTC goes ~5.7×

“Amplified” response makes it act like ~7.1×

BTC/share grows another ~1.73×

market optionally adds a premium multiple (mNAV)

That is a rocket equation. It also cuts the other direction if BTC dumps (which is what ASST holders have been feeling lately).

These conditions must hold:

Bitcoin reaches something like the $385k neighborhood (or at least multiples up strongly). (obviously still make crazy money from here even if it only goes to $200k)

ASST maintains something like 20% BTC yield on a per-share basis, net of dilution.

The market gives ASST at least a 1.0× to 1.5× mNAV valuation at that time, rather than crushing it to a discount.

Capital markets remain open enough for preferred issuance to be rolled, scaled, and supported.

To me, these are all reasonable assumptions and I am allocating accordingly.

English