fallingknife

2K posts

fallingknife

@gofallingknife

irresponsible investor.

Katılım Mayıs 2025

630 Takip Edilen6.6K Takipçiler

@gofallingknife @aleabitoreddit Just bought some. I assume you're long?

English

Everyone is looking at $SMCI smuggling billions of dollars of AI chips to China.

But nobody is answering the question:

How do I make money off this, and is it a good buying opportunity?

My answer:

If $SMCI drops much lower than ~$24 overnight. It like a buying opportunity at a ~$14B MC.

Everyone looks at the DOJ case and thinks Super Micro are cooked.

But two things:

1. The company itself looks insulated, so far (not named a defendant)

2. $SMCI chip sales to China state actors was already known (just not to the $2.5B+ extent), by Hindenburg short seller reports in 2024.

So a decent part of the China revenue stuff was already priced in, which is why $SMCI crashed from $100+ and is now trading at $24.

Now if we strip away optics and some material revenue:

-> $SMCI GAAP net income was $1.05B last year, and FY 2026 is estimated to be around ~$1.25B with some estimates going to $1.5B.

And then we rip away an est ~$150M in smuggled in profit out of financials: ~$1.05 billion -> ~$900M?

On a P/E basis, still looks relatively cheap as a growing company, maybe ~10-11x?

Now the downside:

-> Optics are still trash. You can add more trash to trash.

But it's still trash regardless, doesn't change much?

-> $NVDA distancing itself with $SMCI? (They already did in 2024).

-> $SMCI not named a defendant, but in the case SEC/DOJ goes after them, then lot of regulatory fees and possibly fines.

-> Maybe order cancellations, but if they didn't cancel orders for the problems they had in 2024, it looks fine now?

Now... Are there a lot better opportunities than taking this regulatory leap of faith?

100%.

Is there potential more downside from panicking?

Yes.

But if you strip away the noise, $SMCI as a company looks cheap ~$14B at roughly 10-11x forward earnings.

English

@aleabitoreddit @gofallingknife Are you a buyer as it dropped way below $24? If so, heavy buy?

English

$TE finally announced an earnings date scheduled for 3/31 @ 6:00am EST release.

English

BREAKING 🚨: X users have burned through 15 trillion AI tokens arguing $IREN vs $NBIS - accidentally creating more demand for both companies than any analysis ever could.

English

English

English

@aleabitoreddit @thgstar2 Felix wang tech analyst at Hedgeye has just stated on X that #RPI is one of his 3 new stock picks. Explains the strength

English

$AAOI one thing that is given me pause on AAOI up here is the stocks recent parabolic move ... and I imagine management and their bankers will almost certainly be evaluating opportunistic financing ... I would not be surprised if they take advantage of the recent stock strength and come to market with an ATM, secondary and/or convert ... I mean, this is what growth companies do, no? If/when hyperscaler demand materializes, they must invest ahead of revenue. Their balance sheet is stable, but I wouldn't characterize it as strong. Selfishly, I'd love the opportunity to buy on a capital related pullback.

English

PJM approval status for Scrubgrass will move this ticker. That results in an extra 750MW secured.

Not a bad idea to position ahead of that approval. Especially since job openings for roles the roles Power Plant Fuels Technician and Assistant Plant Controller were posted specifically for Scrubgrass in January 2026.

To me this indicates $BITF has active execution on site development and see the endzone on PJM approval.

English

$IREN's AI Cloud customer @FireworksAI_HQ announces acquisition of Hathora

CEO @lqiao said "Fireworks AI acquired Hathora not for gaming customers but for its ultra-low-latency orchestration stack".

The goal: build a global compute layer for real-time AI inference where millions of continuously customized models run and agents interact faster than humans.

Global computer layer? That rhymes with global leadership in AI cloud

Choosing the right partners is paramount in dominating the AI Cloud on a global scale.

SiliconANGLE@SiliconANGLE

Fireworks AI bets on Hathora acquisition to power the next phase of real-time AI ift.tt/0BjMI51

English

@aleabitoreddit Solid comparison. Did a spec position on it and I’m crying I only bought $200k last week. Had no idea the $nvo lawsuit was coming to an end, just pure luck. Doubling my position this week even after the 40% bump.

English

Feels like people aren't articulating the bull case for $HIMS correctly:

Here's my view.

The main moat of $HIMS is network capture of retail audiences.

And the bull case is latent revenue monetization.

$HOOD achieved that same effect in fintech over 2025.

$META (fully grown) achieved that same effect in the social media sector over the past decade.

$HIMS is now at the starting point in 2026.

But given millions of new users across the globe (Europe, Australia, Japan, Canada) from Zava + Eucalyptus:

$HIMS now has that one-of-a-kind retail audience capture in the healthcare sector.

However, the difference between ~$70B companies in Robinhood and $1.6T giants in $META is that:

They've already successfully monetized their retail audiences both through margin optimization, and new revenue streams.

And very aggressively. $HIMS has not yet.

Robinhood did so by pushing new products from banking/credit cards/prediction markets/etc.

And they are all now independently generating $100m+ each as new revenue streams.

$META did so by capturing the maximum amount of revenue per user after acquiring WhatsApp/Instagram.

However, $HIMS has not gotten the chance to yet in the same way they did with the US (eg. Testosterone). Especially partially due to former lawsuits.

Now that's cleared up, the bull case can be seen again:

Instead of modeling what revenue Zava/Eucalyptus traditionally brought, the important thing to look at is retail network capture through # of people.

As this is biggest source of latent revenue + revenue projection beats not priced in.

Now, the billion dollar question is:

Will $HIMS end up like $HOOD?

$HIMS now has the one of the largest retail networks + distribution for healthcare.

However, cross-selling seems much harder in healthcare vs. fintech or social media channels.

The answer whether it ends up a $30B company or a $5B one is up for management to figure out.

So for people on the sideline, it might be worth flipping long again in the off-chance $HIMS manages to figure out latent revenue expansion from their new global userbase.

The ~40%+ short interest and the new $NVO partnership serves as a huge bonus as well.

English

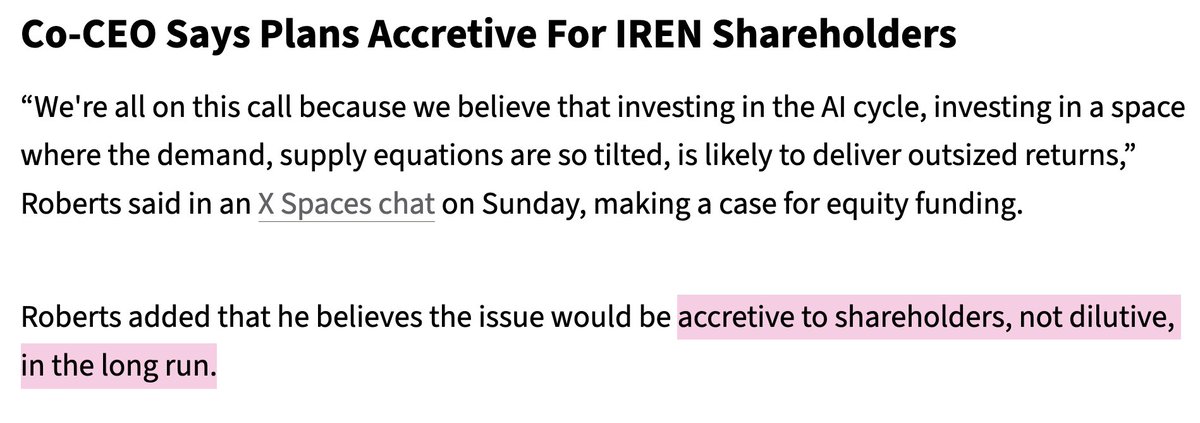

Dilutive to book but accretive to eps. Bad for 3 month holders great for 1 year+ holders.

Have you tried modeling it based off Microsoft deal terms? Those assumptions would be worst case because $/KWh/month is only increasing and not decreasing.

Bullish on Riot NBIS and WULF great picks and hedge strategy for 3-6 months. However, it is likely $iren will outperform all 3 by 2027.

English

It's probably the first time I've ever heard someone say $6B in ATM dilution was not in fact "dilutive".

But in fact, "accretive".

If you genuinely believe this and want to be buying liquidity for the $6 Billion in new $IREN shares sold over time into the open market, you're welcome to do so.

English

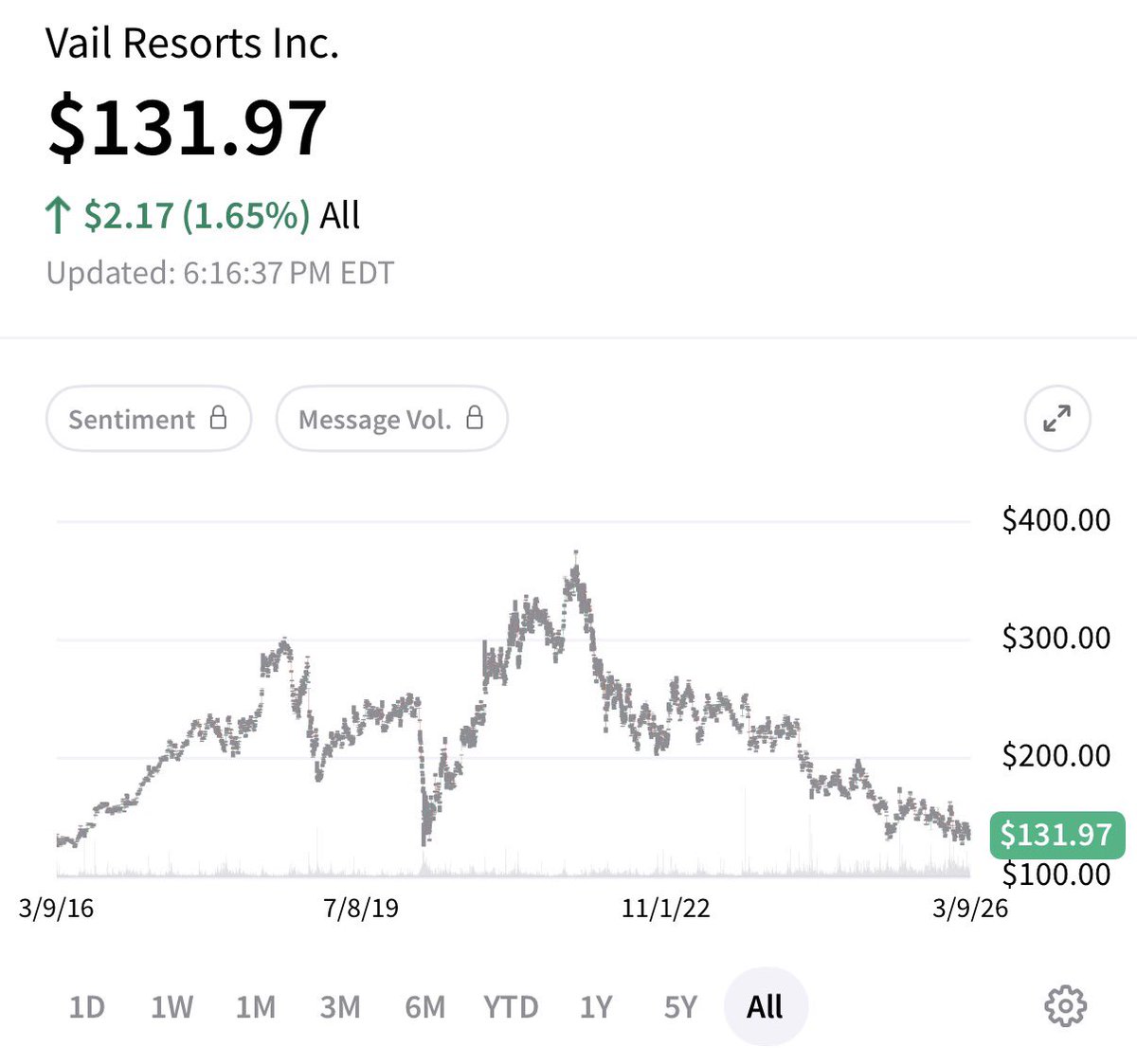

Clarification: worst snowfall in Colorado in 25 years. That geography represents 12% of their footprint but 45-50% of skier visits on peak seasons.

Doesn’t seem like you follow the news or market much but here’s a simple override to your small sample logic

2021 - Covid bubble everything popped

2022 - Systemic crash from rate hike

English

@gofallingknife @eastdakota 2022/23 and 2023/24 were amazing (and 2022/23 was RECORD) where was stock then compared to 2021/22 which was below average snow???

English

Vail Resorts ($MTN) likely to open tomorrow down to where if you invested 10 years ago you’d have done as well putting your money in a hole. It’s time for a change to become more asset-light, sell off resorts, and allow character and differentiation to return to skiing.

English

@midlevelcruiser check ur DM i sent market signals popping off that supports the trend.

English

there was a neon blinking sign throughout February that markets were about to roll over. If you have cash, I wouldn’t be too fast to BTFD, we probably haven’t seen the worst yet. $SPY $SPX $QQQ $NDX

Mid-Level Cruiser@midlevelcruiser

I am very cautious of this pump. Raising cash. March / April puts on $SPX and $NDX.

English

@_Timdoyle @wearehims @AndrewDudum Congrats on the acquisition, impressive retention from the early cohorts

English

We're joining @wearehims to build the world's great preventative health business.

What I think separates @AndrewDudum and his team from the endless list of businesses pursuing this, is the understanding and ability to serve the average person.

English

Anyone yet read this piece $TTD Jeff Green put out, as to why he bought $150 mil of his stock?

thecurrent.com/opinion-jeff-g…

English

Everyone wants $IREN to sign deals today, because they have 4.5GW of contracted power today. And will energize 1.4GW of that power next month. But at the same time, everyone wants to benefit of the higher GPU hour prices that the market is seeing, but we also want to sign long dated contracts to justify the purchase of these GPUs, and cover the payback period.

> Be @IREN_Ltd

> Do everything early

> Buy plenty of land, sign interconnects, secure grid power

> Sign your first hyperscaler with GB300s at $2.92 per hour

> Lose 50% of your market cap

> Wen deal

> Buy 50k B300s without naming a client

> Wen deal

> H100 prices exceed your GB300 contract

> Wen deal

Retail investors are impatient and irrational.

IREN is not an on-demand company.

IREN (pre-)contracts all their GPUs.

H100 spot prices are not something you can enjoy when you lock your customers in for multiple years.

Deals are long-dated contracts for GPU hours.

A deal today means you lock in the price of today.

A deal in 2025 means your GPU rate is much lower than a deal in 2026.

Screaming "wen deal" doesn't line up with wanting to capture the highest value of your infrastructure capabilities.

Long duration contracts are great for DCF models, but they need to capture the value of the market.

There is no better way to do this than gradually

Signing everything today would lock in the prices that will be outdated in a few months.

There is no capacity flood hitting the market any day soon, and the newest models need the best GPU iterations to run smoothly.

Datacenter capacity is a larger constraint than the underlying power

IREN is not creating a massive backlog, it doesn't tout about being sold out for the rest of 2026, but quietly divides their upcoming shipments amongst their existing clients and signs them at the rate that will be applicable when they actually arrive.

If you think the increased ARR guidance from the 50K B300s was disappointming, remember that they guided for $2.5B of GPU financing for the $MSFT deal.

They ended up with $3.6B instead.

I'm sure they will report a higher actual result due to market economics improving.

Wen deal is cute, but it fails to capture the investment thesis. IREN as a company and as a stock, doesn't rely on the short term price action of a deal announcement.

IREN will rerate on solid earnings and strong EPS

-> No massive backlogs

-> Deals with revenue recognition within 3-4 months

This is how I envision 2026 to look like for IREN.

Everything will be contracted, but I hope we have learned from the $MSFT contract.

If IREN were to sign a hyperscaler, it will be for Sweetwater, but since this will be phased, massive scale operation, with possibly the newest VR300 architecture in mind. I think this will not be something to happen soon.

If you hold IREN you need to have a ton of patience. But this flywheel is just spinning up now.

I'll be here for that inevitable inflection point.

English