Half Lemonade

28 posts

@halflemonade The final outlook still hinges on the ongoing testing and qualification results of M10Q

English

The deployment of PTFE materials is currently confined strictly to exploratory testing and is highly unlikely to achieve commercial adoption in mass production. Investors should entirely disregard the market noise surrounding PTFE, as the clear, non-negotiable mainstream roadmap remains anchored exclusively by M9Q and M10Q materials.

Jeff Pu@sssjeffpu

Abstract of Our PCB Note -> PTFE Likely Chosen for Nvidia Kyber Midplane ✅ Key Highlights: •PTFE likely be selected over M9+Q glass for superior high-frequency performance & lower signal loss •PTFE supports 337G+ SerDes requirements •PTFE has solved past rigidity/drillability issues Market Impact: •PTFE CCL market projected to hit RMB 8bn in 2027 for Kyber •Further ramp expected in Feynman platform •Mass production likely starts late 2026 due to manufacturing complexity Stock Beneficiaries: •Shengyi Tech (600183 CH) •TPE 台虹 (8039 TT) •Upstream: Dongyue Group (0189 HK) — main PTFE supplier to Shengyi •Others: Daikin (6367 JP), Haohua Chemical (600378 CH) Solid long-term tailwind for PTFE supply chain. #NVDA #Kyber #Midplane #正交

English

PCB进展更新

1,Vera Rubin200机柜中OAM板的技术规格、价值量等情况?

在Vera Rubin200机柜(26年大概45000柜)的Computer Tray中,OAM板(Super Chip HBM Board)采用M8材料,为7+12+7结构的26层HDI板(GB300为6+12+6的24层板),对应下一代Ultra Rubin为52层板。

供应商份额方面,胜宏份额最大;其次沪电;再次鹏鼎;然后是深南、方正等。此外,预留了10%的份额,将根据供应商的交付速度进行分配,其中胜宏有较大机会获得这部分份额。

目前,OAM板的生产良率普遍在85%至90%之间。

2,Vera Rubin机柜中价值量最高的PCB是哪一块(BlueField-4)?Vera Rubin机柜中价值量最高的PCB是用于连接OAM的正交中板(Orthogonal Middle Plane)。其在单个机柜中的总价值量占据了机柜内PCB成本的绝大部分。供应商份额方面,沪电是主要供应商;其次深南;再次胜宏。

由于其高层数、M8材料特性以及0.2mm的孔径对钻针、电镀和镭射工艺提出了极高要求,该板的生产难度很大。

3,Vera Rubin机柜中Switch Board的供应商情况以及选用高端铜箔的原因?

Switch Board的供应商份额分布较为平均,包括深南、生益、胜宏、沪电、鹏鼎、方正等厂商均有参与,每家占比大约在10%至15%之间。

尽管Switch Board设计相对简单,但它仍需使用HVLP4等级的铜箔。这是因为它需要直接连接OAM板,为了确保信号传输的稳定性和避免低K值问题,必须采用高规格的铜箔。

4,Vera Rubin机柜中OAM板、正交中板和Switch Board的上游CCL及铜箔供应商情况?

这三款板材的上游供应商情况如下:

OAM板:CCL完全由台光供应(Only)。铜箔供应商仅有两家,分别是德福,铜冠和三井,均为HVLP4等级。

正交中板:CCL供应商主要为台光、斗山和松下。铜箔供应商包括德福、三井和松下,同样采用HVLP4等级。生益科技未进入该板材的CCL供应,因其板材目前主要供应至HVLP3等级,适用于800G光模块,但在1.6T及以上的高速应用中则较少出现。

Switch Board:CCL供应商包括生益、台光和斗山。

5,在Vera Rubin机柜的Computer Tray中,除了OAM板和Switch Board,还有哪些PCB组件价值较高?

在Computer Tray中,SSD和HBM4模组的PCB也具有较高的价值。6,关于LPU机柜,其目前的开发进度、预计推出时间以及面临的主要挑战是什么?

LPU机柜目前仍处于样品阶段,并非量产产品。该项目自2026年3月开始,由富士康主导,遵循NPI(新产品导入)流程。原计划于2026年第三季度推出,但目前看来存在难度。预计其推出时间将推迟至2026年第四季度。延迟的主要原因是PCB和封装厂的验证工作仍在进行中,这些验证环节要求严格,例如通电测试需要持续1000小时,相当于约一个半月的时间,这是导致时间表推后关键因素。

7,Ultra Rubin方案中OAM板和Switch board的在材料和工艺方面可能面临哪些潜在变化?

Ultra Rubin方案中的OAM板在材料和工艺上存在一个潜在的变更风险。台积电在进行CoWoS封装测试时发现,M9材料的硬度较大,与芯片封装结合时,由于内应力无法有效释放,会导致板材出现翘曲现象。为了解决这个问题,封装工艺可能会从CoWoS转向台积PCB设计和材料选择产生影响。所以OAM主板基本结构不变,但组装工艺有变动。

Switch Board方面,目前的供应商包括胜宏、鹏鼎、深南、方正、超毅、景旺和沪电,这些厂商均在扩充其mSAP工艺产能。

8,Ultra Rubin散热系统是否采用了正交背板方案?

是的,Rubin平台为改变散热系统,采用正交背板方案以取代铜缆。

9,在Ultra Rubin的供应链中,OAM主板和正交背板的主要供应商格局?

OAM主板采用mSAP工艺,沪电因其在基站射频板领域的深厚积累,耕耘最深,预计将占据主要份额。沪电和深南电路是值得关注的供应商,但需要注意两家公司的新建产能(沪电常州厂、深南珠海厂)目前仍处于建设或准备阶段,具体产能释放时间尚不确定。

10,GB300平台生命周期内的总出货量、出货节奏等?

GB300平台的生命周期总出货量预计为55000个柜。该产品从2026年年初开始放量。

CCL(覆铜板)供应商方面:OAM的CCL由斗山和台光电子供应。Switch Board的CCL由生益科技和斗山供应,台光电子未进入Switch Board供应链。

13,GB300 OAM板的主要供应商?

在GB300的OAM板市场中,胜宏占据主要份额,沪电、深南、鹏鼎供应商、欣兴方正和景旺也参与供应。

在Vera Rubin中,沪电的份额预计将从当前GB300 OAM板占比显著提升。这一变化主要得益于英伟达对其研发能力的看重,双方正在进行共同研发。

14,1.6T光模块PCB必须采用mSAP工艺的原因是什么?其与800G光模块PCB在工艺和材料上有何区别?1.6T光模块PCB必须采用mSAP工艺,因为其线宽线距已达到20微米,传统的HDI工艺无法满足要求。虽然曾有观点提出使用可剥离铜箔(载体铜箔)的方案,但因其成本比HVLP4铜箔高出近两倍,且需要使用镭射,总成本不低于mSAP,因此并不可行。

相比之下,800G光模块PCB可采用HDI或mSAP工艺,但由于HDI设备更为普及,通常采用HDI工艺。在材料方面,1.6T光模块PCB使用M8等级板材和HVLP4等级铜箔,而800G光模块则使用M6等级板材和HVLP3等级铜箔。

2025年9月时,800G光模块PCB的单价约为76至80元人民币,而目前已上涨至140元。1.6T光模块PCB的单价则从2025年约208元上涨至目前的420元。价格上涨的主要原因有二:首先,受地缘政治等因素影响,铜等原材料价格上涨,导致CCL厂商自2026年2月起陆续提价,涨幅达30%至40%;其次,市场需求旺盛,GB200和谷歌V7等新平台均采用1.6T光模块,导致板材和特定等级的铜箔(如德福生产的HVLP4)出现短缺。预计未来三个月内价格不会下跌。

15,目前市场上1.6T光模块PCB的主要认证供应商有哪些?

谷歌并未对1.6T光模块PCB进行独立认证,而是参照英伟达的认证结果。目前,通过英伟达认证并能批量供应1.6T光模块PCB的厂商主要有胜宏、沪电、深南和鹏鼎。虽然市场上有多家公司声称正在进入1.6T领域,但它们目前仍处于认证阶段,尚未通过。

在光模块组装领域,旭创与新易盛的业务重心有所不同。旭创主要产能用于生产1.6T光模块,而新易盛则相反,其主要产能仍集中在800G。

目前,英伟达已要求供应商送样3.2T光模块PCB,这表明其未来可能倾向于采用3.2T技术路线。而CPO技术主要是由英伟达推动,同样谷歌未来也可能会选择CPO路线。

16,对于1.6T光模块所使用的PCB,其市场需求、单片价值、月度交付量、利润率水平以及主要供应商格局是怎样的?

1.6T光模块PCB采用mSAP工艺路线,性能要求比HVLP4更高。目前鹏鼎每月交付量约占市场份额的20%至25%,并且这个量级预计还会增长。该产品的利润率显著高于800G产品的利润率。800G产品的单价仅为1.6T产品的40%左右。

在1.6T光模块PCB供应方面,目前鹏鼎只向旭创交付。新易盛的1.6T光模块PCB主要由沪电和胜宏科技供应。

17,1.6T光模块PCB的价格从200多元上涨至420元,其涨价的具体时间点是什么时候,未来价格走势如何?

价格上涨主要发生在2026年春节之后,是由CCL厂商率先涨价30%所带动的。目前来看,价格不会继续上涨。主要原因有两点:首先,CCL厂商的交期已从8周延长至12周,但已下订单的基板价格不会再变动,锁定了未来12周内的成本。其次,当前价格已处于暴利水平,再涨价将超出终端客户如NVIDIA及北美零售市场的承受能力。

18,鹏鼎未来的产能扩张计划将如何影响光模块业务?

旭创的1.6T PCB供应商主要有四家:沪电、深南、景旺电子和鹏鼎,各家交付量和产能大致相当。公司计划在2026年7月将总产能提升至40万平方米/月,并在11月达到50万平方米/月。然而,新增的产能将优先分配给AI Pin和自动驾驶相关业务,因此光模块业务能获得的产能增量有限。

产能扩张确实受设备交付的制约。目前所有mSAP相关设备都面临供应紧张,采购周期已排到明年(2027年)。具体来看,瓶颈设备包括镭射钻孔机、电镀镍设备、直立式曝光机以及压合机等。

中文

A 28% yoy rental price decline actually implies a pretty fat IRR >~30%. And spot prices at AWS/GCP imply a big premium to what this series shows (~50% higher).

Most importantly, the A100, a 5yr old GPU, is still in high demand at prices implying less than 28% rent declines.

James Chanos@RealJimChanos

The BBG Hopper GPU Rental Index with a big move down in late-October. Now down 28% Y/Y.

English

"But this sounds like OpenAI is entering the EDA territory — the realm of Cadence and Synopsys."

No, they are not dawg

Jukan@jukan05

But that’s fascinating. How could OpenAI possibly develop AI technology related to semiconductors? Of course, since OpenAI is taking the lead in designing the ASIC with Broadcom, it’s undeniable that they already have some semiconductor design capabilities. But this sounds like OpenAI is entering the EDA territory — the realm of Cadence and Synopsys. How are they even able to do that?

English

Google is indeed increasing the portion of TPU designs it develops in-house. However, they still can’t make everything on their own.

$AVGO looks very promising—except for the uncertainty surrounding its project with ByteDance.

The AI Investor@The_AI_Investor

AVGO holders, why do you think Google can’t drop Broadcom and develop TPUs with Marvell or fully in-house instead?

English

买入msft/mrvl call做反弹。

msft很明显410就是底,goog再等等180以下。mrvl等110以下再加。

中文

google的卡,这里说的是个数不是价格,76%是asic,24%是nvda gpu。

这个比例24年和25年差不多,所以你可以线性的推理。

asic目前是avgo,下一代7代是mtk和avgo。

中文

Had lunch with the Comfort Systems $FIX CEO this week. No signs of slowing. Numbers going higher for $FIX $VRT $TT etc.

English

@elonmusk @markusdd5 @JeffTutorials Who makes the cooling equipment? Seems tough with the hotter chips

English

@markusdd5 @JeffTutorials Not as high as that, but still very high. The march of 9’s of reliability requires massive data and compute.

English

We are nothing without our fans

Smoke-away@SmokeAwayyy

Elon is building a giant GPU cooler in Texas.

English

Selling Euro 2024 tickets:

Match 46, Hamburg, QF, 2 tickets

Probably:

Portugal v Serbia/Denmark

Match 47, Berlin, QF, 4 tickets

Probably:

Belgium v France

Happy with PayPal, video call, sharing ID etc.

Genuine seller, have sold other tickets

#euro2024 #tickets #eurotickets

English

@LA_stevens_ What do you think is happening with CPNG? Earnings was great but stock has been pretty poor since

English

@willschoebs I honestly couldnt find anything actually wrong in MF's earnings. Numbers were good imo

English

🇯🇵 growth tech / software (a.k.a. the names "hot money" foreigners generally touch) is getting absolutely SMOKED today...and, frankly, beyond just today...

Names like Rakus & SHIFT at 52W lows...Hennge straight down since earnings, Sansan & Money Forward crushed on earnings

English

enabling Shopify's Markets Pro product for international selling decimated our conversion rate internationally. This is NOT a product for anyone wanting to scale internationally.

English

@RadnorCapital What do you make of NVDA saying the new B100 chip can reduces cost and energy consumption by up to 25x for large language inference models? Isnt that bad for VRT?

English

Index of ~30 🇯🇵 SaaS companies is down 2.4% YTD, while the Nikkei 225 is up 16.3%...

"When there's blood in the streets..."

I joke 😂...but in all seriousness, will be interesting to see when exactly & how fast this software basket flips the Nikkei...may not be in '24

English

@RadnorCapital Have you looked at the construction companies building data centers? FIX's stock chart is pretty incredible

English

More hyper scale capex commentary courtesy of Wedbush:

AWS $AMZN - As we look forward to 2024, we anticipate CapEx to increase year-over-year primarily driven by increased infrastructure CapEx to support growth of our AWS business, including additional investments in generative AI and large language models.

$MSFT - We expect capital expenditures to increase materially on a sequential basis, driven by investments in our cloud and AI infrastructure and the slip of a delivery date from Q2 to Q3 from a third-party provider noted earlier.

$GOOGL - The step-up in CapEx in Q4 reflects our outlook for the extraordinary applications of AI to deliver for users, advertisers, developers, cloud enterprise customers and governments globally and the long-term growth opportunities that offers ... In 2024, we expect investment in CapEx will be notably larger than in 2023.

$META - We are also investing more in our AI infrastructure capacity this year. And given many of our ambitious forward-looking plans will rely on having sufficient compute capacity, we expect this to be an area we invest more aggressively in over the coming years. We anticipate our full year 2024 capital expenditures will be in the range of $30 billion to $37 billion, a $2 billion increase of the high end of our prior range. We expect growth will be driven by investments in servers, including both AI and non-AI hardware, and data centers as we ramp up construction on sites with our previously announced new data center architecture.

Radnor Capital@RadnorCapital

I own Vertiv $VRT (leader in power / cooling solutions for several end markets, but most importantly, data centers) and will continue to own. I’d imagine the stock continues to run into earnings on 2/21 after strong data center capex commentary from the hyper scalers and robust trends from other AI / data center beneficiaries like Super Micro $SMCI (there is a very linear correlation between cloud capex and Vertiv demand). Vertiv came public in February 2020 via SPAC. The sponsor was Dave Cote, the legendary CEO that turned around Honeywell $HON. This is like Satya Nadella forming a SPAC and buying an enterprise software company. These guys have domain expertise and domain dominance. This is a good (not great) company benefiting from a massively rising tide. Its also the biggest pure play available to ride that tide. My thesis is based on a few key points: market for data center power / precision cooling is exploding, gaining market share, and upside to numbers (at a reasonable valuation). I say good (not great) because while their solutions are certainly not commoditized, they are replicable (more similar to Super Micro than Nvidia $NVDA in terms of proprietary technology / margin profile) and they also had some execution hiccups around the pandemic (although under a different management team). I will further discuss these points below: The first point to mention is the durability of data center / AI capex, because everything else is downstream. Everyone from Microsoft $MSFT and Google $GOOGL to Super Micro and TSMC $TSM and Eaton $ETN / Trane $TT continues to be extremely optimistic about this trend continuing. Importantly, Microsoft spoke on their earnings call about inference use cases taking shape, showing the economic benefits of these outsized AI investments. This should put to bed the belief that there could be an “air pocket” in demand on the horizon. The transition from traditional CPU-focused servers to GPU-powered AI servers will take a long time and drive growth for the foreseeable future. My belief in this multi year wave is also underscored by record order pipelines and backlog – I expect orders to grow in excess of backlog again in 2024. Comments from management suggest current demand could take 3-4 years to work through. The data centers running those AI servers generate 5x more heat / power than traditional CPU servers and require 10x more cooling per square foot. ~75% of Vertiv’s business is power and cooling related infrastructure, with the balance largely being services like maintenance, installation, remote monitoring, etc. Vertiv has announced plans to double its production capacity for electrical switchgear and busway over the 2023-2025 period. This comes on top of a >100% increase in capacity over 2021-2023. And they recently opened a new manufacturing facility in India for thermal management products for domestic and international markets. This follows the opening of a thermal manufacturing facility in Mexico early in 2023. And at its recent investor day, management raised medium-term capex guidance to 2.0-2.5% of revenue, from an average of 1.6% over 2019-2022 period. This capacity expansion is obviously rooted in the belief that demand is durable and sustainable (similar to Super Micro’s comments of taking capacity to ~$30bn from low teens today). A general rule of thumb is that if volume of data goes up 10%, we generally will see 3-5% increase in the volume of gear to ensure adequate power supply. Many of these AI benefits are yet to flow through to Vertiv, particularly around liquid cooling. There are several reasons for this: The market for cooling infrastructure is gradually transitioning from air cooling (where Vertiv is currently the leader) to liquid cooling (which is Vertiv’s to lose). Super Micro’s CEO said on the last earnings call: “You are right. In these current 600 watt / 700 watt modules, people can still do well with air conditioning. And that's why people still are comfortable with our traditional air cooler. But when that system grows to 1,000 or even 1,000 watt per module, yes. I mean -- I think cooling becomes even much more critical.” Basically as power / compute demands increase, there is a need for more heavy duty cooling direct to the chip / rack. Super Micro CEO then said: “I anticipate that up to 20% or more of global data centers will transition to liquid-cooled solutions in just a few years.” So we are early days. Important to note that liquid cooling will largely be additive to Vertiv’s business – down the road ~1/3 of thermal cooling will still be from air cooling – liquid cooling does a great job taking heat away from the chip and rack but it still needs to be moved and expelled from the building. For example, traditional compute requires 6 computer room air conditioners vs. 10 for high density compute. As we move toward Nvidia’s next chip (B100), more cooling capability will be required. The industry was growing high single digits prior to liquid cooling – so growth with liquid cooling is obviously higher. Additionally, new AI data centers take time to permit, build, etc. and even existing data centers are only turned on with half – 2/3 capacity, which illustrates why the demand curve could be longer and more durable than the market appreciates. A few comments from management on the last earnings call: “still very early in AI opportunity – its barely started.” “AI will show up in more pronounced manner in 2024.” “More demand than capacity in industry.” Longevity of current order inflection: “Believe this is a long term trend – multi year cycle – this is just the beginning” As I mentioned, Vertiv is the largest pure play, with other competitors like Schneider $SCHN, Eaton and Stulz $STULZZ, as well as a long tail of independents (still ~50% of market). As hyper scalers continue to drive AI data center demand, there are only a few players that can service this demand. Scale and service excellence matter when dealing with hyper scalers (they want someone to hold their hand). Ecolab $ECL has a similar competitive advantage. Vertiv’s product offering is good, not great, but their ability to service customers and be a one stop shop / systems integrator for power, precision cooling and other infrastructure management systems is what sets them apart. For example, you don’t want several different teams in your data center, you want one team doing power, air cooling, liquid cooling, etc. This is why Vertiv has the prime position and this is why it is theirs to lose. There are also several startups working on liquid cooling technologies – these starts up could never service the needs of a hyper scale data center – so the natural move is for Vertiv to buy them. At ~2x net leverage and a cash generative business model, they are positioned to make this happen. We also cant overlook the fact that Vertiv has partnerships with Nvidia, Intel $INTC (bought Habana AI in 2019) and others. Jensen (Nvidia CEO) called out Vertiv as the world leader, saying their collaboration is growing in leaps and bounds and that their partnership is more important than ever. Numbers / estimates higher at a reasonable valuation = stock higher. Simple model summary and valuation snapshot below. These are base case estimates and I don’t expect them to guide to what I am expecting right away on the Q4 call. I also reserve the right to revise my estimates as the data suggests - likely higher. Starting with Q4 – management said to expect a similar growth rate in Q4 as in Q3. We saw 18% growth in Q3 and the street is at ~14% growth for Q4. Either people aren’t paying attention, or they don’t trust management. I trust that this management team will continue to be conservative with the hopes of creating a consistent beat / raise story. At the investor day in November 2023, management gave “very preliminary” 2024 guidance of 8-11% sales growth and operating margins 16.5-16.9%, with 83-87% FCF conversion. Given the “very preliminary” comment its clear that this is more a floor than a ceiling. The street is at ~10% growth for 2024 and has it slowing to HSD in 2025 and 2026. Important to note that Vertiv’s growth has largely been US driven (grew >40% in 2023). And while this is where most of the AI investment is taking place, international markets will eventually pick up – this is another advantage of Vertiv’s global footprint. Vertiv grew >20% in 2023, despite APAC down ~5% (macro weakness in China) and EMEA only up high single digits. Additionally, management has said incremental margins (margins on incremental revenue that flows through) are currently ~30%, but will move toward ~35% as the liquid cooling investments start to bear fruit. As you can see in my model summary, I can get to >20% operating margins in 2026 (managements long term guidance is 20%+ operating margins sometime in 2026-2028 period). Backlog is also at record levels ~$5bn, which tells you >3/4 of the year is already accounted for. And again, I expect orders to grow faster than sales through 2024, leading to another record backlog number on the horizon. Importantly, management spoke to taking ~5% pricing in their backlog, which tells me pricing could be up mid single digits again this year. Historically this has been a flat to down ~1% annually pricing business, but the demand environment has changed this and I expect it to last for several years before mean reverting. Management has said they expect to be price / cost positive on a go forward basis. Balance sheet is healthy, which will allow them to paydown debt, buyback stock and make bolt on technology acquisitions. Current debt structure is $850mm fixed rate bond 4.125% due October 2028 and a $2.1bn term loan due March 2027. The term loan is split between $1.1bn at variable rate currently ~8% (focus is to pay this down over next two years, which should allow them to accelerate capital deployment) and $1bn fixed ~4%. Vertiv also has authorization to buyback $3bn worth of stock over the next 4 years (~15% of market cap). The stock currently trades ~20x EV / operating profit (I’m using this metric because this is what they guide to). I’m assuming this multiple holds, which it will as long as numbers / estimates go higher. There is no pure play comp, but Eaton trades ~23x and Amphenol trades ~22x (also a low double-digit growth with >30% incremental margins). As I look out a few years, I can still get to meaningful upside, despite the recent run in the stock (see below). The key risk is that AI investment / capex slows. Additionally, Vertiv could lose market share if they don’t continue to innovate / buy the innovators. They could also make execution errors, which they did early in Covid under a different management team. Vertiv also serves certain telecom end markets, which have slowed post heavy 5G investments. However, this is a small part of the overall business (and getting smaller given data center growth).

English

@Patticus Is this a data set you guys regularly released? Would love to subscribe if so, very helpful info.

English

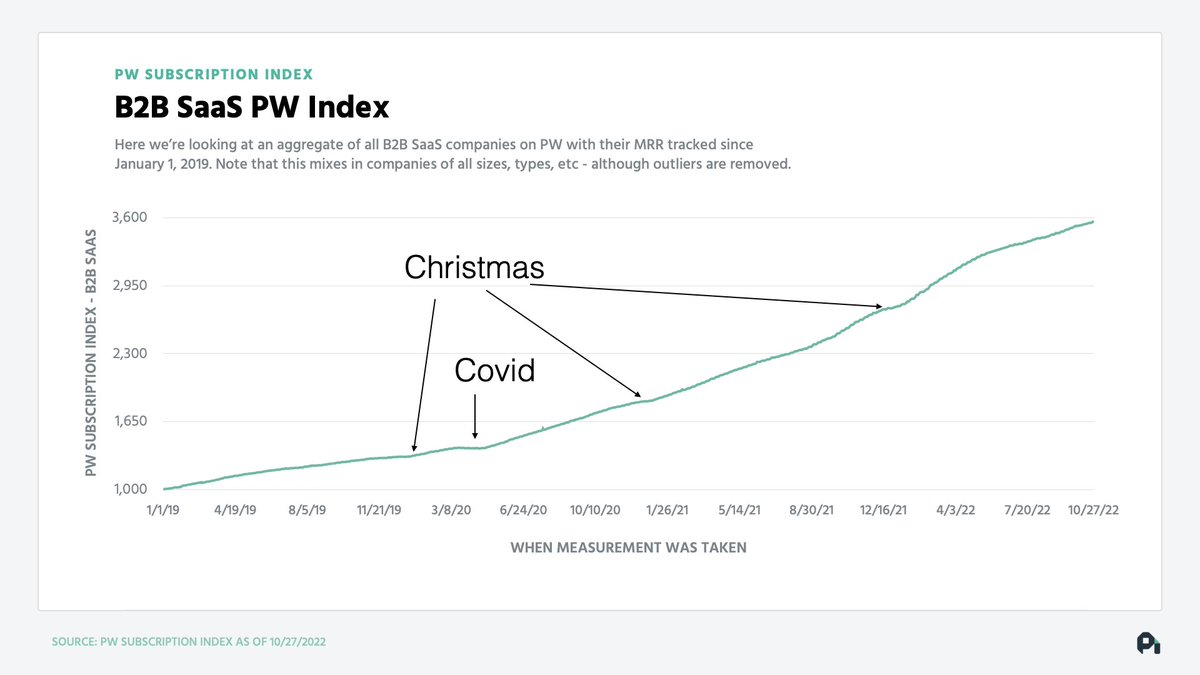

Let's first look at businesses who sell to other businesses (B2B).

Here's revenue growth since 2020.

Notice how COVID was no worse than a Christmas slowdown. Just a little blip.

Mazel Tov everyone. 🎅🕎

But wait - what's happening at the end of that graph? 😳

English

Half Lemonade retweetledi

What is stock-based compensation?

Here’s an overview of this controversial & confusing topic explained (in plain English):

English