Government L⃫u⃫n⃫c⃫h⃫e⃫s⃫ Groceries

7.8K posts

Government L⃫u⃫n⃫c⃫h⃫e⃫s⃫ Groceries

@iamdamone

Carnivore

Katılım Eylül 2010

218 Takip Edilen151 Takipçiler

Is this as "sale" as it gets?

$apm.to $apm $anpmf

Boz@bozkaschi

Andean Precious Metals $APM.TO Holding a Big Position 🔥✌️ Fourth Quarter and Year-End 2025 Highlights: Record Revenue of $133.7 million and $359.8 million for Q4 and year-ended 2025 💸

English

@SteveSaretsky Intervention -> Price Controls -> Scarcity -> Rationing -> Starvation.

English

@FibSixOne8 Flight costs double yet? I see Canada domestic air travel 2x come August

English

I need to buy a few thousand worth yen cash soon. I think I'll hold off.

English

@ronmortgageguy Ron. What is the term for a borrower who can neither pay back a loan, or does not intend to pay back a loan, yet still borrows the money?

English

Can Ontario (which owes more money than many small countries) & Canada just keep spending because somebody buys our Bonds?

So far YES

Which means we are all part of one of the biggest FAFO experiments in history

English

Nobody In Canada Really Cares About Government Deficits: Until We All Have To Care

Ontario ran out another huge $14B Deficit yesterday

The massive $88B Federal Government Deficit will be higher once we get the actual numbers

The BC Deficit is a Ball Buster

No one cares

2/

English

@ksorbs He looks good for 95. Role model material.

English

From Captain Dylan Hunt to Captain James T Kirk, Happy Birthday, sir.

William Shatner@WilliamShatner

At 95, I'm still smokin'! 😝 I’ve learned two things: Never waste a good cigar. Never trust anyone who says you should ‘act your age.’ 😉👍🏻

English

@JeffMcCrimmon80 @BenRabidoux @cbcwatcher Don’t ask Eby because he conveniently never knows anything (like the title negotiations) until he is caught

English

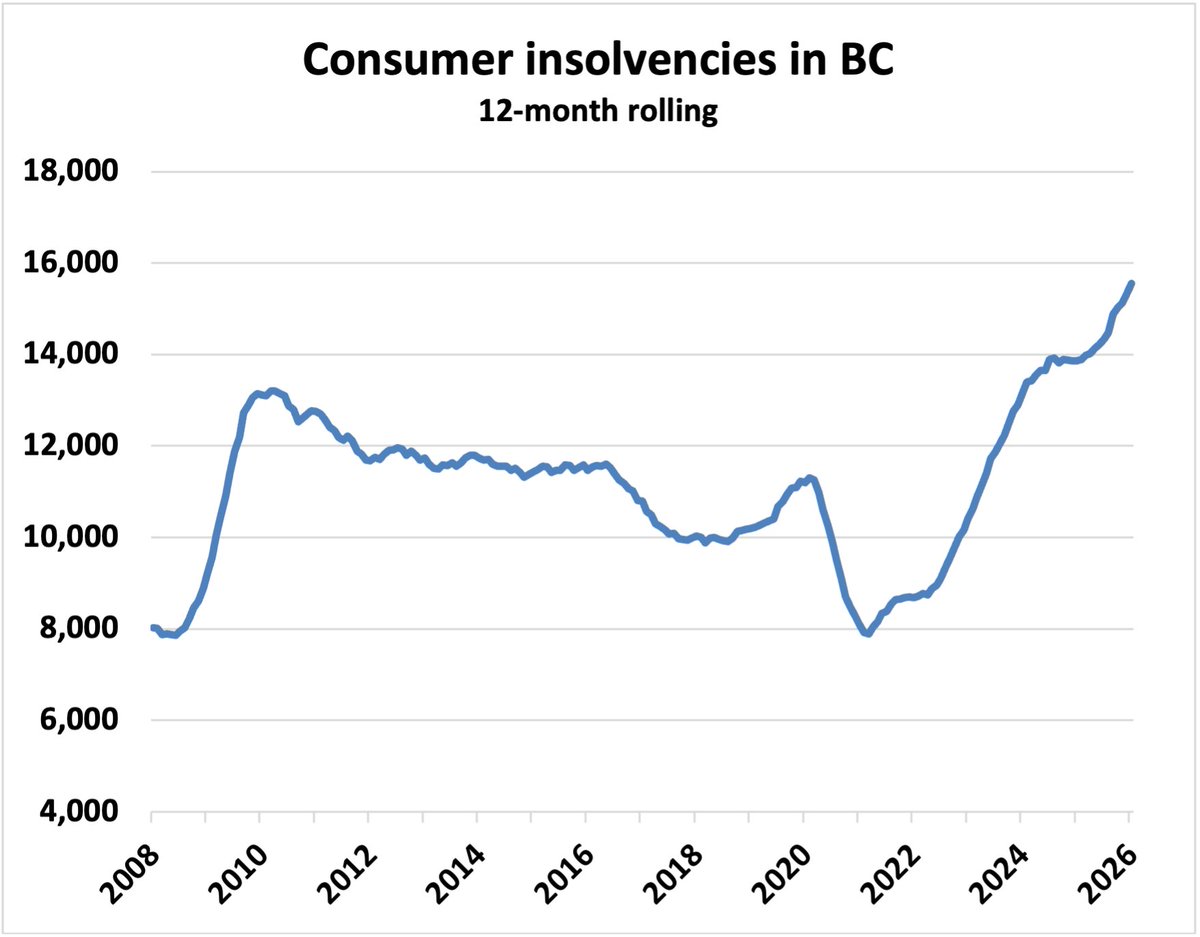

What's going on in BC? Noticeably worse insolvency trends than the rest of the country right now

English

@BenRabidoux @danielfoch Oh, you mean in the land of the “Mortgage Helper” where nearly everyone rents out their basements to cover the mortgage? Places like Kelowna where a dump starter was $950k with household incomes under $100k?

My guess; a flood of purpose built rentals, rising costs & unemployment

English

Do you hear those rumblings folks?

This happens every time oil prices spike.

Suddenly the "dirty oil" that belongs to Alberta & should be kept in the ground becomes "Canada's oil".

Get ready for the grab.

The Globe and Mail@globeandmail

How the oil shock could lead to wider economic pain for Canada theglobeandmail.com/business/artic…

English

Nothing unusual about gold selloff. Profit taking a 3yr move and raising cash as we go risk off. Think it spends most of the year building the next base.

English

@JonFlynnREstats Nice. Last time I took some rotors to the metal recycler, I got a flat tire from sheet metal screws that were everywhere. Now I throw them in the trash.

English

@danielfoch @JFN1971 Mass migration

Mark Carney

Monarchy

English

Canada has observed the largest decline in happiness in the world (along with the UK)

English

No military navy captain, the highest authority at sea, will be so crazy to put his and his crew lives at risk for what is objectively a suicide mission in the current circumstances. Why do you think the USS Lincoln isn’t in the area of Hormuz anymore?

FinancialJuice@financialjuice

The UK and others are ready for efforts for safe passage via Hormuz

English

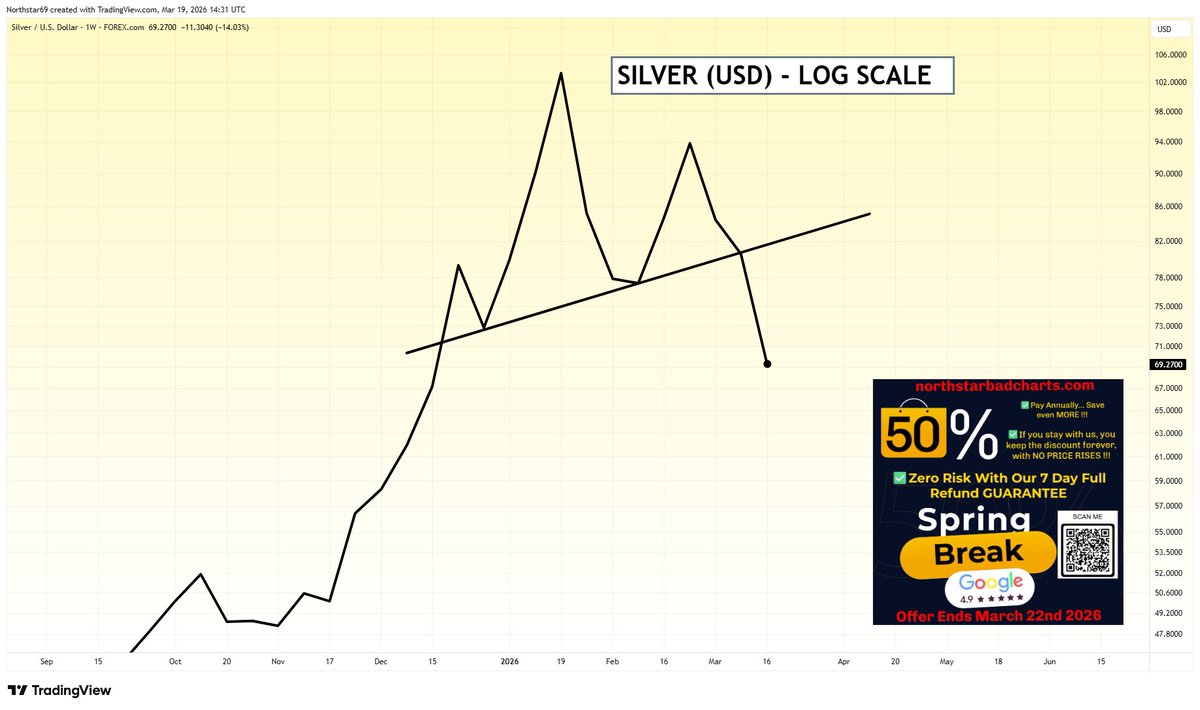

@NorthstarCharts Massive 50% discount in miners 😅

English

Our website members were well prepared for this. Were you? It's not too late to join us with a massive 50% discount at northstarbadcharts.com

English

@FibSixOne8 There will be a re-entry point here at some point but I think patience is required. Gold may be the canary in the coal mine here for a broader selloff in the rest of the market and credit. It will shine, but not until it’s done being the baby in he bath water

English

you have to go back to sept 2023 to find similar levels now

FibSixOne8@FibSixOne8

Last two times that gold became this oversold on the hourly chart, it was one or two days from the next major move up. #gold #silver

English

@FibSixOne8 Will be a steal at $6.50 if it makes it that low.

English

$apm.to $anpmf gap fill.

Price has been consolidating the 10-15x gains since September 2025.

Q4 earnings coming up (which will break all records), and Q1 is not being priced-in AT ALL, which during that time frame, gold has maintained 5k and silver averaged $84/ounce.

English

@BluntButRight @business Yep. More Canadian taxpayer money into the black hole of corrupt pockets (bailout friends). I had never heard of this company and when I saw a headline with a doctored photo of a glorified concrete parking lot I knew what this was, just another robbery.

English

Prime Minister Mark Carney’s government announced a 10-year, C$200 million ($146 million) agreement to use a private space port on Canada’s east coast as it pursues a satellite launch capability independent of the US and other countries. bloomberg.com/news/articles/…

English

@wokal_distance Don’t forget that April 01 Canadas carbon tax (self inflicted wound) increases. We are our own worst enemy here.

English

9/

Once we see inflation, the clock is ticking on *stagflation* because if the economy does not begin to grow you'll have a shrinking economy, increasing unemployment and inflation of prices - and that's the calling card of stagflation.

English

1/

Carney gives the appearance of getting things done, so people see him as accomplishing things, defending Canada and making change happen.

This will hold for a while, his support is rock solid.

However, Carney is headed towards a brutal recession, and *stagflation*

/🧵

Polling Canada@CanadianPolling

(Models Available For Subscribers) Federal Polling: LPC: 48% (+4) CPC: 27% (-14) NDP: 15% (+9) GPC: 5% (+4) BQ: 4% (-2) PPC: 2% (+1) EKOS / March 15, 2026 / n=937 / Online (% Change w 2025 Federal Election) Visit @338Canada for polling details: 338canada.com

English

@CarlHigbie @sask_farmer “A small price to pay” as some would attempt to rationalize.

English

So the Measles vaccine caused 30x the deaths than Measles itself… got it.

English

@RippleXrpie @Krommsan Committed to price stability means you’re gonna see rate hikes into a declining economy as the energy shock arrives (hasn’t rippled through yet but it’s in the pipeline now).

Stagflation

English

🚨WTF!!?? 👀

🇨🇦 The Bank of Canada has admitted that the economy is broken and that there are no solutions to fix the situation.

English