Sabitlenmiş Tweet

imani

1.1K posts

imani

@imani_chilo

building @sortedwallet writing https://t.co/gLZTW8apdO prev @snap | @cornell

Now Katılım Ağustos 2011

293 Takip Edilen284 Takipçiler

Tokenized financial instruments on USSD so that everyone can save and earn a yield on their money.

That is being built in Africa on Starknet.

English

@insane_analyst Are you concerned at all about those Nvidia calls with lack of price action following recent earnings/announcements?

English

If for some reason any of you are bearish CPO or advanced optics, here is my book. Go invert it. The only long that has zero optics exposure is Intel. Go short all of my other longs in size. I dare you.

English

Live your life you have today or be born as a King of England 200 years ago? Which life would you rather have?

Once I answered that, I thought damn. Last year @dylan522p tweeted “Whether you’re religious or not remember to be grateful, this is the biggest economic boom ever”

English

Leo ni Leo!!

African football at its finest! Rooting for Senegal & Morocco 💪🏾

Love Egypt & Nigeria tho - great teams.

English

Wrote a piece for @lavavc_ on SME financing in Africa, covering the work that @jia_DeFi is doing bringing onchain liquidity to where it’s needed most.

Thanks to @s3unha and the team for the opportunity

s3unha@s3unha

@imani_chilo gave us a fresh take on @jia_DeFi by comparing it w/ glocal institutions: - onchain credit @creditcoop_xyz @goldfinch_fi - 🇹🇿 fintech @ramani_io @omniretailinc - 🇹🇿 banks @kcbbanktz @CRDBBankPlc writing.lavavc.io/p/jia-bringing…

English

totally agree with this, and shared similar thoughts on my recent substack:

local stables may not provide sufficient value to drive domestic adoption in markets with instant reliable payment rails

programmability of onchain money does offer a compeling use case but I think you need the network effects in terms of merchants and users in countries where the ave user doesn't have much disposable income.

the biggest use case I see local stables serving in the near term is connection to local fiat for x-border flows, with usd (or other highly liquid) stablecoins still facilitating the actual x-border money movement.

this could look like:

user/business mints local stable a via issuer-> swaps for usdt -> sends x-border to another wallet-> receiver swaps usdt to local stable b -> and redeems fiat.

lucrative yield on reserves backing local stables is what enables this flow. those prefunding today can be LPs, earn yield on their accounts, and payout when they need.

kunle.app@ay_o

Been thinking a bunch about sovereign stablecoins (independently issued non-USD stablecoins). I've long believed that the primary drivers of USD stablecoin growth is access to USD, but that doesn't hold true for non-USD stables. So far I think: 🚄 All the benefits of speed, programmability, 24/7 availability, finality and high limits can be made uniformly available around the world. In this model, turns of money can matter far more than AUM (different business model than the USD majors, but still a good business) 🏦 The competitiveness of a locally pegged stablecoin vs. local fiat depends greatly on the limits/constraints of local payments rails (eg if a local rail has low limits for institutions doing certain types of transactions, a locally pegged stable can fill that gap). 💹 One of the most novel/compelling advantages of a locally pegged stable that shares yield and is both easily off ramped + interoperable onchain, is that it is a better form of money at rest than fiat cash or a local checking account; its a new source of demand for local government debt, and a higher earning form of cash than a local checking account or even cash in hand. More to come.

English

one key point here is the point of on-ramp/use case.

say this is being used for remittances where I'm abroad and go from usd->usdt, and use this to mint ngn tokens that i send to a local then thats an overall positive for the economy

on the other hand if the main use case is local users going from ngn->usdt->ngn tokens, then yeah i agree that is overall inflationary

English

@b3npayd But yes, We do agree on RWA backed local stablecoins as the sustainable path forward for our fragile economies.

English

This is accurate but an oversimplification in my opinion.

Here's two scenarios (Long post alert, TL;DR towards the end);

Scenario 1.

Fully USD-backed stablecoins used locally

If I mint 1 USD-backed token (say, 1450 NGN equivalent), that token is not new NGN, it’s a digital claim on a foreign reserve asset.

It doesn’t directly expand Nigeria’s money supply.

The real issue with this is currency substitution: At scale, people start saving, spending, and pricing in USD-pegged tokens instead of NGN.

The economy starts “thinking in dollars.”

FX shocks pass through faster to local prices.

The central bank loses policy control over demand, inflation, and liquidity.

The risk here is the slow dollarization of domestic money and the weakening of monetary sovereignty.

Scenario 2:

Synthetic or under-collateralized NGN “pegs”

Now, this is where the inflation argument holds water.

If someone mints 1450 NGN tokens supposedly worth $1 without full USD or NGN backing, that’s unregulated money creation.

You’re effectively printing new purchasing power out of thin air.

At scale, this can absolutely become inflationary and destabilizing, the same way an unbacked central bank expansion would.

Here's what I think would make sense especially in the context of emerging markets;

Basicallt re-architecting stablecoins to preserve sovereignty while unlocking speed.

That means:

Local, 1:1 fiat-backed stablecoins with reserves held in local banks or MMFs.

Transparent on-chain FX pools eg cNGN/USDC with proof of reserves, circuit breakers, and fair pricing mechanisms.

Redemption SLAs, liquidity buffers, and stress-tested risk caps to prevent runs.

Regulatory integration for oversight and monetary data visibility. (This is essential for building trust as well)

Basically having programmable, fast, borderless liquidity, without undermining local monetary systems.

TL;DR

The $1 to 1450 NGN = inflation analogy is only true if the NGN token isn’t fully backed.

Fully USD-backed stablecoins risk dollarization, not direct inflation.

A sustainable path forward is potentially local-collateralized money + transparent on-chain FX.

Speed, trust, and sovereignty, all at once.

elias hezron@0xeliashezron

Here's why I am against synthetic and USD backed stablecoins for our fragile economies. Let's say I hold 1USD in my reserves, that then permits me to mint 1450 NGN into circulation. Essentially, I have just put 1450NGN into the economy that never exited. Now imagine this at scale, with billions. Then imagine this with a company that's unchecked, unregulated, and out for profit. How much inflation can the economy cushion before it grumbles?

English

Love to see it…congrats @machuche1 @victorthetravlr

Neda Pay@nedapay_xyz

We’re excited to share that NEDApay has been selected to join the next cohort of the @celo_camp! One of the biggest programs supporting innovative projects building mobile compatible solutions on Celo. This opportunity brings together 12 startups from around the world, each focused on shaping a more inclusive financial ecosystem. Through the eight-week program, our team will focus on refining our mini app on @farcaster_xyz as well as a MiniApp on @minipay to make cross-border payments across Africa simpler and more transparent. Stay tuned for more updates! 🫡

English

@mrstephendeng @CoinStokes Curious...in what ways you've seen PSPs risk appetite changing?

English

@CoinStokes Not sure how I described a CLMM.

But point here isn't the structure of onchain fx, it's how local currency tokenization + risk appetite of tradfi is now changing what might be possible with onchain FX.

English

Something interesting brewing at the intersection of:

1. tokenized local currency (local stables, bonds, etc.) +

2. risk-on PSPs who own collections/payout +

3. AMMs that manipulate treasury/liquidity incentives on-demand

All this with stables issuance-as-a -service emerging.

English

You can read my Substack article here - open.substack.com/pub/kisaxyz/p/…

English

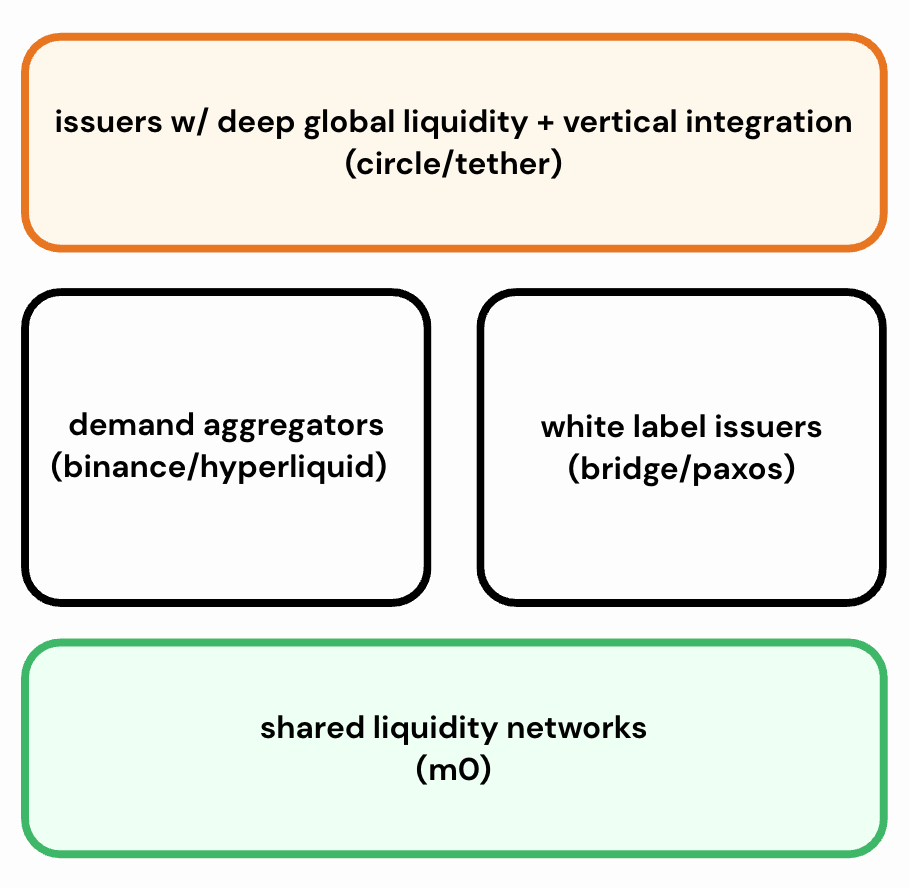

I wrote about the accelerating growth we are currently seeing in stablecoin issuance right now, as every platform circulating stablecoins starts to chase yield.

Liquidity is the bottleneck that every stablecoin will likely face in the future as it tries to scale.

I made a bet that usdt/usdc will continue to dominate due to their deep liquidity + network effects, but at the same time we will see a rise in shared liquidity networks that issuers build on top of.

And seems like this is where Bridge is going with the launch of its new Open Issuance platform (I've got to update my visual 🙂 - but the point still stands).

Bridge@Stablecoin

1/6 Today we announced Open Issuance, a new platform that enables any business to launch their own stablecoin. As stablecoins increase in adoption, businesses handling a large flow of funds need greater control of their product experience, roadmap and their economics. Open Issuance gives businesses control over key stablecoin design choices, while also providing the ability to maximize rewards and benefit from shared liquidity and interoperability. 🚀

English

Wrote a piece on this on my Substack this past weekend.

Tempo is aiming to build settlement infrastructure for the internet in the era of AI

In this post I cover how:

- Tempo's success hinges on balancing neutrality vs distribution

- The decision to build a layer 1 blockchain instead of building on a neutral layer (i.e. Ethereum)

- Comparisons to Libra

- Tempo and Stripe may still win even if they don't achieve what they set out to accomplish

open.substack.com/pub/kisaxyz/p/…

imani@imani_chilo

Wow! excited to see how @Tempo shapes up long term A built-in AMM is quite powerful in moving towards stablecoin singleness in payments Are we about to see the fastest adoption in terms of transaction volume for an L1?

English

"In less than two years, stablecoin jobs have expanded beyond crypto outfits to become established roles across traditional finance."

Bloomberg @business has the receipts

Chuk@chuk_xyz

There is insane demand for people who can enable stablecoin technology in fintechs and FIs. Block, Stripe, Airwallex, Fiserv, Ramp and many more Supply of stablecoin engineering talent is limited!

English

@thepatwalls Peter Lynch talks about this being one of his most successful strategies behind his investing

English

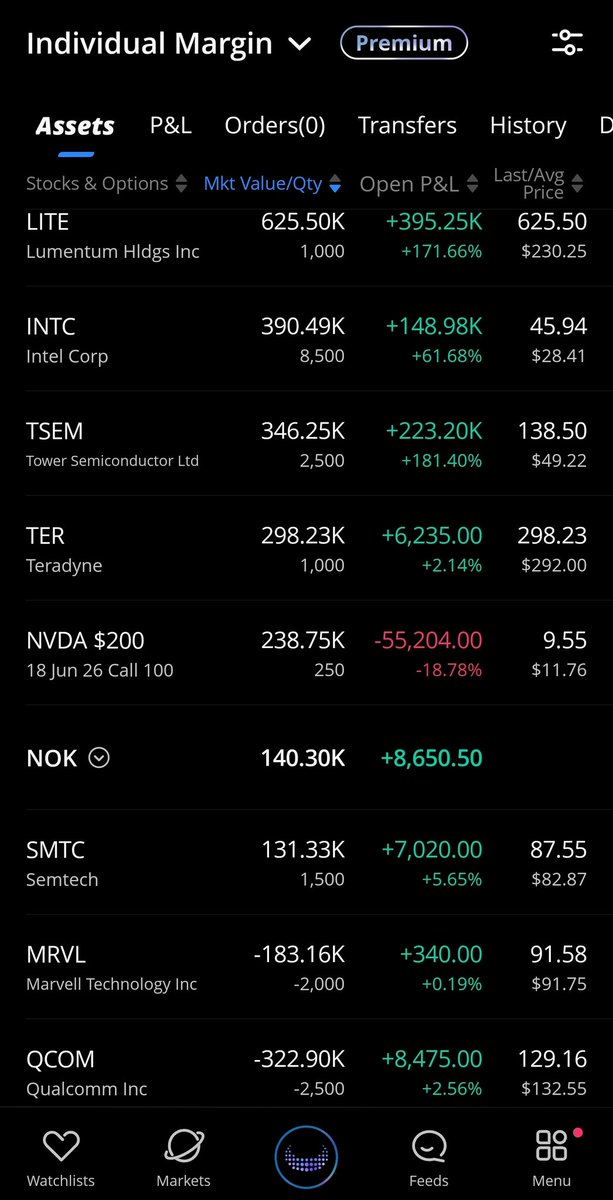

Is this dumb?

So i have this investing philosophy.

Whenever i have a "magic moment" as a customer, i pull out my phone and invest a lil bit into stock.

e.g.

- amazon delivering a package in 2 hours

- tesla driving me across the country with FSD

- choosing loyalty to Marriott bc they're so consistent

over time, this adds up, and my holdings are reflective with the products im most excited about.

i feel like as an investor you need some sort of edge.

and my edge is... being a REAL customer.

where maybe investors who react to earnings reports and make short sighted decisions

Is this dumb?

English

Wow! excited to see how @Tempo shapes up long term

A built-in AMM is quite powerful in moving towards stablecoin singleness in payments

Are we about to see the fastest adoption in terms of transaction volume for an L1?

Patrick Collison@patrickc

Introducing @Tempo. At Stripe, we care about high-throughput, low-latency payments use cases. As the use of stablecoins (and crypto more broadly) grows across Stripe, Bridge, and Privy, we found that existing blockchains are not optimized for them. For example, it's valuable for real-world financial applications that fees be denominated in a fiat currency that makes sense to the user, but existing blockchains denominate their fees in blockchain-specific tokens. Batch transfers are very useful in payments, but much less important in trading. Bitcoin does ~5 TPS; Ethereum does ~20 TPS, some (like Base and Solana) get to ~1k TPS, but Stripe peaks at >10k TPS. And so on. As such, we decided to incubate Tempo, a new blockchain, in partnership with Paradigm. We think of Tempo as the payments-oriented L1, optimized for high-scale, real-world financial services applications. Tempo is an independent company, with Stripe and Paradigm as the first investors. To ensure that Tempo serves a broad array of needs, we're excited to be working with Anthropic, Coupang, Deutsche Bank, DoorDash, Lead Bank, Mercury, Nubank, OpenAI, Revolut, Shopify, Standard Chartered, and Visa as initial design partners. We will start with an independent and diverse validator set, and plan to move towards permissionless validation. Tempo will have a built-in stablecoin AMM to enable platform neutrality with respect to different stablecoins, and Stripe itself will of course continue to work with many chains as first-class partners. We hope that Tempo makes it easier for things like payment acceptance, global payouts, remittances, microtransactions, tokenized deposits, agentic payments, and more, to move onchain. The Tempo team is 15 people today, led by the terrific @matthuang. If you're interested in building Tempo, get in touch! And if you're interested in partnering, reach out to partners@tempo.xyz.

English

@machuche1 Ahh didn't know that, but for pick up too they always ask "is your map showing right location?"

English

@imani_chilo I think for TZ they wanna confirm the location you’re heading to to see if it makes sense. On the driver’s app they see the pickup location but not drop off apparently..

English

Every time you order a bolt/uber in Tanzania smh

Who decided that?@destinyspoke

When I order goods, the rider calls me and tells me they don’t know the location…..that is clearly stated on the app… And I have to use landmarks to describe where I’m at

English

@paulemmanuelng Yeah there's def a sense of entitlement, but also idk if Amorim's system suits our players...our best players - bruno and amad - playing out of position...its so worrying

English

I used to like Manioo but bro looks average to me right now.

He was started against a 4th division team, what did he do? Nothing

The sense of entitlement in these man United players is crazy. They don’t have the fight in them.

Now look at Rashford that was lazy at United, he is now showing work in Barcelona and running like who has a train to catch up.

English

These players are so desperate to make Amorim look bad

Of course I don’t entirely believe in his system but these players can do better

They don’t behave like a team. Man United deserves to be relegated for them to learn. Sometimes we just need to learn things the hard way.

Fabrizio Romano@FabrizioRomano

🚨 Kobbie Mainoo asked again to Manchester United about chance to go on loan in the final 48h of the summer window. Kobbie insists despite Amorim’s words in press conference and Man United clear reply. #MUFC insist on no chance for exit and plan to keep Mainoo.

English