Sabitlenmiş Tweet

RecessKickBallStar

5.2K posts

In Sochi, a drunk Russian vatnik wanted to impress his friends and jumped from the roof into a pool, but something went wrong...

English

Català

English

For $SIVE to become the next $80B+ $LITE.

Sivers is the current laser kingmaker of the optical transition to CPO and 1.6T.

They basically supply lasers to the leading players in the CPO space.

From likely $MRVL Celestial, Lightmatter, Lightelligence, $POET, and others for CPO. before they got big.

And now with large players like $JBL for 1.6T LRO + more test/qualifications underway for pluggables.

They've finally solved the Catch22 problem, and have the attention of the market to pull off foundational CPO related IP acquisitions downstream on NASDAQ listing (or now with equity).

And expand revenue as much as possible from the laser source into:

-> Optical Engine/ELS value.

-> Optical Transceiver IP

Just like $LITE did to drive their valuations from $2B -> $80B in 2 years.

But instead of EML + pluggables, Sivers is doing this for the CPO supercycle, the fastest TAM expansion in history for photonics.

I'm following the story for them to pull this off this David vs. Goliath shift catching up to $LITE.

More than I care about little MC % returns that's happening currently.

Barbara Kek@kekbarbara

@aleabitoreddit What’s your goal on Sive @aleabitoreddit

English

If my stocks don’t go up in a parabolic way from the moment I enter I feel like a failure.

English

@cyberprince_rwo It’s finna be more overvalued by the end of the year

English

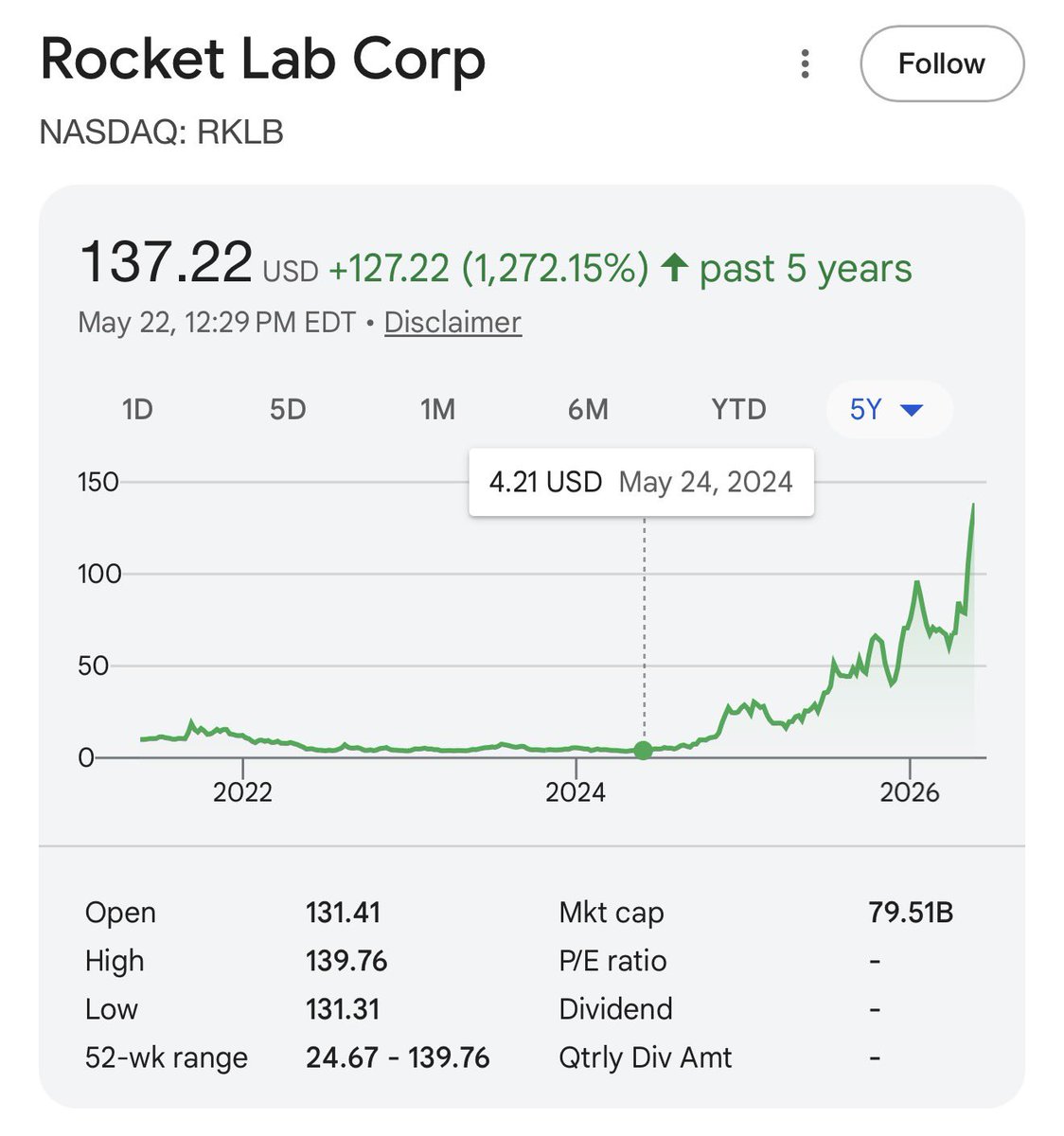

$RKLB is so so overvalued and I love it.

Fuck efficient markets.

English

That's all for now!

But before you go...

If you found this thread helpful consider:

1. Following me @SalVetriDFS for more of these

2. Repost this thread so others can find it too :)

SAL VETRI@SalVetriDFS

Here are 7 players I'd bet my house on this fantasy football season: 1. Tyler Warren...

English

@cyberprince_rwo Millions are regarded. 600m sub 100 iq

English

Why is India so ghetto?

Most of their population truly feel like they are like 300 years behind.

It’s hard not to be racist man.

English

why is this considered a castle but the one in disneyland isn't. they were built 60 years apart

only aesthetic@aestheticpost

The spirit of the Middle Ages truly exists...

English

@Sandeman52 There are only downsides. What’s the benefit of sharing prematurely? It should be a surprise on the 1 year wedding anniversary that they aren’t brokies.

English

Yoda is 22. Net worth 200k. Most likely he will have millions in his 30s, probably could retire early, live an amazing like.

Should he tell his girlfriend…who he says by his own words “is the one” his money situation?

I want answers only from guys who are 30 and older. Can someone give this young buck advice. I already gave my opinion in the original thread.

YodaStocks@YodaStockInvest

Should I share my portfolio with my girlfriend or not? My situation: I’m 22 years old with a portfolio worth 200k

English

Leopold Aschenbrenner's 13F never came on Friday.

Here is the REAL reason why, and what it tells you:

The most likely explanation is that he requested confidential treatment from the SEC.

Confidential treatment is a legal tool that lets large funds delay disclosing positions they are still actively accumulating, sometimes for UP TO A YEAR.

Funds use it for one reason: they are building a position big enough that public disclosure would MOVE THE PRICE AGAINST THEM before they are done.

If that is what happened here, it means Aschenbrenner is quietly accumulating something significant and does not want the market to see it yet.

The 24 year old who turned $225 million into $5.5 billion in 12 months going dark on the one day he was legally required to show his hand is not nothing.

Pay attention to what happens when this position finally becomes public.

We are checking every day, and when it comes, we’ll share it here publicly.

Turn on notifications so you don’t miss the signal, this is VERY important.

Many people will wish they followed us sooner.

English

$3.47 to $100 in two years.

$RKLB retired so many of my followers 😂

English

@KabraxFX @TheStocksKing Feels wierd. Thought it was a straightforward and good report for q1

English

@inspector_token @TheStocksKing No idea, but probably a buying opportunity. The majority of the names I hold today are red.

English

$ROOT needs some more votes! If you believe $ROOT is the best choice for this week's @TheStocksKing community pick!

TheStocksKing@TheStocksKing

Over the last weeks we have seen many companies obliterate earnings. Just like $ROOT did but what is the best buy? Let's decide as FinX on TheStocksKing . com👇

English

@BenTenGolds Your claims are what stupid people call evidence

English

$MELI

The market is focused on margins compressing, operating income declining 20%, and some experimentation with the credit products but underneath the surface this may have actually been one of the strongest strategic quarters in $MELI history. Revenue grew 49% to $8.8b, TPV grew 50% to $87b, and GMV grew 42% to $19b.

This is not a mature company struggling to grow a few extra percentage points. This is a company already operating at massive scale while still growing like a startup. The really important thing is that growth is actually accelerating in several key areas even while they are intentionally sacrificing short term profitability. There’s a big difference between weak margins caused by weakening demand and weak margins caused by aggressive reinvestment.

The entire philosophy behind this quarter is actually pretty simple. $MELI believes Latin America is still extremely early in the digital commerce and fintech transition, so management is choosing to maximize long term ecosystem dominance instead of optimizing near term margins. Honestly, when you look at the underlying numbers, it becomes pretty hard to argue against that logic.

The average American makes around 40 online purchases per year while the average Latin American makes just 7. Even buyers on $MELI only average around 11 purchases annually today, which means ecommerce penetration still looks extremely early. If management believes that number can eventually double or triple over time, then aggressively investing today probably makes a lot of sense.

The lower free shipping threshold in Brazil is probably the clearest example of this strategy. Most investors initially saw it as margin destruction, but $MELI clearly views it as long term habit formation. After lowering the threshold, Brazil GMV growth accelerated to 38%, items sold growth accelerated to 56%, and unique buyers accelerated to 32%, the fastest growth in five years.

What stood out to me most was that daily active users are now growing faster than monthly active users. That usually means engagement itself is deepening, not just user acquisition. Anyone can temporarily buy growth through promotions, but when conversion, frequency, and retention all improve simultaneously, it usually means consumer habits are actually changing. That’s where internet businesses become extremely powerful.

What makes this even more interesting is that the economics are already improving faster than expected. Unit shipping costs in Brazil declined 17% versus 11% last quarter, and almost half of the profitability hit from the lower shipping threshold has already been offset through efficiency and scale of logistics. They said that lower cost shipments are already breakeven.

This is basically the classic ecommerce flywheel playing out in real time. Lower shipping costs improve conversion, better conversion drives higher order density, and higher density improves logistics efficiency which lowers costs further. Over time, the ecosystem becomes stronger and more profitable because scale itself becomes the advantage. That is exactly why companies like $AMZN became so dominant over time.

I also think people massively underestimate the importance of the logistics network itself. $MELI now operates more than 50 fulfillment facilities and fulfillment handled 55% of shipments during the quarter while growing 39%. The moat is no longer just the marketplace or app itself. The moat becomes warehouses, delivery routes, seller relationships, underwriting data, payments infrastructure, advertising infrastructure, and consumer habits all compounding together into one ecosystem.

1/ 👇

English