Jon Arnell retweetledi

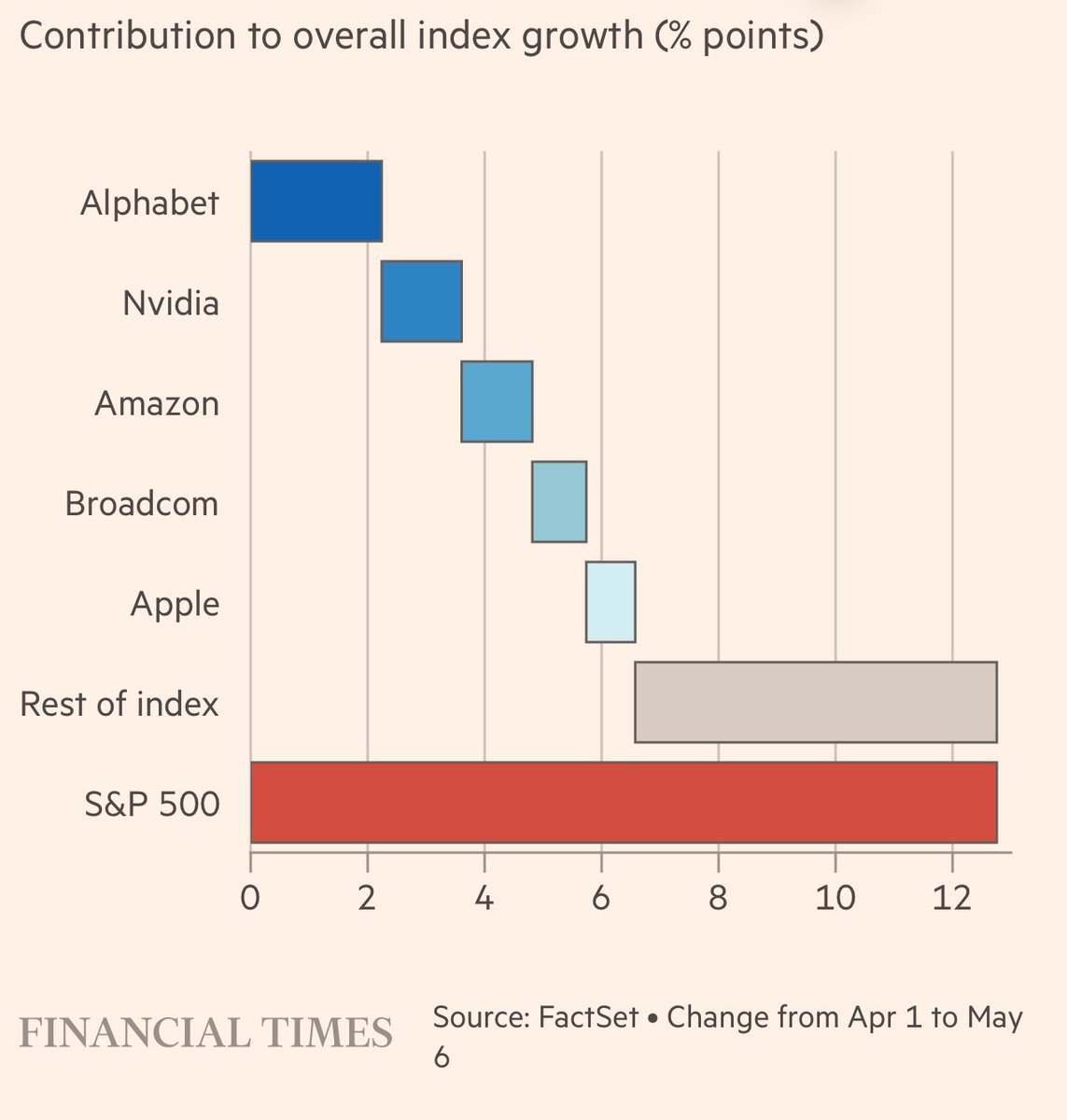

"The earnings outlook is more dependent on a few stocks than ever before" --BofA

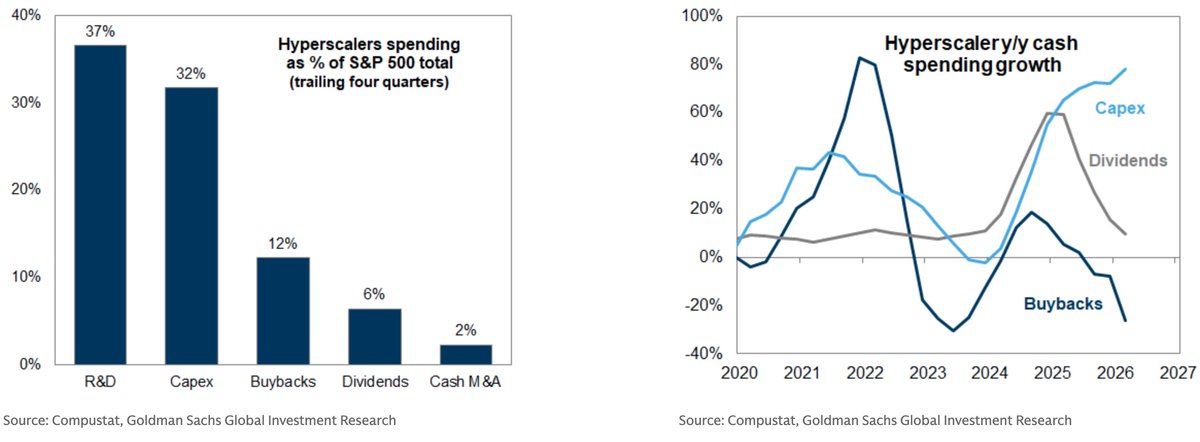

the top 5 cos make up around a quarter of S&P 500 earnings

English

Jon Arnell

3.8K posts

@jon_arnell

Chief Investment Officer på von Euler & Partners en del av Säkra. I marknaden sedan 2004. Fokus global tillgångsallokering. Tidigare aktieanalys och trading.

HORMUZ DISRUPTION TO LAST INTO H2: GOLDMAN POLL A Goldman Sachs survey of 837 investors shows growing expectations that shipping through the Strait of Hormuz will remain disrupted well into the second half of the year. • Most see disruption beyond June • 43% expect normalization only after July • Brent forecast clustered at $80–$90/bbl The outlook reflects stalled U.S.–Iran talks and fears of a prolonged supply shock in a key global oil route. Investors are also positioning for “short oil” if flows recover.

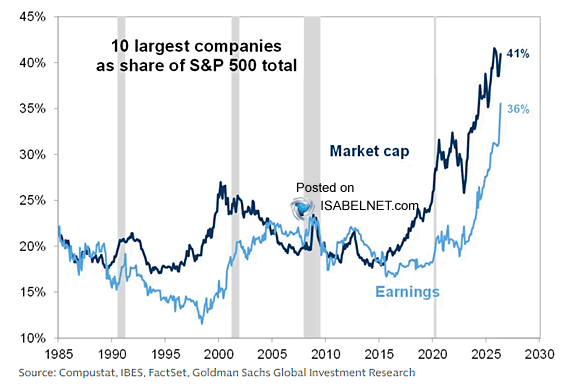

AI bubble watch. BofA Hartnett

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy: "We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%. If you think about the periodicity of significant bear markets. Since 1970, we get a mean reversion about every 10 years. Let's say mean revert to the past 25 or 30-year PE. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP. 10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect. In the stock market, we're over-equitized as a country. We have the highest individual equity weightings in the history of the country. And then the real problem is if you look at private equity in 2007-2008, that was about 7% of institutional portfolios. Now it's about 16% of the institutional portfolios. We're so much more illiquid than we were in 2008. The problem is that if you buy the S&P at this current valuation, the 10-year forward return is negative when you buy the S&P with a PE of 22. That's what history shows. So yes, the S&P is spectacular long-term, if you have a hundred-year view. But that's because that's an average of a hundred years, including times when the S&P 500 PE was 6, 7 and 8, or one third of what it is right now. Valuation matters a lot, and the stock market's really high and it's gonna be really hard to make money from here with any kind of long-term view."