Now that $SATA plans to pay 13% yield in daily dividend do we think $STRC will follow and go from bi-monthly to daily and up its yield from 11.5% ? We are already seeing the nav dropping close to $99.

English

Systems Over Noise | Code & Capital

1K posts

@junedkazi

Engineering leader in payments and platforms. Writing about payments, commerce, AI, and where I'm putting my money.

It was an honor to be shown the awesome @Intel fab in Oregon this week. Looking forward to a great partnership with @SpaceX & @Tesla!

Strategy is calling $STRC 11.5% yield a "high-yield savings account." It's not. It's a single-name junk bond with embedded crypto beta. Here's the breakdown before you put real money in it. WHAT $STRC ACTUALLY IS $STRC ("Stretch") is a perpetual preferred stock from Strategy (formerly MicroStrategy), launched July 2025 at 9% yield. Strategy has hiked the rate multiple times to defend the peg, reaching 11.5% today. Notional outstanding has grown to $6.4B as of April 2026, generating an annual dividend obligation of roughly $735M that Strategy must fund through new $STRC issuance, $MSTR equity issuance, or eventually $BTC sales. The mechanics $100 par, monthly cash dividends, rate resets every month in 0.25% increments. If price drops below par, the rate gets hiked to attract buyers. If price overshoots, the rate drops. The whole point is to keep the price pinned near $100 and strip out volatility. There is no maturity. No buyback obligation. No conversion right. Strategy created $STRC as a funding tool for $BTC purchases, and Saylor markets it as a short-duration high-yield savings account. Some analysts now describe it as the backbone of a yield-backed stable coin ecosystem. That framing should make you ask harder questions, not fewer. WHERE IS THE $BTC / $MSTR EXPOSURE On the downside only. $STRC holders do not participate when $MSTR or $BTC rip higher. You collect 11.5% and that's it. Your principal is backed by Strategy's solvency, which depends on 815k $BTC and the ability to keep issuing more preferred at a premium to NAV. You get none of the upside. You absorb all of the downside. WHY THE T-BILL COMPARISON BREAKS DOWN This is where the marketing gets dangerous. T-bills and $STRC are not the same risk universe. Backing: T-bills are full faith and credit of the US government. $STRC is corporate credit on one leveraged company. Insurance: T-bills do not need it. $STRC has no FDIC, no SIPC principal protection, no government backstop of any kind. Terminal value: T-bills have a known face value at a known maturity date. $STRC is perpetual. There is no contractual point at which Strategy ever has to give you your $100 back. Yield setting: T-bill yields are set by Fed policy and Treasury auctions, transparent and market-driven. $STRC yield is set by Strategy itself every month to defend the peg. The seller is choosing the rate. Liquidity: T-bills are the deepest, most liquid market on earth. $STRC trades thinly by comparison and depends on Strategy's ATM issuance machine to maintain the bid. Crisis behavior (this is the big one): in a panic, T-bills rally. They are the textbook flight-to-quality asset. $STRC in the same panic would crash, because the same shock that triggers risk-off also crushes $BTC, drops $MSTR below NAV, and breaks Strategy's funding model. Your "savings account" goes down precisely when you need cash to be cash. WHAT HAPPENS IN STRESS SCENARIOS Mild drawdown ($BTC down 30%): probably fine. Strategy has roughly 21 months of dividend coverage in USD reserves. Price wobbles, rate ticks up, par holds. Moderate stress ($BTC down 50%, $MSTR loses its NAV premium): the funding machine breaks. Strategy can no longer issue preferred at a premium. Has to either sell $BTC into weakness or crank the dividend rate higher to find new buyers. Both are bad outcomes. Severe stress ( $BTC down 70% sustained): the dividend gets cut or suspended. The prospectus is explicit that the rate is variable and not guaranteed. $STRC breaks par hard. Could trade at 60 to 70 cents on the dollar or worse. THE CAPITAL STACK MATTERS This is where most retail buyers do not look, and where the real risk lives. In a Strategy liquidation or restructuring, the order of payment is roughly: - Senior secured creditors (if any get added later) - Convertible bondholders (Strategy has billions outstanding across multiple tranches, all senior to every preferred) - The preferred stack itself, which is layered. $STRF, $STRK, $STRD, and $STRC all have different terms and seniority. $STRC is not necessarily the most senior preferred. Read the prospectus before assuming you are at the front of the line. - $MSTR common equity (last, almost always wiped) Historical recovery rates on perpetual preferred in distressed situations run 10 to 40 cents on the dollar. Sometimes worse. And you do not need a full bankruptcy for pain. Strategy can defer the dividend long before insolvency, since the rate is not contractually fixed and the prospectus reserves the right to adjust it lower or skip it. The "perpetual" structure also cuts the wrong way. There is no maturity event that forces Strategy to ever return your principal. If $STRC trades at $70 for five years, that is just your new reality. There is no catalyst to bring it back to par except Strategy's own willingness to keep raising the dividend, which only works if the funding machine is still running. WHAT TO CONSIDER INSTEAD (yield AND upside) $QQQI (NEOS Nasdaq-100 High Income): ~14% yield via index covered calls on the Nasdaq 100. Tech equity upside plus options income, with Section 1256 tax treatment baked in. $SPYI (NEOS S&P 500 High Income): ~12% yield, same call-spread strategy on the S&P 500. Lower volatility, broader diversification, same tax efficiency. $BTCI (NEOS Bitcoin High Income): ~40% trailing distribution via synthetic $BTC exposure plus call writing. You sacrifice some $BTC upside for steady income, but you get actual $BTC beta with no single-name credit risk. $BLOX (Nicholas Crypto Income): ~36% yield via $BTC and $ETH exposure with an active options overlay. Active management adapts to vol regimes, weekly distributions, real crypto upside participation. None of these are perfect. Some do carry NAV erosion risk and capped upside. The point is they give you actual market exposure in exchange for your yield, not concentrated single-name credit risk on one company's Bitcoin thesis. If you would not park your emergency fund in a single-B junk bond tied to $BTC, do not park it in $STRC.

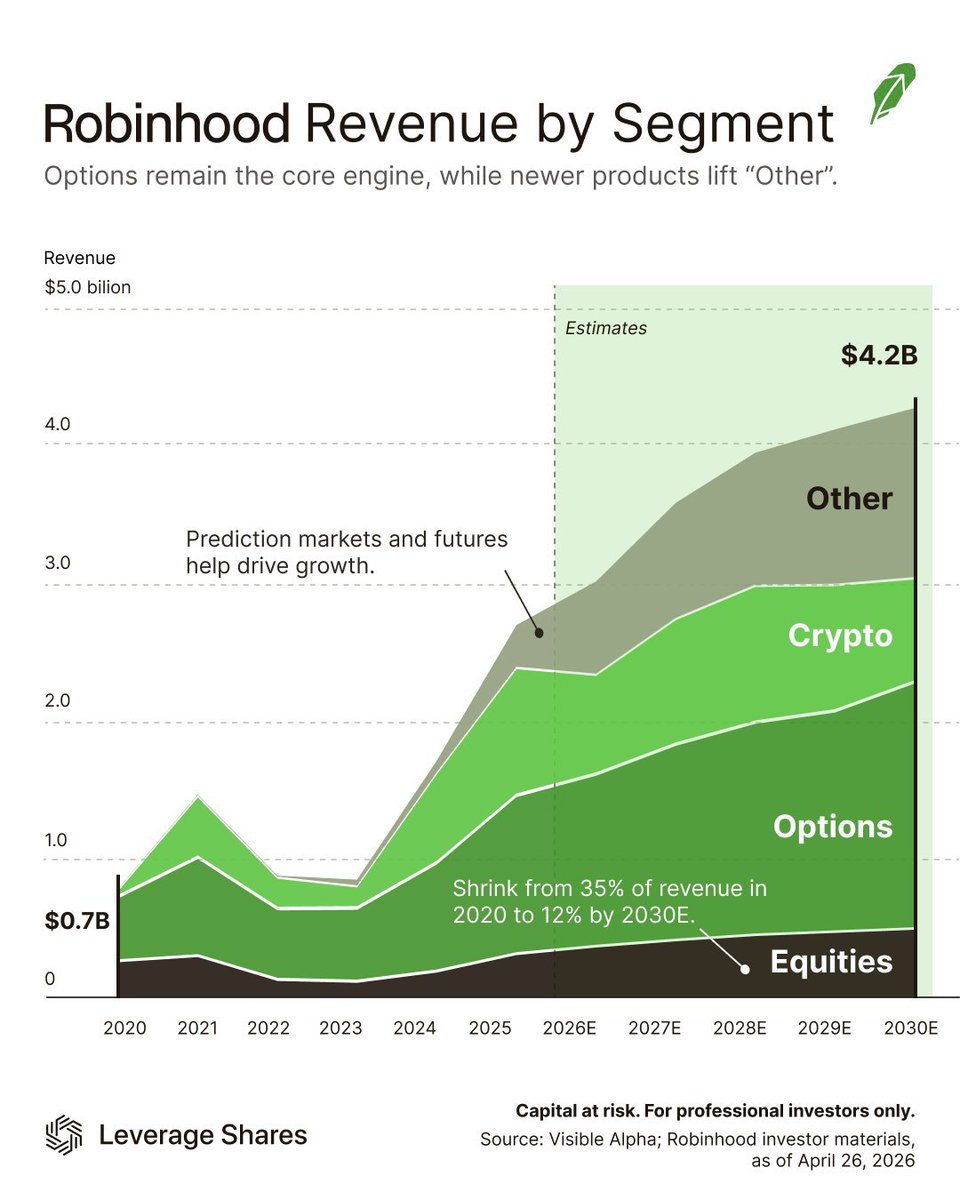

Options still lead, but the mix is shifting. $HOOD revenue is projected to reach ~$4.2B by 2030E, with “Other” and crypto driving most of the growth while equities remain a smaller contributor. Options share declines from ~35% in 2020 to ~12% by 2030E as new products scale.

So you’re telling me we should take out a loan or HELOC to invest in $STRC ?